Impact Analysis of Jiangnan Rural Commercial Bank's Village and Town Bank Merger and Restructuring on Valuation

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Based on the latest search data, the impact of village and town bank merger and restructuring on Jiangnan Rural Commercial Bank’s valuation can be analyzed from the following dimensions:

Jiangnan Rural Commercial Bank held an extraordinary shareholders’ meeting on December 26, 2025, and reviewed and approved two proposals to absorb and merge

Village and town banks have long had the problem of being “small, scattered, and weak”, with non-performing loan (NPL) ratios generally higher than the industry average. According to data from the China Banking Association, the NPL ratio of rural commercial banks was 2.8% at the end of 2024, while the risk situation of village and town banks was more prominent, with some individual institutions having an NPL ratio as high as 4.98% [4]. Through merger and restructuring, the main sponsoring bank can:

- Divest non-performing assets and reduce historical burdens

- Inject capital to enhance capital strength

- Unify the risk management system and improve risk control capabilities

Institutions after merger and restructuring generally achieve three major improvements:

- Higher level of standardized operation

- Stronger risk resistance capability

- Further enhancement of business scope and informatization level with the support of head and branch banks[5]

Taking Changshu Bank as an example, after absorbing and merging 3 institutions including Suqian Sucheng Xingfu Village and Town Bank, its NPL ratio dropped to 0.76% and provision coverage ratio rose to 462.95% as of the third quarter of 2025 [4].

After integration, the integration and sharing of human, material, and information resources can be realized to improve resource utilization efficiency; at the same time, by converting to branches, a more complete information system and risk control system can be established to enhance operational efficiency and risk management level [3].

| Time | Policy Points |

|---|---|

| End of 2020 | The former China Banking and Insurance Regulatory Commission issued the “Notice on Further Promoting Risk Resolution, Reform and Restructuring of Village and Town Banks” |

| 2025 Central No.1 Document | Clearly defined the “one province, one policy” reform path and incorporated village and town bank restructuring into the rural revitalization strategy |

| 2025 Government Work Report | Actively prevent risks in the financial sector, and comprehensively adopt methods such as capital supplementation, merger and restructuring, and market exit to resolve risks by classification |

- Neutral to Positive: One-time integration costs and outlet adjustments involved in merger and restructuring may lead to short-term expense expenditures

- Short-term Pressure on Asset Quality: Need to take over the historical non-performing assets of the integrated village and town banks

- Clear Logic for Valuation Upgrade: Referring to peer cases, improved operational efficiency and risk indicators after integration will support valuation repair

- Economies of Scale Emerge: Expansion of business scale and increase in market share enhance market competitiveness

- Improvement in Regulatory Rating: Effective risk resolution helps to obtain better regulatory evaluations

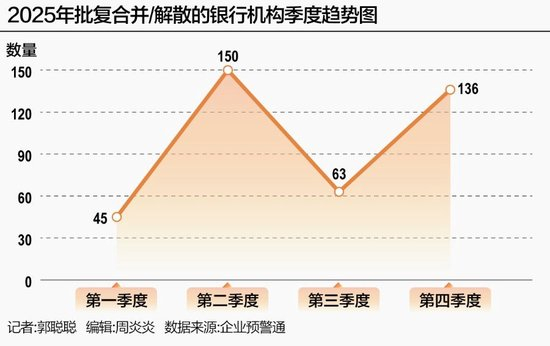

As of December 15, 2025, the number of village and town banks nationwide has plummeted from 1,636 at the end of 2023 to 1,301 [4]. The industry expects that by 2027, the number of village and town banks may further decrease to around 500 [4]. Professor Wang Tingting from the School of Finance at Central University of Finance and Economics pointed out that the integration trend of small and medium-sized financial institutions will continue, but the pace may slow down and become more refined [6].

[1] Southern Net - Banking Industry “Slimming Down” (https://news.southcn.com/node_179d29f1ce/965ea96143.shtml)

[2] Yahoo Finance - Over 300 Small and Medium-sized Domestic Banks Exit Market This Year, Mergers and Acquisitions Speed Up, Number Hits Record High, 90% Are Village and Town Banks (https://hk.finance.yahoo.com/news/今年逾300中小內銀退出市場併購提速數目破頂九成屬村鎮銀行-182300250.html)

[3] Xinhuanet - Over 300 Integrated Small and Medium-sized Banks Usher in Restructuring Year (http://www.news.cn/money/20251204/4ac98b853494419ab91e2e5f39219b66/c.html)

[4] DoNews/Sina Finance - Village and Town Bank Integration Wave: County Financial Quality Improvement Revolution Behind the Reduction (https://www.donews.com/article/detail/8189/94626.html)

[5] Eastmoney.com - Over 300 “Exit” This Year, Integration of Small and Medium-sized Financial Institutions Accelerates (https://finance.eastmoney.com/a/202512203597214091.html)

[6] Economic Reference News - Over 300 Integrated Small and Medium-sized Banks Usher in Restructuring Year (https://www.donews.com/article/detail/8189/94626.html)

高瓴资本重仓德力佳的投资逻辑分析

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.