贝克休斯Q4 2025财报分析:天然气业务对冲油田服务疲软

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

基于贝克休斯最新财报数据及行业对比分析,我为您提供以下深度投研报告:

贝克休斯于2026年1月25日发布的第四季度财报显示[0][1]:

| 核心指标 | 实际值 | 市场预期 | 超出幅度 |

|---|---|---|---|

| 调整后净利润 | 7.72亿美元 | - | +11% YoY |

| 每股收益(EPS) | 0.78美元 |

0.67美元 | +16.77% |

| 营收 | 73.9亿美元 |

70.7亿美元 | +4.44% |

公司季度营收已连续四个季度实现环比增长,从2025年Q1的64.3亿美元攀升至Q4的73.9亿美元,增幅达

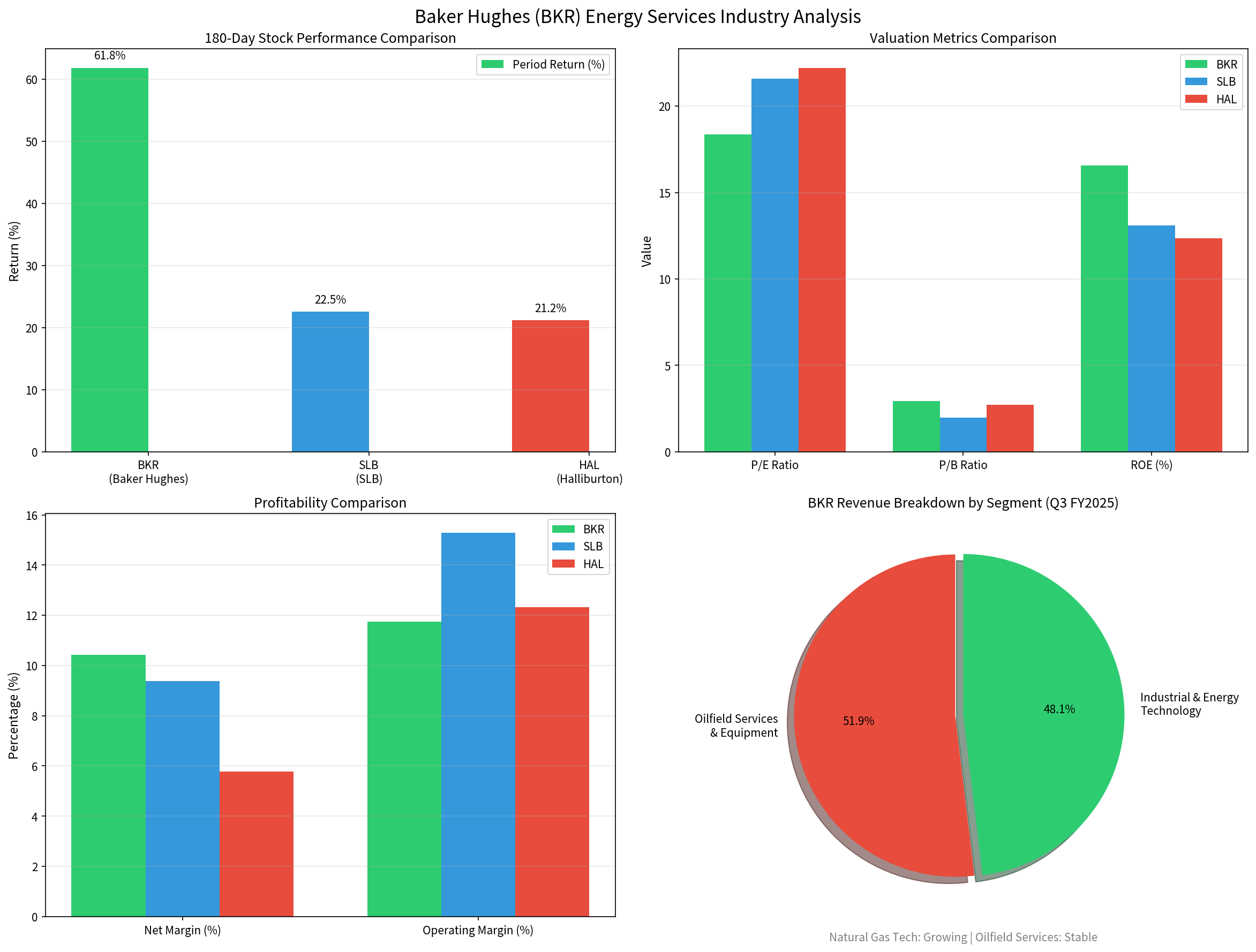

根据Q3 FY2025披露的收入结构[0]:

| 业务板块 | 营收 | 占比 | 业务特征 |

|---|---|---|---|

油田服务及设备 |

36.4亿美元 | 51.9% |

传统业务,受行业周期影响 |

工业及能源技术 |

33.7亿美元 | 48.1% |

天然气技术设备需求强劲 |

贝克休斯的业务结构呈现**"天然气技术+油田服务"双轮驱动**模式,能源技术业务占比接近半数,这使其在传统油田服务疲软时具备较强的对冲能力。

- 美国LNG出口设施扩建:贝克休斯是主要设备供应商

- 中东天然气项目:卡塔尔、沙特等国的天然气开发加速

- 亚洲新兴市场:中国、印度天然气基础设施投资增加

美国钻井活动数据[1][3]显示油气行业仍处于调整期:

| 指标 | 当前 | 一年前 | 变化 |

|---|---|---|---|

| 美国活跃钻机数 | 544台 |

576台 | -5.6% |

| Permian盆地钻机数 | 244台 | 298台 | -18.1% |

贝克休斯的油田服务业务(占营收52%)仍面临

| 维度 | 评估 |

|---|---|

对冲有效性 |

中等偏强(天然气业务占比48%,与油田服务形成互补) |

增长确定性 |

高(LNG需求长期增长趋势明确) |

利润贡献 |

能源技术板块利润率较高,对整体盈利有支撑作用 |

风险敞口 |

仍有52%营收暴露于传统油田服务周期 |

三大能源服务公司核心指标对比:

| 指标 | BKR | SLB | HAL | 行业洞察 |

|---|---|---|---|---|

| 市值 | 531亿美元 | 734亿美元 | 290亿美元 | SLB规模最大 |

| P/E估值 | 18.4x |

21.6x | 22.2x | BKR估值最具吸引力 |

| ROE | 16.6% |

13.1% | 12.3% | BKR股东回报最优 |

| 净利润率 | 10.4% |

9.4% | 5.8% | BKR盈利能力最强 |

| 1年总回报 | +23.5% | +15.5% | +24.6% | BKR回报优秀且稳健 |

| 天然气业务暴露 | 高 |

中 | 低 | BKR最受益于LNG需求增长 |

-

估值优势明显

- BKR当前P/E为18.4x,低于SLB(21.6x)和HAL(22.2x)

- 相比可比公司存在15-20%的估值折价

- 分析师共识目标价55美元,较现价有2.2%上涨空间[0]

-

业务转型红利

- 天然气技术业务占比从五年前的不足30%提升至48%

- 受益于全球能源转型和LNG投资周期

- 德勤预计仅15-25%的美国油气公司能实现营收增长超5%[2],而BKR天然气业务增速显著高于行业平均

-

盈利能力领先

- BKR的ROE(16.6%)、净利润率(10.4%)均为三家公司中最高

- 运营效率持续改善,成本控制能力强

| 风险类型 | 具体因素 | 影响程度 |

|---|---|---|

周期性风险 |

油气价格波动影响资本开支 | 中高 |

地域风险 |

77.5%营收来自海外[0] | 中 |

竞争风险 |

SLB在数字化钻井领域领先 | 中 |

政策风险 |

能源转型政策不确定性 | 低 |

| 策略类型 | 建议 |

|---|---|

仓位配置 |

可作为能源服务板块核心持仓,建议占组合1-3% |

入场时机 |

股价回调至50日均线附近可考虑建仓 |

持有周期 |

中长期(6-12个月),等待天然气业务估值重估 |

对比选择 |

相比SLB和HAL,BKR在当前环境下 风险收益比更优 |

贝克休斯Q4财报展现了其**"天然气技术+油田服务"双轮驱动

从行业角度看,能源服务行业正经历结构性分化:

[0] 金灵API - Baker Hughes公司数据、财报及行业数据 (https://api.jinlingai.com)

[1] GuruFocus - “Baker Hughes (BKR) Reports 11% Increase in Q4 Profits Driven by Natural Gas Demand” (https://www.gurufocus.com/news/8549653/baker-hughes-bkr-reports-11-increase-in-q4-profits-driven-by-natural-gas-demand)

[2] Deloitte - “2026 Oil and Gas Industry Outlook” (https://www.deloitte.com/us/en/insights/industry/oil-and-gas/oil-and-gas-industry-outlook.html)

[3] Investing.com - “Oilfield service company Baker Hughes posts 11% rise in adjusted quarterly profit” (https://www.investing.com/news/commodities-news/oilfield-service-company-baker-hughes-posts-11-rise-in-adjusted-quarterly-profit-4464117)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.