2026 Global Investment Strategy and Asset Allocation Recommendations Research Report

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Based on the United Nations’ newly released World Economic Situation and Prospects 2026 and research insights from relevant professional institutions, I will systematically analyze investment strategies and asset allocation recommendations against the backdrop of slowing global economic growth.

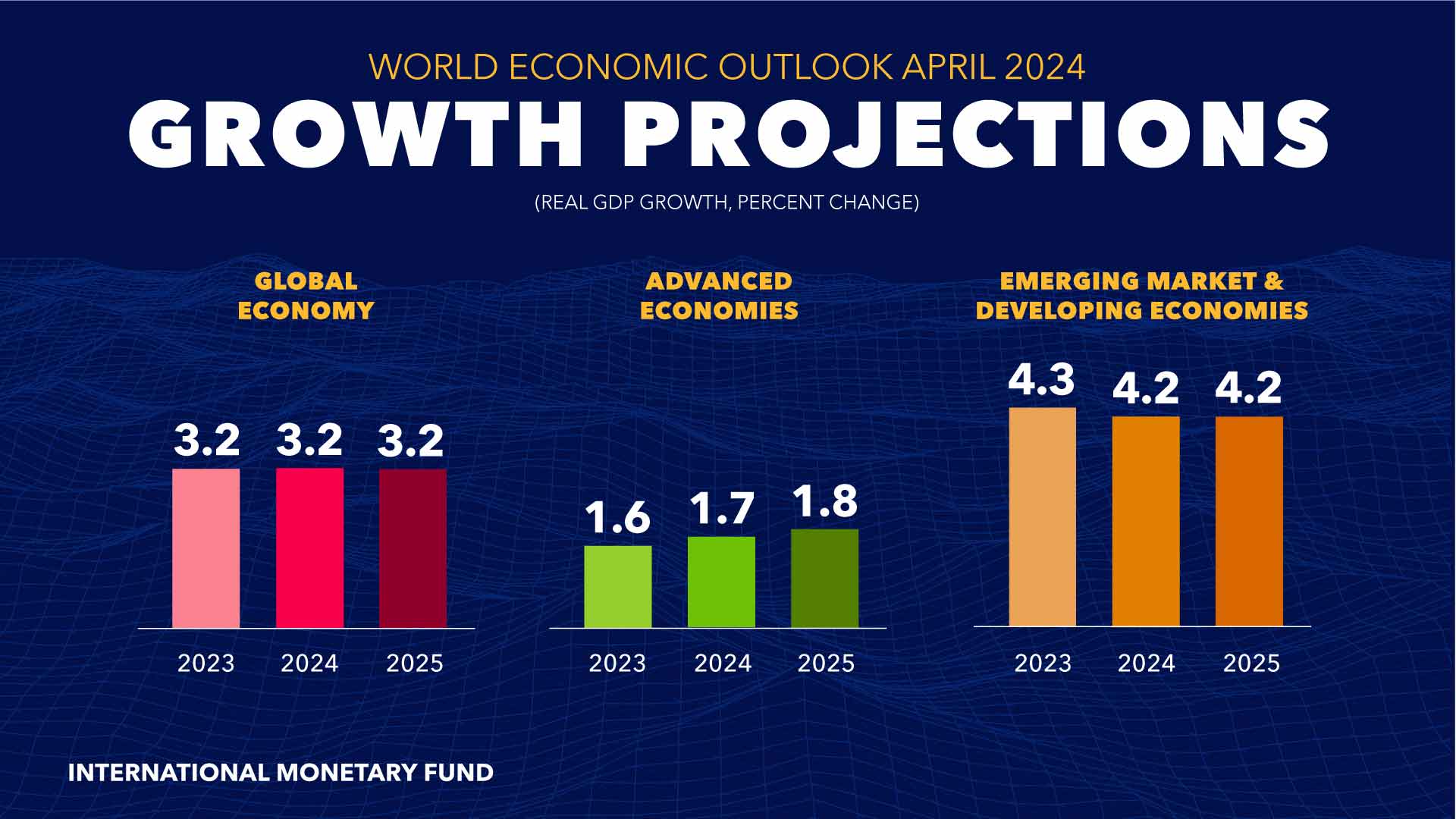

According to the report released by the United Nations on January 8, 2026, global economic growth is showing a continuous slowdown trend. The projected growth rate for 2026 is only 2.7%, a further decline from 2.8% in 2025 [1]. This trend reflects multiple structural challenges:

- Trade Tensions: The WTO projects that global trade volume will grow by only 0.5% in 2026, a sharp slowdown from the 2.4% forecast for 2025 [2]

- Fiscal Pressures: Governments around the world have limited fiscal space, restricting their ability to implement policy stimulus

- Rising Uncertainty: Escalating geopolitical risks and policy divergences have dampened corporate investment willingness

- United States: Projected to grow by approximately 2.0% in 2026, benefiting from the AI investment boom and corporate tax cut policies [3]

- Europe: Growth momentum is weak, with German fiscal stimulus providing partial support, but valuations are already elevated [4]

- Asia: Has become a global growth engine, with divergent performance in markets such as India, China, and Japan [5]

- Emerging Markets: Leveraging the dual advantages of “demographic dividend + critical minerals”, they are attracting capital inflows amid the interest rate cut cycle [6]

Major global central banks have entered the “second half” of the interest rate cut cycle [7]:

- Federal Reserve: Expected to cut interest rates 3-4 times in 2026, with the policy rate range looking to 3.00%-3.25%

- European Central Bank: Will keep interest rates around 2.0%

- Bank of Japan: May raise interest rates slightly due to wage growth pressure

- Emerging Markets: Monetary policy has been eased first, providing support for risky assets

The overall easing of the liquidity environment provides favorable funding conditions for risky assets.

Against the backdrop of slowing economic growth and increasing market differentiation, traditional single-direction or single-asset investment strategies face significant risks. Multiple institutions recommend that investors build more resilient investment portfolios [8]:

| Tier | Proportion | Function | Asset Types |

|---|---|---|---|

| Ballast | 40% | Provides stability and liquidity | Short-term bond funds, bond-like funds, high-dividend blue chips |

| Growth Engine | 45% | Captures trend opportunities | Tech growth, overseas expansion themes, AI industry chain |

| Hedge Satellite | 15% | Hedges tail risks | Gold, safe-haven assets, overseas ETFs |

Both Standard Chartered Bank and Franklin Templeton emphasize that global markets are entering a “desynchronization” phase [9][10]:

- United States (Core Allocation): Stable leading position in innovation, focus on technology, healthcare, and utilities sectors

- Asia (Overweight): Taiwan, Japan, India, South Korea – core beneficiaries of the AI supply chain

- Latin America (Increase Allocation): Mexico, Brazil – direct beneficiaries of supply chain reshoring and the interest rate cut cycle

Data from 2025 shows that emerging markets such as South Korea, Mexico, Brazil, and China have far outperformed the US S&P 500. The decline in cross-market correlations has significantly enhanced the effectiveness of diversified allocation [11].

| Theme | Rationale | Key Industries |

|---|---|---|

AI Industry Trend |

AI investment contributes nearly 1% to GDP, with strong demand for semiconductors | Semiconductors, computing power, edge hardware, AI applications |

“Price Hike Chain” |

Nominal economic recovery and price rebound, cyclical stocks attract incremental capital in the late bull market | Non-ferrous metals, chemicals, new energy |

“Overseas Expansion Chain” |

Globalization of Chinese enterprises opens up profit growth space | Machinery, innovative drugs, power equipment, military industry |

Structural Recovery in Domestic Demand |

Drag from housing prices weakens, structural improvement in consumption | Food & beverage, agriculture, social services, pharmaceuticals |

| Region | Rating | Core Rationale |

|---|---|---|

United States |

Overweight | AI-driven profit growth, strong corporate cash flow, marginal easing of monetary policy |

Asia (Excluding Japan) |

Overweight | Improved earnings and valuation re-rating in India; technology, healthcare, and communications in China |

Europe (Excluding UK) |

Underweight | Elevated valuations, mixed economic data, political uncertainty in France |

Japan |

Underweight | Risk of central bank interest rate hikes, yen appreciation may erode exporters’ profits |

UK |

Underweight | Focus on defensive allocation, performance may lag behind growth-oriented markets |

- One End: High-tech growth sectors – capture AI-driven profit upside potential

- The Other End: High-yield high-quality value stocks – serve as downside protection against uncertainty [15]

| Asset Type | Allocation Recommendation | Core Rationale |

|---|---|---|

Developed Market Investment-Grade Government Bonds |

Core Holding | High credit quality, improved yields, restored diversification function |

Developed Market Investment-Grade Corporate Bonds |

Standard Allocation | Beneficiary of declining yields, but valuations still need attention |

Developed Market High-Yield Bonds |

Cautious | Yields are attractive but issuers need to be carefully selected |

Emerging Market USD-Denominated Government Bonds |

Overweight | Attractive yields, improved credit quality |

Emerging Market Local Currency Government Bonds |

Overweight | Beneficiary of interest rate cuts by various central banks, weakening US dollar |

Asian USD-Denominated Bonds |

Standard Allocation | Moderate yields, low volatility, beneficiary of policy easing |

Given that the Federal Reserve’s interest rate cut magnitude may be lower than market expectations, it is recommended to adjust the duration of USD-denominated bonds to 5 to 7 years to address the risk of increased volatility in long-term bonds [17].

Multiple institutions maintain optimistic expectations for gold [18][19]:

- Medium-Term Target Prices: $4,350 per ounce in 3 months, $4,800 per ounce in 12 months

- Supporting Factors:

- Persistently rising global uncertainty

- Some central banks continue to increase their gold reserves

- Expectations of a weaker US dollar

- Geopolitical risk premium

- Retail investors: 5%-10% of investable assets [20]

- Conservative investors: No more than 20%

- Private Equity: Liquidity premium and improved financing environment make it attractive

- Hedge Funds: Absolute return strategies can hedge market volatility

- Private Credit: High yields but credit risks need attention

- Infrastructure: Long-term structural demand, inflation-linked, increased public capital expenditure

- Digital Assets: Can be allocated in small amounts to enhance portfolio diversification

| Commodity | Strategy | Rationale |

|---|---|---|

Gold |

Overweight | Safe-haven attributes, central bank demand, weaker US dollar |

Silver |

Neutral | Risks of two-way volatility exist |

Crude Oil |

Underweight | Supply surplus limits upside potential |

- Trigger Conditions: Continuous improvement in manufacturing sentiment, sustained rebound in social financing growth

- Response: Increase allocation to pro-cyclical sectors, seize opportunities for beta reversion

- Rebalancing Action: Increase the proportion of the Growth Engine tier

- Trigger Conditions: Macroeconomic data remains in the current pattern, economy stabilizes at a low level but lacks obvious upward momentum

- Response: Maintain the baseline proportion of the three-tier anti-fragile portfolio, keep a balance between the two core themes of technology and overseas expansion

- Rebalancing Action: Quarterly rebalancing, convert volatility into returns

- Trigger Conditions: Market volatility rises sharply and hits the warning range (>35%)

- Response: Reduce irreversible drawdowns, maintain sufficient liquidity

- Rebalancing Action: Increase the proportion of cash and bond funds in the Ballast tier, reduce the risk exposure of the Growth Engine tier, and increase the weight of gold

| Indicator Type | Specific Indicator | Monitoring Frequency |

|---|---|---|

| Macroeconomic Sentiment | Manufacturing PMI | Monthly |

| Credit Expansion | Year-on-year growth rate of outstanding social financing | Monthly |

| Market Status | 20-day annualized volatility of CSI 300 | Monthly |

| Policy Signals | Federal Reserve interest rate resolutions, trade negotiation progress | Event-driven |

| Asset Class | Allocation Direction | Priority | Notes |

|---|---|---|---|

Developed Market Equities |

Overweight the U.S., Asia (excluding Japan) | ★★★★★ | Beneficiary of AI investment and liquidity easing |

Emerging Market Equities |

Overweight India, China, Mexico, Brazil | ★★★★★ | Driven by supply chain restructuring and policies |

Developed Market Bonds |

Standard allocation of investment-grade bonds | ★★★☆☆ | Yields have improved but duration needs attention |

Emerging Market Bonds |

Overweight USD-denominated and local currency bonds | ★★★★☆ | High yields and diversification value |

Gold |

Overweight | ★★★★★ | Safe-haven hedging and central bank demand |

Alternative Assets |

Standard allocation | ★★★☆☆ | Enhances portfolio diversification |

Cash |

Underweight | ★★☆☆☆ | Yields are declining, opportunity cost is rising |

-

Diversification is Unprecedentedly Important: Global markets have entered a phase of “desynchronization”, making it difficult to capture all opportunities with a single country or single asset [23]

-

Active Management is Preferable to Passive Holding: From 2015 to 2025, the annual return gap between the best and worst-performing markets reached 50%-80%, making active allocation critical

-

Balance Growth and Defense: Against the backdrop of slowing economic growth, the barbell strategy (growth + defense) can effectively reduce portfolio volatility

-

Prioritize Tail Risk Hedging: When volatility rises, the hedging value of gold and safe-haven assets becomes prominent

-

Focus on Policy-Driven Opportunities: Fiscal expansion, shifts in monetary policy, and changes in trade policy will bring phased trading opportunities

- Trade Policy Risk: Uncertainty in U.S. trade policy may affect global risk appetite

- Interest Rate Risk: The pace of Federal Reserve interest rate cuts may fall short of expectations, affecting asset pricing

- Geopolitical Risk: The Russia-Ukraine conflict, Middle East situation, China-U.S. relations, etc., may trigger market volatility

- Valuation Risk: Valuations in some markets are already elevated, and attention needs to be paid to whether earnings can be realized

- Liquidity Risk: When market volatility intensifies, portfolio liquidity needs to be maintained

[1] United Nations, World Economic Situation and Prospects 2026, released in New York on January 8, 2026

[2] WTO Global Trade Forecast, October 2025

[3] IMF, World Economic Outlook, October 2025

[4][13][14] Standard Chartered Bank, 2026 Global Market Outlook: Bubble Suspended? Diversify to Prosper, December 2025

[5][9][10] Franklin Templeton, Dina Ting, 2026 Global Equity Market Outlook

[6][12] Mou Yiling, Chief Strategist of Sinolink Securities, 2026 Investment Strategy

[7][17] CITIC Prudential Fund, 2026, Foresee | Fixed Income Chapter, January 7, 2026

[8][22] Hualong Securities, 2026 Macro Asset Allocation Outlook: Bond-like Defense + Tech Offense + Risk Hedging, December 2025

[11][23] Securities Times · Broker China, Save! Ten Brokerage Chiefs Decode 2026 Investment Strategies!, January 5, 2026

[15][18][19] Standard Chartered Bank Wealth Solutions Department, 2026 Investment Strategy Interview

[16][21] Fidelity International, 2026 Global Market Outlook

[20] Wang Lixin, CEO of World Gold Association China, “Gold +” Investment Concept

[17] Fubon Asset Management, 2026 Asset Allocation Key: Non-USD Allocation, December 2025

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.