辉瑞(PFE) 2026年业绩指引深度分析报告

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

基于以上全面分析,我将为您提供关于辉瑞(PFE) 2026年业绩指引可行性的深度投研报告。

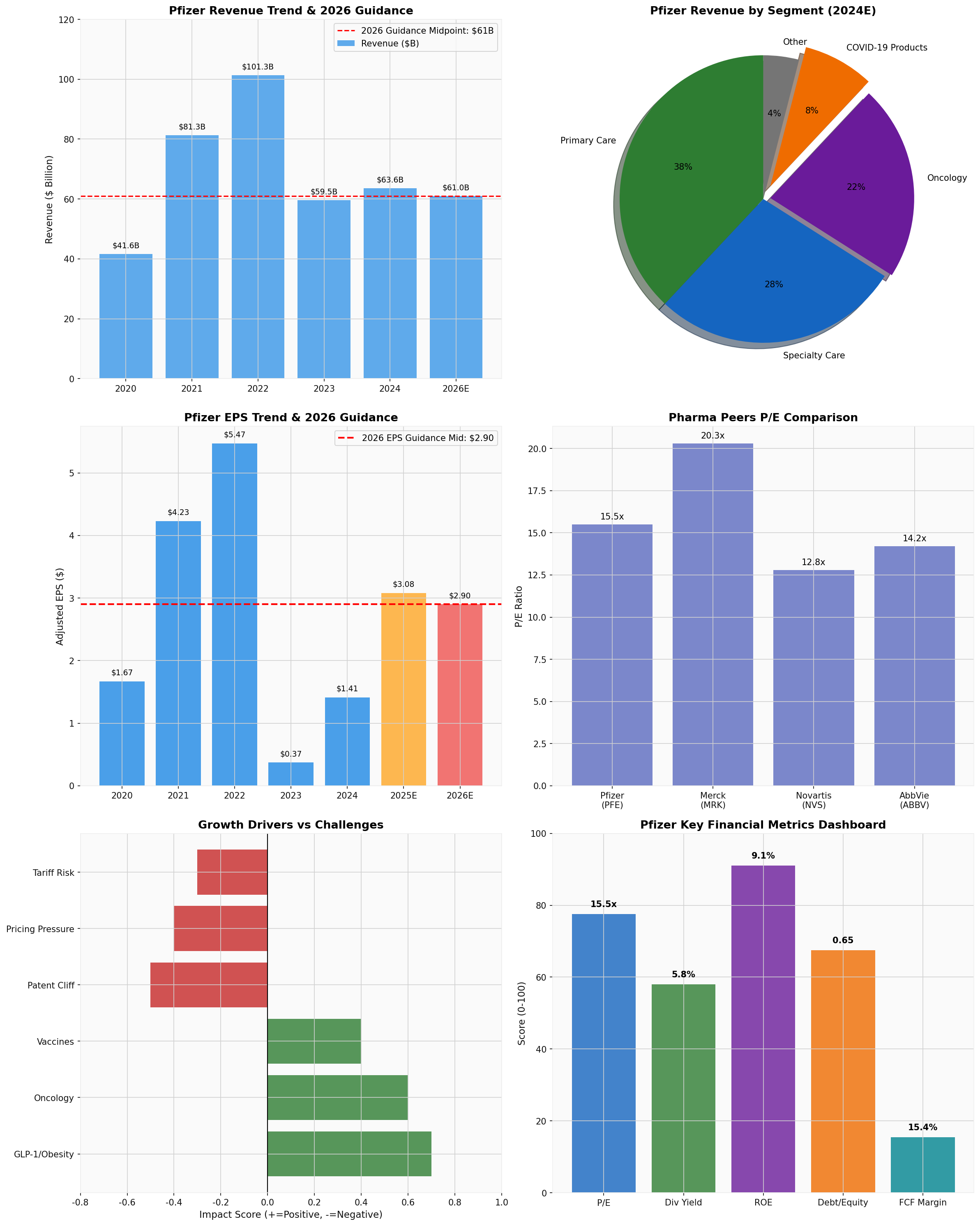

| 指标 | 指引区间 | 中点值 | 同比变化 |

|---|---|---|---|

营业收入 |

$595-625亿 | $610亿 | 约-4% |

调整后每股收益 |

$2.80-$3.00 | $2.90 | 约-6% |

Covid-19产品收入 |

约$50亿 | - | 持续下降 |

公司2024年第四季度实现营收175.6亿美元,调整后每股收益0.66美元,

辉瑞正经历"后疫情时代"的显著营收回落:

| 财年 | 营收(亿美元) | 同比变化 | 净利润(亿美元) |

|---|---|---|---|

| 2022 | $1,012.8 | +24% | $313.7 |

| 2023 | $595.5 | -41% | $21.2 |

| 2024 | $636.3 | +7% | $80.3 |

| 2026E | $610.0 | -4% | ~$60(估算) |

- 2022年营收峰值主要来自Covid-19疫苗(约378亿)和口服药(约189亿)[0]

- 2023年营收"断崖式下跌"标志着疫情红利的终结

- 2024年有所企稳,但距离疫情前水平仍有差距[0]

| 指标 | 数值 | 解读 |

|---|---|---|

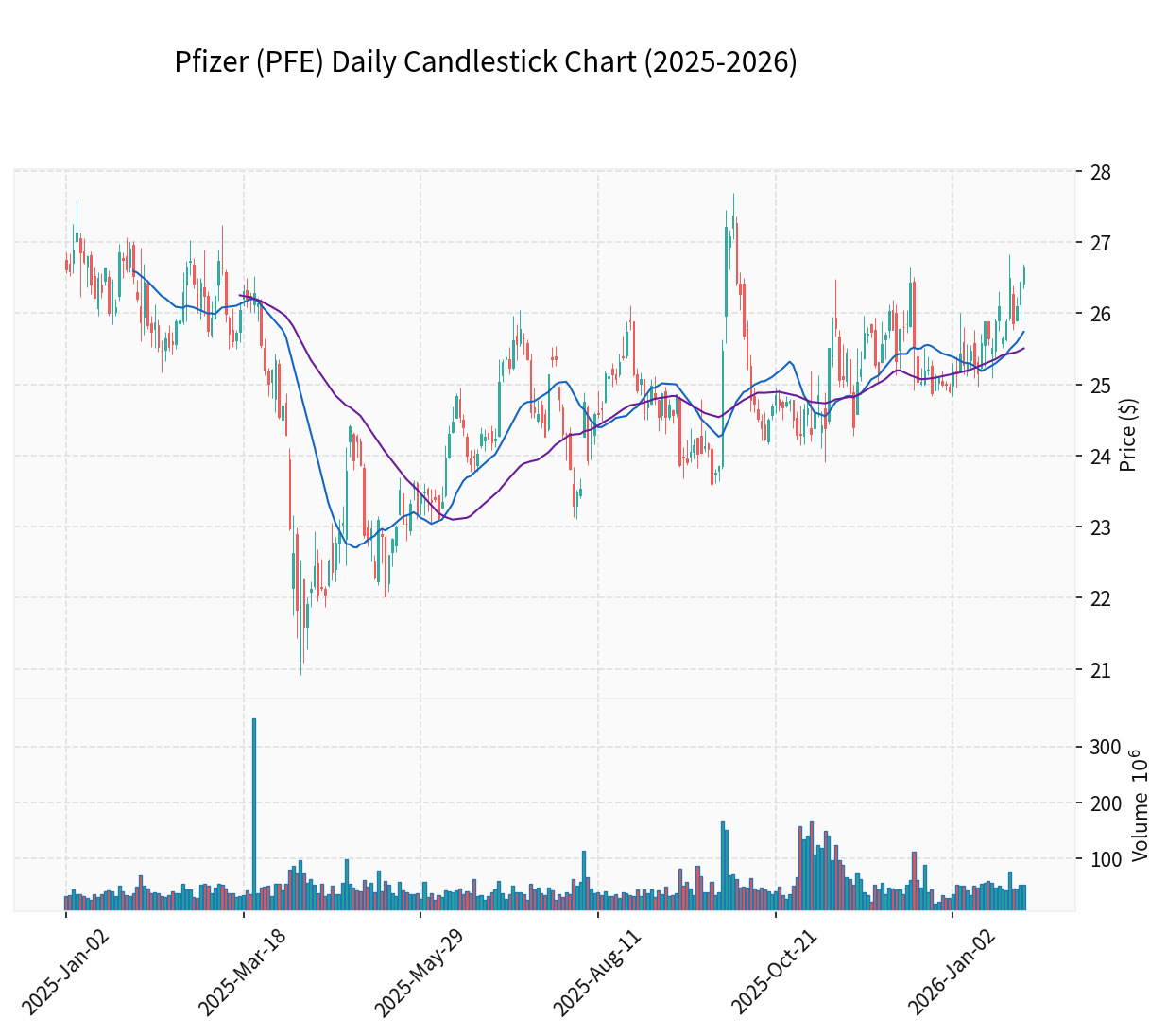

| 当前价格 | $26.66 | - |

| 52周区间 | $20.92-$27.69 | 接近区间低位 |

| 距52周高点跌幅 | -3.7% | - |

| P/E估值 | 15.5x | 低于历史均值 |

| 股息率 | 5.8% | 具有吸引力 |

2024年第四季度财报显示,辉瑞非Covid-19产品表现稳健,老年疾病药物需求强劲,部分抵消了Covid产品的下滑[1][2]。

- 肿瘤学产品成为核心增长引擎

- Specialty Care和Oncology业务在Q4分别实现增长,抵消了Primary Care 11%的下滑[4]

- 并购整合协同效应逐步显现

辉瑞最新收购的Metsera公司在研GLP-1药物显示出优异疗效:

- 每月一次给药的减肥注射剂在中期研究中减重达10.5%[5][6]

- 体重下降最高达12%[7]

- 有望在竞争激烈的减肥药市场分一杯羹

- 当前股息率约5.8%,在制药行业中处于较高水平

- 稳定的分红政策对长期投资者具有吸引力

- 2026年面临约$16亿美元的专利到期影响[3]

- 仿制药竞争将侵蚀部分核心产品收入

- 美国药价谈判政策带来的不确定性

- 政府压价压力可能影响整体毛利率

- 特朗普政府关税政策可能对制药行业产生影响

- 供应链成本可能上升[8]

- 市场预期2026年营收约$625亿,公司指引中点$610亿

- EPS指引$2.80-$3.00低于市场预期的$3.06[9]

| 情景 | 内在价值 | 相对当前价格 |

|---|---|---|

| 保守情景 | $136.15 | +410.7% |

| 中性情景 | $144.28 | +441.2% |

| 乐观情景 | $308.17 | +1055.9% |

概率加权价值 |

$196.20 |

+635.9% |

- 营收增长率:11.2%(历史5年均值)

- EBITDA利润率:31.0%

- WACC:6.4%

- Beta系数:0.44

| 公司 | P/E | 股息率 | 特点 |

|---|---|---|---|

辉瑞(PFE) |

15.5x | 5.8% | 低估值、高股息 |

| 默克(MRK) | 20.3x | 2.4% | 肿瘤药增长强劲 |

| 诺华(NVS) | 12.8x | 3.5% | 专注创新药 |

| 艾伯维(ABBV) | 14.2x | 3.9% | 专利危机缓解 |

从"疫情受益者"向"多元化制药巨头"转型

├── Primary Care (38%) → 保持稳定,重点发展心血管、代谢疾病

├── Specialty Care (28%) → 高增长领域,重点发力罕见病、免疫

├── Oncology (22%) → 核心增长引擎,持续加大投入

├── COVID-19 Products (8%) → 常态化,但规模大幅收缩

└── Other (4%) → 辅助业务

2024年R&D支出约$108亿美元,持续推进:

- 肿瘤免疫疗法

- 罕见病基因治疗

- 下一代疫苗技术

- 口服GLP-1药物开发

辉瑞通过战略性收购补充管线:

- $43亿收购Seagen(2023年)→ 强化肿瘤学管线

- 收购Metsera(2024年)→ 切入GLP-1减肥药赛道[5][6]

- 裁减冗余岗位,优化运营结构

- 提高生产效率,降低COGS

- 控制SI&A支出

| 维度 | 评级 | 说明 |

|---|---|---|

短期(1-6月) |

⚠️ 观望 | 营收指引低于预期,面临多重逆风 |

中期(6-12月) |

📈 关注 | GLp-1数据、业绩改善信号 |

长期(1-3年) |

⭐ 看好 | 估值具有吸引力,业务转型成效待显现 |

- GLP-1减肥药临床进展(2026年关键看点)

- 肿瘤学产品获批上市

- 成本削减计划执行

- 股息稳定增长

| 情景 | 目标价 | 隐含涨幅 |

|---|---|---|

| 保守 | $32 | +20% |

| 中性 | $40 | +50% |

| 乐观 | $55 | +106% |

✅ 现有非Covid产品组合保持韧性

✅ 肿瘤学和特药业务持续增长

✅ 高股息率提供估值支撑

✅ 成本优化措施持续推进

⚠️ 专利悬崖(-$16亿)

⚠️ 药物定价政策不确定性

⚠️ 关税政策潜在冲击

⚠️ 营收指引低于市场预期

辉瑞正从"疫情红利驱动"向"创新药驱动"转型,核心增长动力包括:

- 肿瘤学管线:通过Seagen收购获得强大ADC技术平台

- GLP-1减肥药:切入千亿级市场,空间巨大

- 疫苗业务:呼吸道疫苗、流感疫苗等常规疫苗稳定增长

- 成本效率提升:运营杠杆改善利润率

[0] Pfizer Inc. Form 10-K Filing (SEC EDGAR, 2025-02-27) - https://www.sec.gov/Archives/edgar/data/78003/000007800325000054/pfe-20241231.htm

[1] Bloomberg - “Pfizer Beats Sales Estimates on Demand for Older Drugs” (2026-02-03) - https://www.bloomberg.com/news/articles/2026-02-03/pfizer-beats-sales-estimates-on-demand-for-older-drugs

[2] Investing.com - “Pfizer fourth-quarter revenue beats estimates despite year-on-year decline” (2026-02-03) - https://www.investing.com/news/earnings/pfizer-fourthquarter-revenue-beats-estimates-despite-yearonyear-decline-4481354

[3] Seeking Alpha - “Pfizer projects annual revenue decline amid $1.6B hit from patent cliffs” (2026-02-03) - https://seekingalpha.com/news/4546119-pfizer-stock-slips-q4-2025-results

[4] Seeking Alpha - “Pfizer in Charts: Specialty Care and Oncology offset 11% Y/Y drop in Primary Care revenue in Q4” (2026-02-03) - https://seekingalpha.com/news/4546106-pfizer-in-charts-specialty-care-and-oncology-offset-11-yy-drop-in-primary-care-revenue-in-q4

[5] CNBC - “Pfizer says obesity injection shows promise as monthly treatment in mid-stage trial” (2026-02-03) - https://www.cnbc.com/2026/02/03/pfizers-monthly-obesity-injection-drove-shows-promise-in-trial.html

[6] Endpoints News - “Pfizer’s Metsera-originated monthly GLP-1 cuts weight by 10.5% at six months” (2026-02-03) - https://endpoints.news/pfizers-metsera-originated-monthly-glp-1-cuts-weight-by-10-5-at-six-months/

[7] Seeking Alpha - “Pfizer posts trial data obesity therapy” (2026-02-03) - https://seekingalpha.com/news/4546086-pfizer-posts-trial-data-obesity-therapy

[8] MarketWatch - “Pfizer says once-a-month weight-loss drug works as it forecasts profit decline” (2026-02-03) - https://www.marketwatch.com/story/pfizer-says-once-a-month-weight-loss-drug-works-as-it-forecasts-profit-decline-5c16ffa4

[9] Nasdaq - “Pfizer Revises Annual Revenue Guidance Below View, Backs Profit Expectations; Initiates 2026 Outlook” - https://www.nasdaq.com/articles/pfizer-revises-annual-revenue-guidance-below-view-backs-profit-expectations-initiates-2026

报告生成时间:2026年2月3日

数据来源:金灵AI金融分析平台、SEC文件、主流财经媒体

免责声明:本报告仅供参考,不构成投资建议

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.