Analysis of Accelerated Enrollment in Stoke Therapeutics' Dravet Syndrome Drug Trial

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Based on the latest data and announcements, I will provide an in-depth analysis of the impact of accelerated enrollment in Stoke Therapeutics’ Dravet Syndrome drug trial on its pipeline value and market outlook.

According to the official announcement on January 11, 2026, Stoke Therapeutics announced major timeline adjustments for the EMPEROR Phase 3 clinical trial [1]:

| Milestone | Original Planned Time | Updated Time | Impact |

|---|---|---|---|

| Completion of 150-patient enrollment | Originally second half of 2026 | Q2 2026 |

Approximately one quarter ahead of schedule |

| Phase 3 data readout | Second half of 2027 | Mid-2027 |

Approximately 3-6 months ahead of schedule |

| Rolling NDA submission | Second half of 2027 | First half of 2027 |

Significantly advanced |

This accelerated progress indicates that

Zorevunersen is an antisense oligonucleotide (ASO) drug with a unique mechanism that directly targets the genetic cause of Dravet Syndrome by increasing the expression of functional NaV1.1 protein from the wild-type SCN1A gene [2]. This mechanism creates a

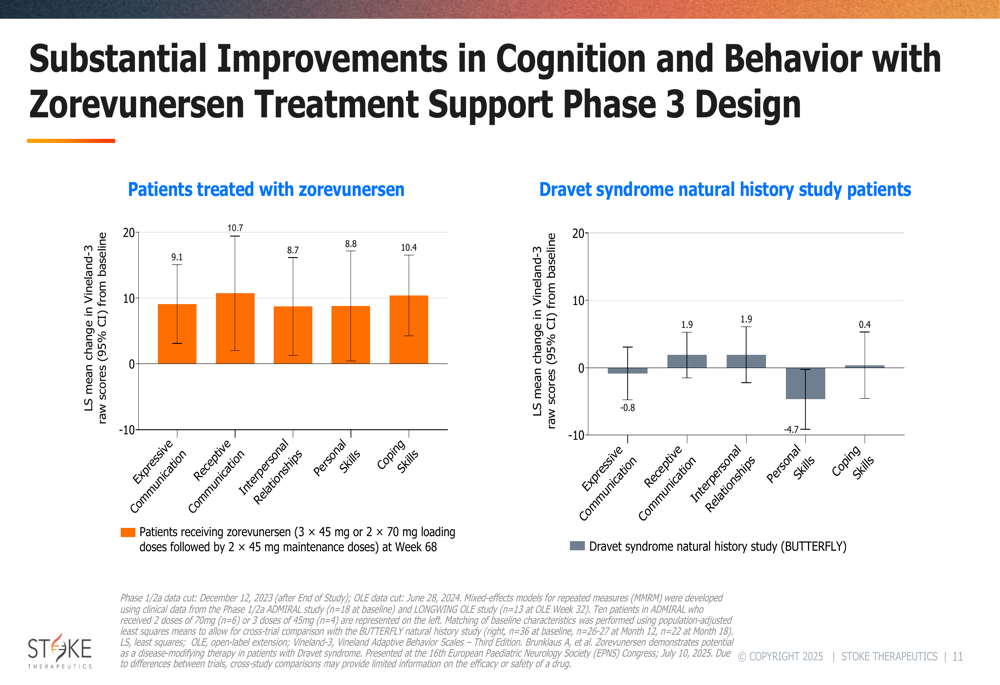

- Disease-modifying potential: Long-term open-label extension (OLE) studies show that 3 years of continuous treatment achieves sustained seizure reduction, along with improved cognition and behavior [3]

- Superior to standard of care: Delivers significant additional reduction in seizure frequency and increase in seizure-free days when added to standard anti-epileptic drugs

| Regulatory Designation | Granting Authority | Value |

|---|---|---|

| Breakthrough Therapy Designation | FDA | Accelerated approval process, priority review |

| Rare Pediatric Disease Designation | FDA | Potential priority review voucher opportunity |

| Orphan Drug Designation | FDA, EMA | Market exclusivity, tax incentives |

In 2025, Biogen acquired global commercialization rights to zorevunersen (excluding the U.S., Canada, and Mexico) with a

- R&D funding support

- Global commercialization capabilities

- Risk-sharing mechanism

According to market research data, the global Dravet Syndrome treatment market is showing steady growth:

- 2024 market size: Approximately $370 million

- 2029 projected market size: Approximately $560 million

- Compound Annual Growth Rate (CAGR): 8.7%-9.4%

The North American market contributes approximately 39% of the growth share, primarily benefiting from higher diagnosis rates and payment capacity [5].

| Drug | Company | Type | Disease-Modifying Potential |

|---|---|---|---|

Zorevunersen |

Stoke/Biogen | ASO Drug | ★★★★★ |

| Epidiolex | GW Pharma | Plant-derived CBD | ★★★★☆ |

| Stiripentol | Generic Drug | Anti-epileptic Drug | ★★★☆☆ |

| Valproate | Generic Drug | Anti-epileptic Drug | ★★☆☆☆ |

| Levetiracetam | Generic Drug | Anti-epileptic Drug | ★★☆☆☆ |

STOK stock has undergone significant revaluation over the past year [0][6]:

| Time Period | Return Rate | Remarks |

|---|---|---|

| 1-Year | +268.27% |

Significantly outperforms the market |

| 6-Month | +176.98% |

Continued strength |

| 3-Month | +8.81% | Upward trend amid fluctuations |

| YTD | +6.31% | Strong start to 2026 |

According to the latest data, analysts hold a

- 12 analysts assigned a Buy rating(80%)

- 3 analysts assigned a Hold rating(20%)

- Consensus target price: $35.50 (8.1% upside from the current price of $32.85)

- Target price range: $28.00 - $50.00

As of January 9, 2026, technical indicators show [7]:

- Price: $32.85

- 50-day moving average: $30.13 (stock price is above the moving average)

- 200-day moving average: $19.19 (significantly below the current price)

- Trend judgment: Sideways consolidation, no clear direction

- Support level: $31.85

- Resistance level: $33.85

Accelerated enrollment directly brings the following risk reduction effects:

- Reduced time risk: Obtain key data earlier, reducing uncertainty during the waiting period

- Reduced patient dropout risk: Reaching the target enrollment count quickly means a shorter overall trial cycle

- Improved operational efficiency: Trial costs are better controlled

Trial acceleration is generally regarded as a

- Earlier catalyst: Investors do not have to wait longer to see key data

- Increased success probability: Enrollment speed exceeding expectations often reflects high trial execution quality

- Increased potential collaboration/acquisition value: Assets closer to commercialization are more attractive

The Dravet Syndrome patient population has long faced limited treatment options. Accelerated enrollment conveys:

- The company’s confidence in the trial’s success

- A proactive response to patient needs

- High willingness to participate among scientists and clinical researchers

| Factor | Description | Impact Level |

|---|---|---|

| First-in-class Potential | First-in-class disease-modifying therapy | ★★★★★ |

| Regulatory Breakthrough Designation | FDA accelerated approval pathway | ★★★★★ |

| Validation from Biogen Collaboration | Endorsement from a major pharmaceutical company | ★★★★☆ |

| Long-term Efficacy Data | Positive 3-year OLE data | ★★★★☆ |

| Growing Market Demand | Expansion of the rare disease market | ★★★★☆ |

| Risk | Description | Impact Level |

|---|---|---|

| Phase 3 Trial Failure | Inherent risk of clinical trials | ★★★★★ |

| Regulatory Approval Delay | Uncertainty in FDA review | ★★★☆☆ |

| Pricing and Reimbursement | Pricing pressure for rare disease drugs | ★★★☆☆ |

| Intensified Competition | R&D of drugs targeting the same mechanism | ★★☆☆☆ |

| Execution Risk | Commercialization capabilities yet to be validated | ★★☆☆☆ |

Current valuation levels [0]:

- Price-to-Earnings (P/E) Ratio: 47.46x (TTM)

- Price-to-Sales (P/S) Ratio: 9.12x

- Price-to-Book (P/B) Ratio: 6.25x

Considering that the company has not yet achieved sustained profitability (latest quarterly EPS: -$0.65) and its main value comes from its clinical pipeline, the valuation premium given by the market mainly reflects investors’ expectations for the success of zorevunersen.

Stoke Therapeutics’ accelerated enrollment for the EMPEROR trial is a

- Increased pipeline value: Accelerated enrollment directly shortens the key data readout timeline, potentially bringing zorevunersen’s commercialization forward by 3-6 months and significantly increasing the pipeline’s net present value.

- Strengthened market position: As a potential first-in-class disease-modifying therapy, zorevunersen’s first-mover advantage in the Dravet Syndrome treatment space is further solidified.

- Enhanced strategic value: The collaboration with Biogen validates the asset’s value, and the accelerated progress increases its potential attractiveness for future collaborations or acquisitions.

- Improved risk-return profile: Enrollment speed exceeding expectations is typically associated with lower trial execution risk, narrowing overall risk exposure.

Investors should pay close attention to the Phase 3 data readout in mid-2027, which will be the most critical catalyst. If the data is positive, the stock price is expected to be revalued upward; if the data is unfavorable, the current valuation will face significant pullback pressure.

[1] Business Wire - “Stoke Therapeutics Announces Updates to Timelines for the Completion of Enrollment and a Phase 3 Data Readout from the EMPEROR Study” (https://www.businesswire.com/news/home/20260111172978/en/)

[2] Biogen Investor Relations - “Biogen and Stoke Therapeutics Present Data that Further Support the Disease-Modifying Potential of Zorevunersen” (https://investors.biogen.com/news-releases/news-release-details/)

[3] Stoke Therapeutics - “Stoke Therapeutics and Biogen Announce Presentations of Clinical Data at 2025 American Epilepsy Society Annual Meeting” (https://investor.stoketherapeutics.com/news-releases/)

[4] PharmaPharma - “Case builds for Biogen, Stoke’s Dravet syndrome drug” (https://pharmaphorum.com/news/case-builds-biogen-stokes-dravet-syndrome-drug)

[5] The Business Research Company - Dravet Syndrome Treatment Market Report 2025

[6] GuruFocus - “Stoke Therapeutics (STOK): New Analyst Price Target Raises to $35” (https://www.gurufocus.com/news/4094331/)

[7] Jinling AI Technical Analysis Data

Report Generation Date: January 12, 2026

Data Sources: Jinling AI Financial Database, Bloomberg, SEC Filings, Company Announcements

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.