Michael Burry Challenges Big Tech Earnings Quality Through Depreciation Accounting Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis examines Michael Burry’s recent critique of Big Tech accounting practices, specifically focusing on depreciation schedule extensions for AI infrastructure. On November 14, 2025, at 9:49 AM EST, Burry questioned whether major technology companies are artificially inflating earnings through aggressive accounting adjustments [1][2][3].

The technology sector exhibited mixed responses to Burry’s concerns:

- Meta (META): $611.49 (+0.26%) - significantly underperforming with only 4.2% gains in 2025 versus 19% for Nasdaq 100 [0][1]

- Alphabet (GOOGL): $277.83 (-0.27%) - strong performer with 47% year-to-date gains [0][1]

- Microsoft (MSFT): $509.54 (+1.24%) - up nearly 20% in 2025 [0][1]

- Amazon (AMZN): $237.49 (-0.04%) [0]

- Nasdaq Composite: +2.24% to 23,049.58, showing recovery from recent volatility [0]

- S&P 500: +1.47% to 6,770.22 [0]

- Dow Jones: +0.26% to 47,347.07 [0]

The divergent performance suggests investors are already pricing different levels of accounting risk across Big Tech names, with Meta facing the most skepticism despite its relatively modest gains compared to peers [1].

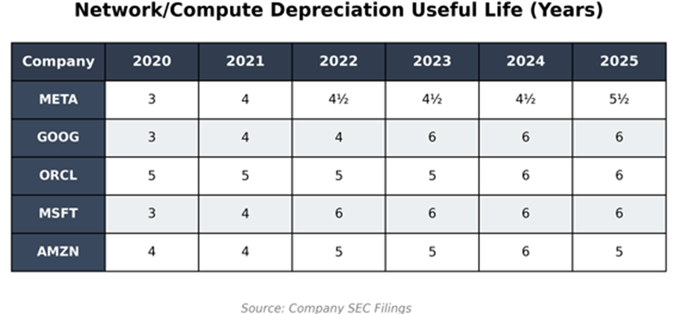

- Meta extended useful life estimates from 4-5 years to 5.5 years, reducing 2025 depreciation by $2.9 billion [1]

- Alphabet extended server useful life from 3 to 6 years [3]

- Oracle extended from 5 to 6 years [3]

- Microsoft made similar extensions in recent years [1]

- Estimated $176 billion understatement of depreciation across major tech companies from 2026-2028 [2][3]

- Oracle could overstate earnings by 26.9% by 2028 [2][3]

- Meta could overstate earnings by 20.8% by 2028 [2][3]

Despite these accounting changes, combined depreciation costs for Meta, Alphabet, and Microsoft rose from $10 billion in Q4 2023 to nearly $22 billion in Q3 2025, projected to reach almost $30 billion by next year [1].

- Tech companies claim they’re extracting more value from equipment through software optimization and efficiency improvements [1]

- Microsoft CEO Satya Nadella emphasized continuous modernization and enhanced productivity [1]

- Notably, Amazon actually shortened server equipment life to 5 years from 6 years, demonstrating different approaches [1]

- Critics argue rapid chip innovation should accelerate depreciation, not extend it [1]

- Questions remain about whether extended useful lives are technically justified for AI hardware

- The debate reflects broader concerns about AI investment sustainability and return expectations [1]

Despite accounting concerns, Magnificent Seven earnings are still projected to grow 27% YoY, nearly double initial 14% expectations [1]. This creates a complex narrative where aggressive accounting may be masking both genuine growth and potential overinvestment risks.

Burry’s reputation from successfully predicting the 2008 housing crisis gives his warnings significant weight in the investment community [1][2]. His promised “more detail coming November 25th” adds anticipation for additional disclosures that could trigger meaningful sector revaluation [2].

- If Burry’s calculations are accurate, earnings quality at major tech companies may be significantly lower than reported [2][3]

- Potential for earnings restatements if regulatory scrutiny increases

- Divergent accounting practices could create misleading comparisons between companies

- High-growth expectations may be vulnerable to accounting-related disappointments

- Growing skepticism about AI investment returns could trigger broader tech sector rotation

- Current high valuations depend on continued earnings growth that may be artificially inflated

- The controversy could accelerate investor focus on free cash flow rather than reported earnings

- November 25th: Burry’s promised additional details [2]

- Upcoming Earnings Season: How companies address these concerns in quarterly reports

- Regulatory Response: Any SEC or FASB commentary on tech depreciation practices

- Depreciation expense trends relative to capital expenditures

- Free cash flow conversion rates as an alternative earnings quality measure

- Return on invested capital for AI infrastructure investments

- Hardware replacement cycles and actual useful life data

The controversy centers on whether Big Tech companies are using aggressive depreciation accounting to mask the true cost of massive AI infrastructure investments. While companies defend the changes as reflecting improved equipment efficiency, the timing coincides with unprecedented AI capital spending, raising questions about earnings sustainability.

Investors should note that even with extended depreciation schedules, actual depreciation costs are still rising significantly - from $10 billion quarterly to nearly $22 billion - indicating massive ongoing infrastructure investment regardless of accounting treatment [1].

The divergent market reactions, particularly Meta’s underperformance, suggest sophisticated investors are already differentiating between companies based on perceived accounting quality and AI investment efficiency. The situation warrants close monitoring of Burry’s upcoming disclosures and any regulatory responses that could impact sector valuations.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.