Market Divergence Analysis: Hedge Fund Selling vs Retail Support in 2025 Bull Market

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

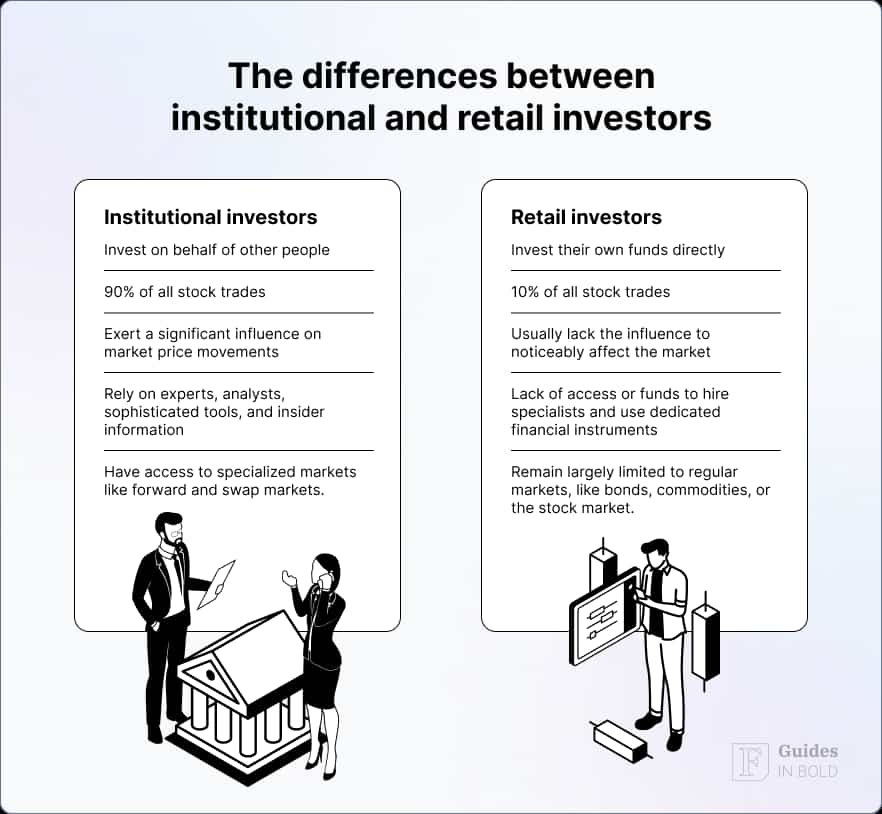

This analysis is based on the CNBC report [1] published on November 13, 2025, which reveals a significant divergence between institutional and retail investor behavior. Hedge funds have unloaded over $67 billion in equities in 2025, becoming the biggest net sellers, while retail investors have emerged as the market’s primary support system. However, emerging data suggests retail enthusiasm may be waning, creating potential market stability concerns.

The market is experiencing an unprecedented split between professional and retail investors. According to Bank of America’s client-flow data, hedge funds and institutional clients have been consistent net sellers throughout 2025, with technology stocks experiencing their biggest institutional selling in two years during the first week of November [1]. This institutional exodus is driven by valuation concerns, with the S&P 500 trading at a P/E ratio of 28.38 and the Nasdaq at 34.31 [0].

Meanwhile, retail investors have been the market’s backbone since 2020, serving as consistent dip-buyers during the three-year bull market [1]. However, Axios reports a significant behavioral shift - retail investors are now “skipping the dip,” departing from their usual pattern of buying during market pullbacks [2]. JPMorgan’s analysis shows retail investors not only scaled back ETF purchases but also turned net sellers in single stocks during recent tech selloffs [2].

The divergence is reflected in recent market performance. On November 13, 2025, major indices showed weakness with SPY closing at $672.04 (-1.66%) and QQQ at $608.40 (-2.04%) [0]. Sector performance reveals significant rotation, with Consumer Cyclical stocks down 2.87%, Energy down 2.16%, and Technology down 1.57% [0]. The worst-performing sectors were Utilities (-3.11%), Consumer Cyclical (-2.87%), and Real Estate (-2.35%), while Consumer Defensive (+0.87%) showed relative strength [0].

Trading volume patterns indicate elevated activity during this institutional selling period, with SPY volume reaching 102.57M (above the 74.02M average) and QQQ volume hitting 69.82M (above the 54.22M average) [0]. The S&P 500 has been relatively flat over the past 30 days (+0.23%) but with increased volatility, ranging from $6,550.78 to $6,920.34 [0].

The current situation represents a potential regime change in market dynamics. For three years, retail investors have provided consistent support during market pullbacks, but their recent “skip the dip” behavior suggests this support system may be deteriorating [2]. Historical patterns indicate that when retail investors stop buying dips, selloffs tend to be longer and larger [2].

The institutional selling appears fundamentally driven rather than technically motivated. Hedge funds’ accelerated selling of technology shares reflects genuine concerns about sky-high valuations [1]. The combination of stretched valuations (S&P 500 P/E of 28.38, Nasdaq P/E of 34.31) and waning retail support creates a precarious market environment [0].

The $67 billion in institutional selling represents a significant withdrawal of professional capital from equities [1]. If retail investors continue to reduce their market participation, the market could face liquidity challenges, particularly in smaller-cap stocks that rely more heavily on retail trading activity.

-

Retail Withdrawal Acceleration: If retail investors continue to “skip the dip,” the market could lose its primary source of support, potentially leading to more severe and prolonged selloffs [2].

-

Valuation Pressure: Current market valuations appear stretched across major indices. Further institutional selling could trigger significant valuation corrections, particularly in technology and growth stocks [0, 1].

-

Liquidity Crunch Risk: The combination of institutional selling and reduced retail participation could create liquidity shortages, especially during periods of heightened volatility.

-

Sector Contagion: While institutional selling has been concentrated in technology, there’s risk it could spread to other sectors, amplifying market weakness.

Decision-makers should track several key indicators for early warning signals:

-

Weekly Retail Flow Data: Monitor whether retail investors return to dip-buying or continue their selling pattern [2].

-

Institutional Positioning Trends: Track whether hedge fund selling accelerates, stabilizes, or reverses [1].

-

Volatility Metrics: Watch for increases in market volatility that could trigger further institutional risk reduction.

-

Sector Rotation Patterns: Monitor whether institutional selling spreads beyond technology into other sectors.

-

Options Market Activity: Track put/call ratios and institutional options positioning for directional sentiment indicators.

The market is experiencing a significant divergence between institutional skepticism and retail fatigue. Hedge funds have sold over $67 billion in equities in 2025, driven by valuation concerns and showing particular focus on technology stocks [1]. Retail investors, who have been consistent market supporters since 2020, are showing signs of fatigue with their “skip the dip” behavior [2]. Current market valuations are elevated (S&P 500 P/E: 28.38, Nasdaq P/E: 34.31) and recent performance shows sector rotation away from growth areas [0]. The combination of institutional selling and waning retail support creates potential market stability concerns that warrant close monitoring of flow data, volatility metrics, and sector performance patterns.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.