Liren Lizhuang (605136): Analysis of Declining Agency Operation Business and Prospects of Own Brands

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Based on comprehensive data analysis, I will provide a detailed analysis of the declining agency operation business and the development prospects of the own brands of Liren Lizhuang.

Liren Lizhuang is a leading e-commerce agency operator for beauty brands in China, with main businesses including:

- Brand Agency Operation: Providing e-commerce operation, store management, marketing promotion and other services for international beauty brands

- Own Brands: Actively developing its own beauty brand product lines in recent years

- Other Businesses: Covering cross-border e-commerce, brand incubation, etc.

According to the latest financial data [0], the company is facing severe profit challenges:

| Key Financial Indicators | Value | Evaluation |

|---|---|---|

| P/B Ratio | 1.76x | Relatively reasonable |

| P/S Ratio | 2.58x | Valuation pressure exists |

| ROE | -1.34% | Negative shareholder return |

| Net Profit Margin | -1.97% | In loss state |

| Operating Profit Margin | -3.48% | Low operational efficiency |

From the perspective of quarterly performance data [0], the company’s profitability fluctuates greatly:

- Q4 2024: EPS $0.01, Revenue $501.28M (Profitable)

- Q1 2025: EPS -$0.05, Revenue $360.95M (Loss)

- Q2 2025: Continued pressure

- Q3-Q4 2025: Latest quarter EPS -$0.01, Revenue $344.10M [0]

- Revenue scale decreased by 31%compared to Q4 2024 ($501M→$344M)

- Agency operation business faces pressure of brand customer churn

- Intensified industry competition leads to continuous narrowing of gross profit margin

According to industry background analysis, the beauty e-commerce agency operation industry is facing overall challenges [1][2]:

- Brands build their own e-commerce teams: International beauty giants gradually take back e-commerce operation rights

- Platform policy changes: Rise of new e-commerce platforms like Douyin and Kuaishou, impacting traditional Tmall model

- Rising traffic costs: Continuous increase in customer acquisition costs compresses profit margins

- Increased brand concentration: Leading brands have strong bargaining power, squeezing profits of agency operators

Liren Lizhuang has actively cultivated its own brands in recent years, seeking transformation from a service provider to a brand owner:

- Brand incubation: Reverse product customization through data analysis capabilities

- Supply chain integration: Use supplier resources accumulated from agency operations

- Channel synergy: Achieve cold start of new products through agency operation channels

- China’s beauty market scale continues to grow, expected to exceed 1 trillion yuan in 2025 [1]

- Increased consumer acceptance of domestic beauty products

- DTC (Direct-to-Consumer) model reduces channel dependence

- Capital pressure: Own brands require large upfront investments

- Long brand building cycle: Beauty brand cultivation takes 3-5 years

- R&D capabilities need improvement: Still lagging behind leading beauty enterprises

- Inventory risk: Risk of unsold new products after launch

According to DCF valuation model [0], the company’s intrinsic value is significantly lower than the current stock price:

| Valuation Scenario | Intrinsic Value | Premium vs Current Price |

|---|---|---|

| Conservative Scenario | $4.26 | -60.5% |

| Neutral Scenario | $4.77 | -55.8% |

| Optimistic Scenario | $5.72 | -46.9% |

| Weighted Average | $4.92 | -54.4% |

- Negative revenue growth: 5-year CAGR of -21.7% [0]

- Weak profitability: EBITDA margin of only 4.2%

- High capital cost: WACC of 9.1%, debt cost up to 24.4%

- Uncertain growth prospects: Shrinkage of agency operation business, own brands not yet scaled

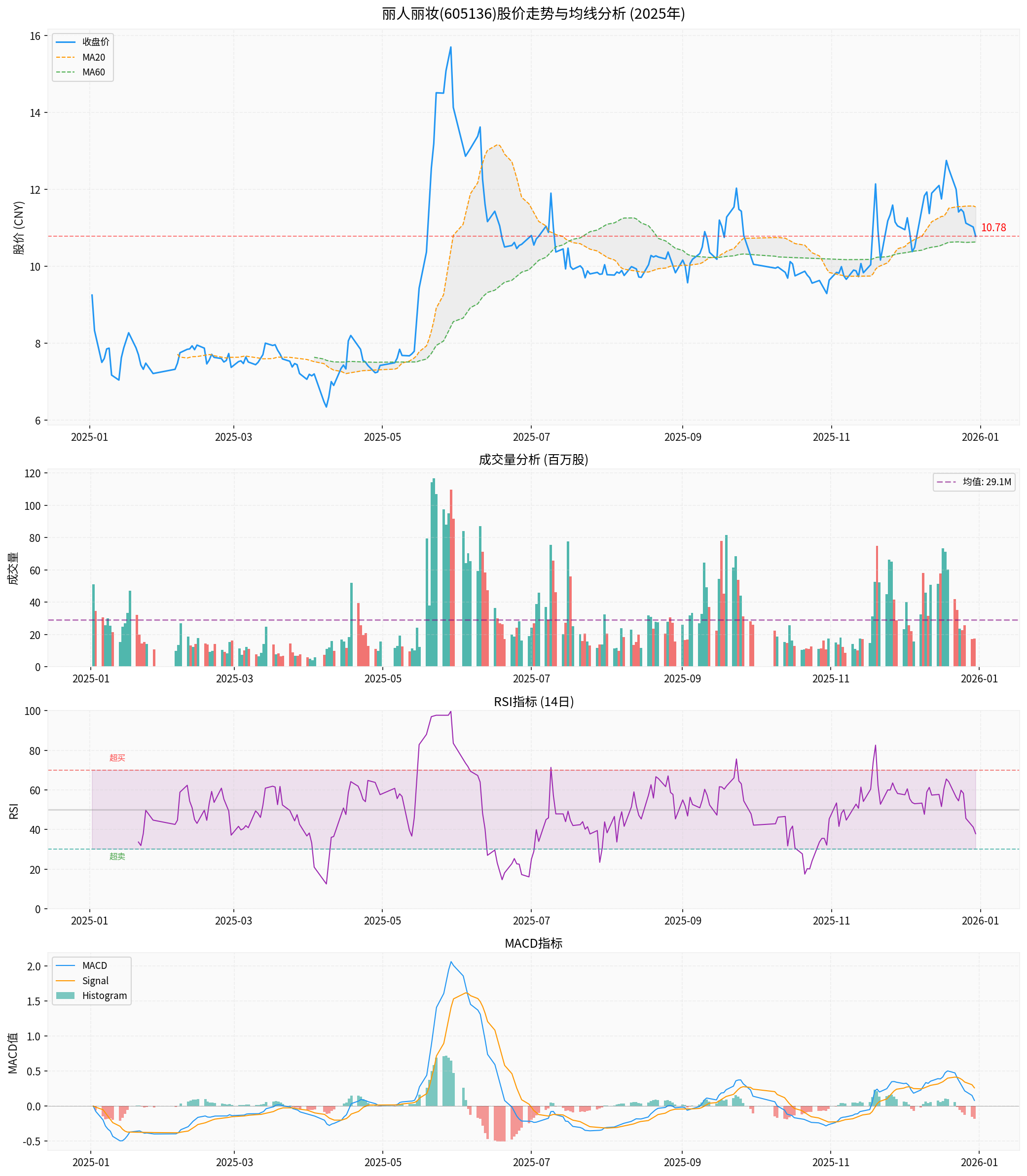

From the perspective of technical analysis [0]:

| Indicator | Value | Signal Meaning |

|---|---|---|

| Stock Price | $10.78 | - |

| 20-day MA | $11.54 | Short-term MA pressure |

| 60-day MA | $10.63 | Mid-term trend weak |

| RSI(14) | 37.89 | Oversold zone |

| MACD | No crossover signal | Weak |

| Beta | 0.66 | Low correlation with market |

###5. Comprehensive Judgment and Risk Tips

####1. Core Conclusions

- Expected to take 2-3 years to form stable revenue

- Success depends on product differentiation and brand building capabilities

- There are capital consumption and inventory risks

####2. Risk Factors

- Business transformation risk: Own brand expansion falls short of expectations

- Liquidity risk: Sustained losses may deplete cash reserves

- Industry policy risk: Tighter e-commerce regulation may affect business model

- Valuation risk: Current P/B of 1.76x lacks support in loss state

####3. Investment Rating Recommendations

- Short-term:Avoid(Performance pressure, high valuation)

- Mid-term:Watch(Monitor own brand development progress)

- Long-term:Pending(Depends on transformation effect)

###6. Data Sources

[0] Gilin API Data - Company financial data, technical analysis, DCF valuation

[1] WWD - “Unicorns Gallop Back on the Beauty M&A Scene in 2025” (https://wwd.com/beauty-industry-news/beauty-features/unicorns-galloped-back-beauty-mampa-scene-2025-1238424140/)

[2] The Business of Fashion - “Proya Misses Sales Estimates, Seeks Hong Kong Listing” (https://www.businessoffashion.com/news/beauty/proya-misses-sales-estimates-seeks-hong-kong-listing/)

南都电源89亿元储能订单及6GWh产能对毛利率影响分析

瑞派宠物医疗投资价值分析报告

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.