VeriSilicon (688521.SS) AI Computing Power Opportunities and Business Model Evaluation

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

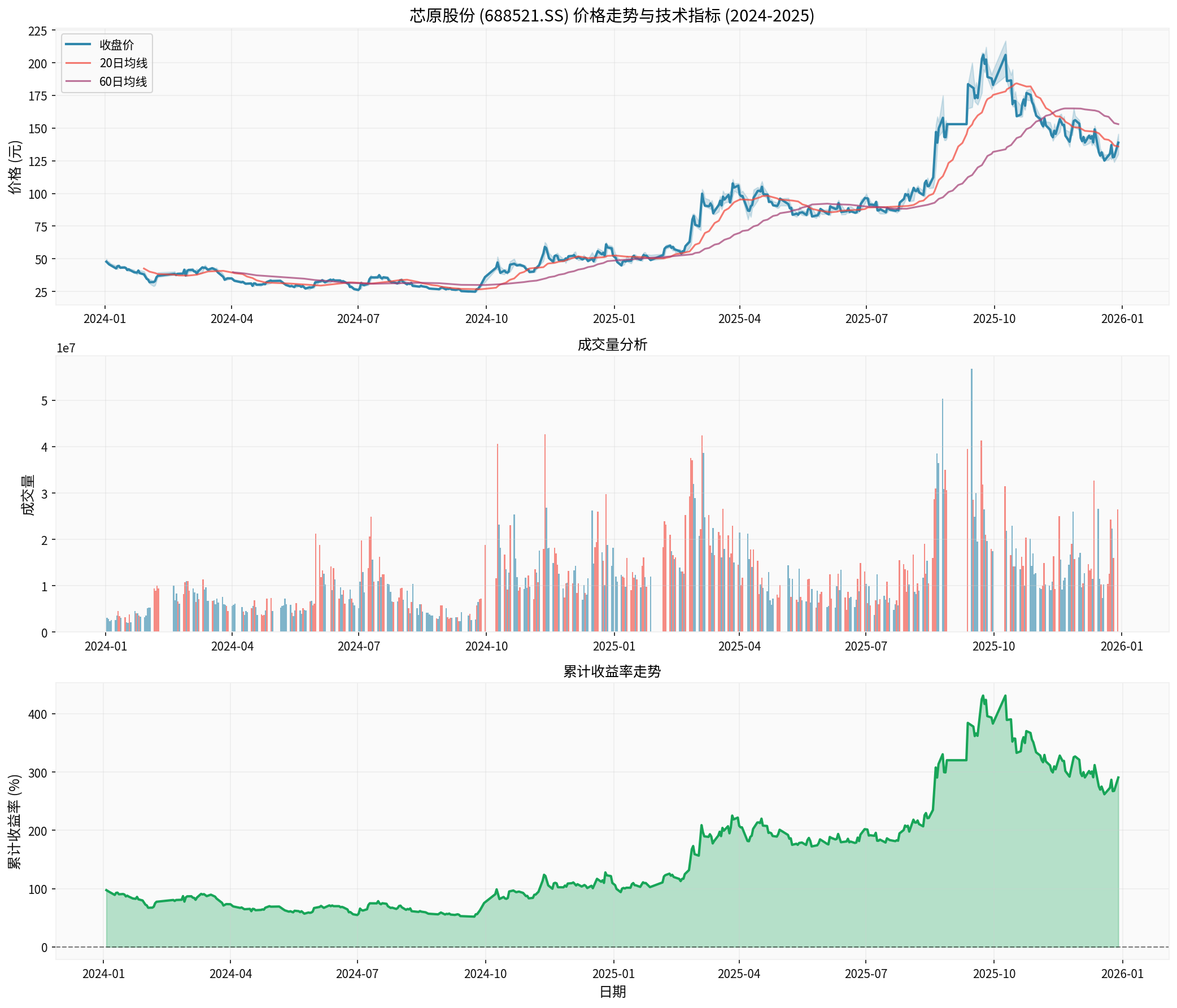

- Short-term share price: The cumulative share price increase since 2024 has exceeded 170%, with an annualized volatility of approximately 75%, indicating high market sentiment and trading activity, and significant volatility and risk [0].

- Industry environment: Global tech companies are accelerating large-scale investments in AI infrastructure (computing chips, data centers) and other areas. Relevant public information shows that the “AI computing power arms race” and trillion-dollar investment plans are gradually being implemented (e.g., multiple multi-billion-dollar investments by OpenAI and its partners, cloud vendors, and chip manufacturers) [1]. This trend provides long-term demand support for computing chips and related design services.

- Company positioning and business: VeriSilicon is a chip design service and semiconductor IP licensing company, covering the entire chain from specification definition, IP integration, design implementation to mass production delivery, with customers including well-known domestic and foreign semiconductor and internet enterprises [2]. The company has laid out NPU IP, Chiplet and small chip technologies, and released product information related to Chiplet and automotive certification [3]. The revenue and net profit growth rates disclosed in Q3 2024 were 23.60% and 29.01% year-on-year, indicating marginal improvement in operations in the quarter [2].

- Profitability and finance: After reaching a peak in 2022, revenue declined from 2023 to 2024 with continuous net losses; gross margin remained around 40% but declined slightly in 2024; operating cash flow and free cash flow were negative recently, indicating pressure on profitability and cash flow [0].

- Certainty of long-term valuation support: Not enough to form a clear conclusion yet. There is great uncertainty in profitability and cash flow, and no available DCF or comparable company valuation data; although AI computing power demand and the company’s technical layout have positive factors, it is necessary to closely track the pace of subsequent customer landing, order fulfillment, and profit recovery to evaluate whether long-term valuation is supported by fundamentals.

- Multiple international media and information platforms report that investment in AI infrastructure continues to heat up, involving OpenAI, Nvidia, Broadcom, Meta, Google, Oracle, Microsoft, etc., with relevant cooperation and investment plans often reaching tens of billions of dollars, some even hundreds of billions, covering AI chips, computing power supply, and data center construction [1]. This trend indicates that the long-term demand for AI computing power and related hardware services is expanding globally.

- Industry research reports and market charts show that the AI chip-related market size is expected to grow continuously from 2018 to 2030, reaching a scale of 100 billion US dollars by 2030, reflecting the industry consensus of “long-term growth in AI chip revenue” (refer to public market research charts and industry analysis reports) [1].

- The increasing design complexity and iteration speed of AI computing chips (e.g., GPU, NPU) have boosted demand for IP cores and one-stop chip design services. VeriSilicon has IP layouts in NPU IP, video/audio, IoT, and data centers [3], and can provide customized solutions for different computing-related scenarios, with the opportunity to benefit from downstream demand growth.

- Chiplet/small chip technology and advanced packaging solutions are becoming important paths to improve computing density and reduce costs. VeriSilicon’s public information involves Chiplet and small chip technology layouts, with the foundation to serve customers and undertake complex projects in this direction [3].

- According to the company’s public information, VeriSilicon adopts a platform-based, one-stop chip customization and IP licensing model to help customers deliver efficiently from specification definition, IP integration, design implementation to mass production [2].

- This model can reduce the resource threshold for customers in chip design and mass production, allowing them to focus more on systems and software ecosystems. For AI computing-related projects that require rapid iteration and multi-scenario adaptation, platform-based services have matching advantages.

- Disclosed customers include many well-known global semiconductor enterprises and internet/cloud-related vendors (e.g., Intel, Bosch, NXP, Broadcom, Synaptics, Marvell, Socionext, STMicroelectronics, Samsung, Realtek; Facebook, Google, Amazon; and domestic Huawei, Unisoc, Rockchip, ZTE, Dahua Technology, Amlogic, ComNav Technology, etc.) [2].

- The company’s concept tags include Chiplet, Artificial Intelligence, Domestic Chips, Autonomous Driving, IoT, etc. [2], reflecting its business layout in computing and intelligent-related scenarios.

- NPU IP: The company has an NPU IP product line (e.g., VIP9000 series) and has promoted automotive functional safety certification (e.g., ISO 26262 ASIL B) for intelligent driving and high-reliability scenarios [3].

- Chiplet/small chip: Public information shows that the company focuses on and participates in Chiplet and small chip-related technology directions, with the foundation to provide advanced packaging and interconnection solutions for customers [3].

- IP licensing revenue: Has certain customer repurchase and scenario reuse characteristics, which are expected to contribute relatively stable licensing and service revenue.

- Chip customization services: More project-based, more affected by order rhythm and industry prosperity, with higher requirements for project management and cost control.

- From January 2, 2024 to December 29, 2025, the opening price was 49.82 yuan, the closing price was 138.85 yuan, the interval increase was about 178.70%, and the annualized volatility was about 75.29% [0].

- The highest price during the period was 216.77 yuan, the lowest was 24.45 yuan, with high price volatility and trading activity, indicating a significant impact from market sentiment and industry themes [0].

- Chart description: From early 2024 to the end of 2025, the share price fluctuated upward with significant阶段性 high volatility; volume distribution shows obvious volume increases at some points, suggesting the influence of themes and events [0].

- From 2020 to 2024, operating revenue (in millions of yuan) was approximately 1506, 2139, 2679, 2338, 2322; net profit (in millions of yuan) was approximately -256, 13,74, -296, -601 [0].

- Revenue peaked in 2022, declined slightly from 2023 to 2024 with continuous losses; Q3 2024 disclosed a 23.60% year-on-year increase in revenue and a 29.01% year-on-year increase in net profit, indicating marginal improvement in the single quarter [2].

- Gross margin fluctuated around 40%, about 39.8% in 2024, slightly lower than previous years [0].

- Operating cash flow and free cash flow have been negative in recent years, with coexisting pressure on cash recovery and reinvestment [0].

- Chart description: From 2020 to 2024, revenue growth was accompanied by profit fluctuations, net profit margin was negative in some years, gross margin was at a medium level, and cash flow was under pressure [0].

- Asset-liability ratio increased significantly from 2023 to 2024, with equity ratio declining; current ratio fell from historically high levels (about 1.71 in 2024) [0].

- Overall, it still has a certain liquidity buffer, but attention should be paid to the rhythm of debt and cash flow recovery.

- Insufficient DCF/valuation data: No available DCF or comparable company valuation data are obtained currently, so no clear valuation range or conclusion can be given.

- Uncertain key variables: The transmission rhythm of AI computing power demand to chip design services, the scale of customer orders and project landing cycles, domestic semiconductor supply chain and policy environment, etc., all have uncertainties.

- Short-term share prices are mainly driven by industry themes and market sentiment, with high volatility and risk; whether long-term valuation can get fundamental support depends on profit recovery, order fulfillment, and cash flow improvement.

- Sustained losses and cash flow pressure: Continuous losses from 2023 to 2024, negative operating cash flow and free cash flow, indicating pressure on profit quality and cash recovery [0].

- Intensified industry competition and project-based risks: Chip design services are highly project-based, with high order concentration and project execution risks; industry competition and overseas restrictions (e.g., advanced process and IP-related restrictions) may affect delivery and expansion.

- Customer concentration and receivable risks: When some large customers account for a high proportion of projects, there are concentration risks in receivables and revenue recognition.

- Share price volatility and sentiment risks: In a high-volatility environment, short-term share price trends are highly related to themes, so attention should be paid to the risks of chasing high and liquidity risks.

- Customer structure and order visibility: The proportion of AI computing-related customers, backlog orders and project reserves, reuse rate and renewal status of IP licensing.

- Product technology landing progress: Landing projects and progress of NPU IP in intelligent computing, data centers, automotive, etc.; cooperation and revenue contribution of Chiplet/small chip-related businesses.

- Profit recovery rhythm: Whether gross margin can stabilize and rise, changes in period expense ratio, impact of impairment and investment income on profits.

- Cash flow improvement: Path and key driving factors for operating cash flow to turn positive, input-output efficiency of capital expenditure and R&D investment.

- [0] Gilin API Data

- [1] Yahoo Finance Hong Kong,

江西铜业大涨与有色金属行业周期可持续性分析

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.