Analysis of the Impact of the Surge in Demand for AI Learning Tools During Exam Season on the Investment Value of the EdTech Sector

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

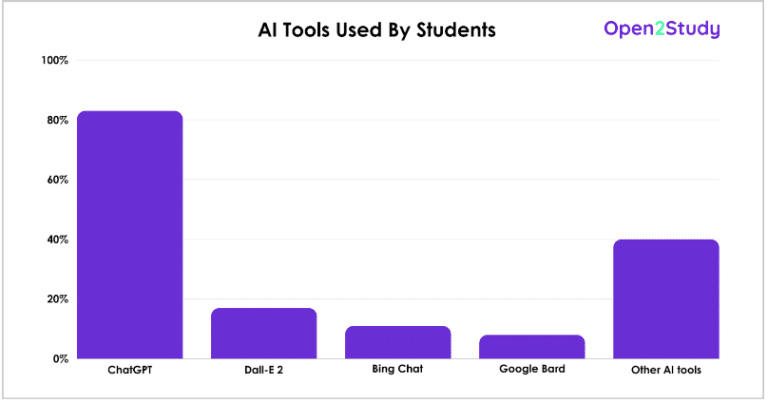

According to the latest market data, as the final review peak in January 2026 arrives, demand for AI learning tools has shown a significant surge. The week-on-week growth rate of learning-related function calls on the Alibaba Qianwen App exceeds 100%, and demand for past exam papers has surged by over 300% in five days [1]. This phenomenon is the first large-scale validation of real demand scenarios for AI education tools in the C-end market, marking that AI technology has found the most down-to-earth “killer application scenario”.

From the perspective of market size, the global AI education market is in a stage of explosive growth. According to data from multiple authoritative research institutions, the global AI education market size was approximately $6.5 billion in 2024, and it is projected to surge to $208.2 billion by 2034, with a compound annual growth rate (CAGR) as high as 41.4% [2]. The Chinese market is growing even more rapidly: the market size of AI+ education is expected to reach nearly 3 trillion yuan by 2030, with a CAGR of about 47% from 2024 to 2030 [3].

The edtech sector has significant seasonal fluctuation characteristics, which are crucial for performance forecasting and valuation analysis.

| Quarter | Time Period | Demand Intensity | Main Scenarios for AI Tool Usage | Investment Implications |

|---|---|---|---|---|

| Q1 | Jan-Mar | High | Spring semester start, final review, wrong question sorting | Demand is strong but disturbed by the Spring Festival |

| Q2 | Apr-Jun | Medium | Spring exams, summer tutoring preparation | Demand driven by exam season |

| Q3 | Jul-Sep | High | Summer learning, fall semester preview | Summer is a golden window period |

| Q4 | Oct-Dec | Extremely High |

Final review, past paper practice | Annual demand peak |

- The demand intensity during the exam season (Q4) reaches the annual peak, which is perfectly confirmed by the data from the Alibaba Qianwen App

- There is a time lag between demand peaks and revenue recognition: prepayments in Q4 are usually recognized in Q1 of the next fiscal year

- Contract liabilities (prepayments) have become a key leading indicator for judging subsequent revenue growth

Edtech companies have obvious seasonal characteristics in revenue recognition. Taking the K12 tutoring industry as an example, training fees collected in advance during the summer vacation are usually recognized in Q3, while prepayments during the exam season may be delayed until Q1 of the following year [4]. This time lag means:

- Q4 financial report data may underestimate the real demand in the current period: The balance of contract liabilities better reflects the actual business prosperity

- Revenue in Q1 of the following year often shows a “good start”: But it is necessary to distinguish between seasonal factors and real growth

- Annual performance needs to be judged comprehensively based on quarterly data: Avoid being misled by single-quarter data

Against the background of seasonal fluctuations, the following indicators better reflect the real growth quality:

| Assessment Dimension | Core Indicator | Judgment Criteria |

|---|---|---|

| User Retention | Ratio of seasonal users converting to long-term users | 30-day retention rate of exam season users |

| Paid Conversion | Change in the proportion of paid users | Difference in conversion rates between off-season and peak season |

| User LTV | Lifetime value per user | Ability to continue paying across multiple semesters |

| Renewal Rate | Renewal rate at the end of the semester | 90% or above is a healthy level |

Take Duolingo as an example: its paid user growth rate has remained above 48%, and it achieved operating revenue of $538 million in the first three quarters of 2024, a year-on-year increase of 42%, while net profit attributable to parent company increased by 1790% year-on-year [4]. This growth quality benefits from AI continuously improving user experience and increasing product payment rates.

The seasonal fluctuations of edtech companies require investors to make corresponding adjustments in valuation:

- Single-quarter PE is easily distorted by seasonal factors

- Annualized forecasts may overestimate or underestimate real profitability

- PEG indicators need to be calculated based on multi-year average growth rates

| Valuation Method | Applicable Scenario | Adjustment Key Points |

|---|---|---|

| CAPE (Cyclically Adjusted PE) | Mature companies | Use 10-year average profit to smooth cycles |

| Revised PEG | Growth companies | Use 3-5 year average growth rate |

| PSR (Price-to-Sales Ratio) | Loss-making or micro-profit companies | Focus on revenue growth rather than profit |

| DCF | Long-term investors | Incorporate seasonal cash flow fluctuations |

Seasonal fluctuations provide layout opportunities for investors:

-

Best entry timing: Q1 off-season (Feb-Mar)

- Post-Spring Festival market sentiment is low

- Q4 performance of the previous year has not fully reflected the demand peak

- Valuation is usually at an annual low

-

Periods to avoid: Exam season (Nov-Dec)

- Short-term gains may overdraw expectations

- Beware of the risk of “good news being fully priced in”

| Indicator | Lead Time | Investment Signal |

|---|---|---|

| Contract Liability Growth Rate | Leads revenue by 1-2 quarters | Growth rate higher than revenue = accelerating growth |

| User Activity (MAU) | Leads revenue by 1 quarter | Can it be maintained after the exam season peak |

| Paid Conversion Rate | Concurrent | Improvement = improved profit quality |

| Customer Acquisition Cost (CAC) | Concurrent | Decrease = improved efficiency |

The surge in demand for the Alibaba Qianwen App during the exam season proves the validity of the following investment logic:

- Scenario authenticity verified: AI+ education is not a false demand, but a real rigid demand scenario

- Payment willingness has formed: Users are willing to pay for efficient learning tools, and the C-end business model is proven viable

- Technical barriers can be established: Question bank resources + AI problem-solving accuracy form a moat

- Broad market space: 30x growth in the global AI education market in 10 years, 47% CAGR in the Chinese market

| Investment Theme | Representative Companies | Core Logic | Risk Warning |

|---|---|---|---|

| AI Education Platforms | DouShen Education, iFlytek | Dual-drive by AI technology + educational content | Risk of technological iteration |

| K12 Tutoring Leaders | Xueda Education, New Oriental-S | Advantages in brand + channels + services | Risk of policy regulation |

| Vocational Education | Fenbi, Zhonggong Education | Rigid demand + increasing concentration | Risk of intensified competition |

| Educational Hardware | Seewo Technology, Hitevision | Synergistic effect of AI + hardware | Risk of compressed hardware gross profit margin |

- Long-term layout: EdTech is a high-quality scenario for AI implementation, and strategic allocation is recommended

- Seasonal timing: Lay out positions in the Q1 off-season, realize gains in the Q4 peak season

- Focus on retention: Prioritize companies with high user retention rates

- Diversify holdings to avoid single-company risk

- Pay attention to changes in policy regulation

- Beware of valuation traps caused by seasonal fluctuations in performance

The surge in demand for AI learning tools during the exam season provides strong validation for the investment value of the edtech sector. Seasonal fluctuations are both a challenge and an opportunity—they increase the complexity of performance forecasts, but also create opportunities for excess returns for investors who are good at seizing timing. Looking ahead to 2025, with the continuous iteration and progress of AI technology and further clarification of education policies, the edtech sector is expected to welcome a “Davis Double Play” of valuation and performance. It is recommended that investors accumulate positions on dips in the Q1 off-season, focusing on high-quality targets with user retention advantages and AI technology barriers.

[1] Sina Finance - “300% Growth in 5 Days! The First Exam Season with AI-assisted Review: Demand for Past Exam Papers on Qianwen Surges” (https://finance.sina.com.cn/stock/t/2026-01-10/doc-inhfvxaf4550788.shtml)

[2] InsightAce Analytic / Research and Markets - AI Education Market Research Report (https://ai-wave.tw/PressCenter/ExpoNewsDetails/faf4ed42-ba3e-4664-9d09-086dd9db2086)

[3] Guosen Securities - “2025 Investment Strategy for the Education Industry” (https://pdf.dfcfw.com/pdf/H3_AP202412291641463250_1.pdf)

[4] Guosen Securities - “Mid-year Report Summary of the Education Sector in 2024” (https://pdf.dfcfw.com/pdf/H3_AP202409271640078459_1.pdf)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.