Retirement Portfolio Strategy: Bond Allocation Recommendations Amid Equity Recency Bias

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

The MarketWatch article published on February 5, 2026, presents a compelling case for increasing bond allocations among investors approaching retirement, grounded in both behavioral finance principles and current market conditions [1]. The central thesis addresses a critical phenomenon: recency bias distorts risk perception among retirees following extended bull markets, leading potentially dangerous overconfidence in equity holdings.

The current market environment presents a unique convergence of factors that make this guidance particularly relevant. The S&P 500 has generated an exceptional 88% total return over the past three years, while simultaneously trading at $6,820.99 with a modest year-to-date decline of -0.83% [0]. This mixed backdrop—strong historical performance but current uncertainty—creates the precise conditions where investors may becomecomplacent about equity risk precisely when vigilance is most needed.

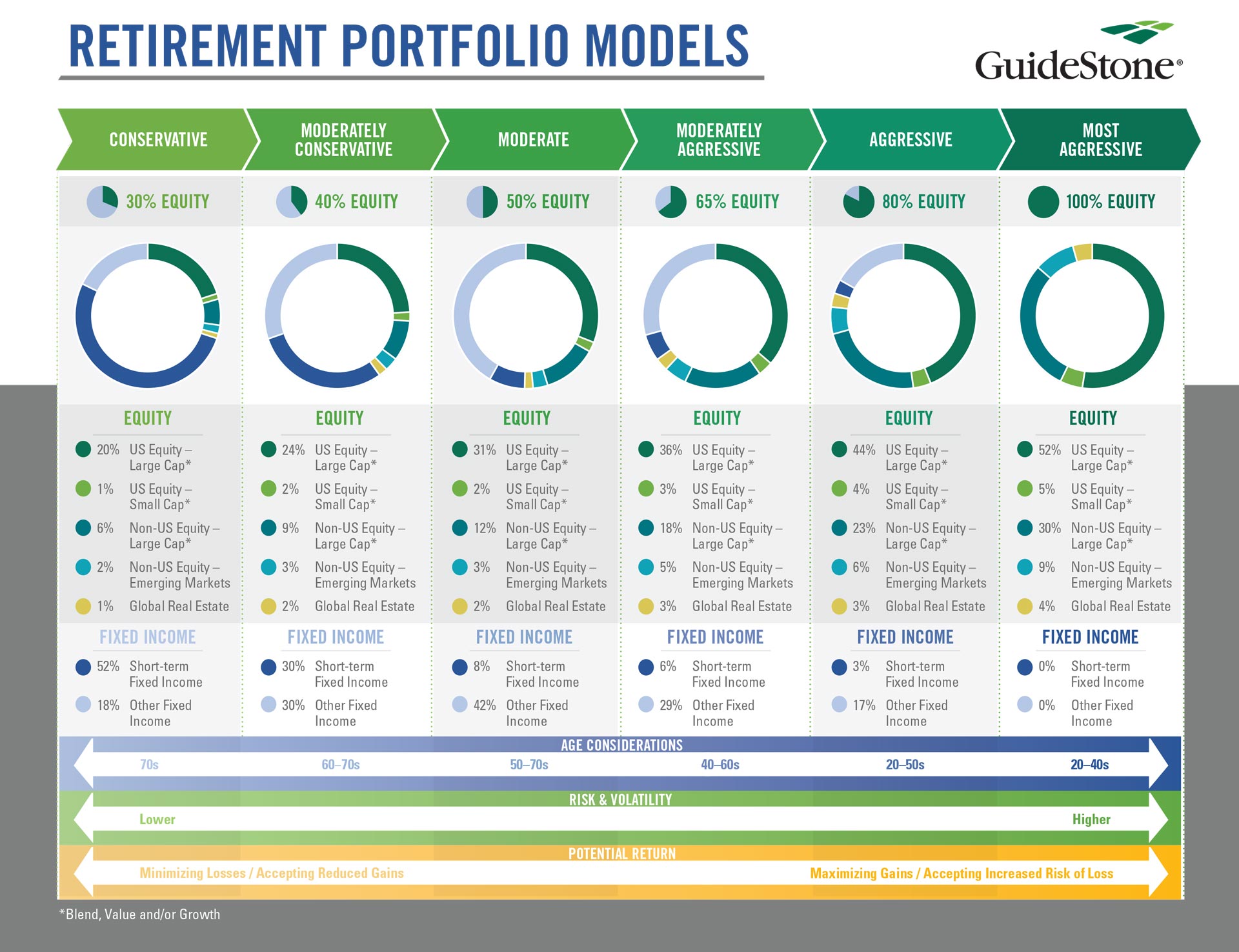

Investors aged 55-64 currently hold an average of 64% of their portfolios in stocks according to Vanguard’s “How America Saves” report [1]. This concentration has likely intensified following the recent bull market, as strong returns naturally attract greater equity allocation through both intentional increases and passive appreciation. The article argues this represents a significant departure from prudent risk management principles for individuals with limited time horizons to recover from potential market downturns.

The bond market valuation opportunity emerges from a contrarian perspective: bonds are currently “out of fashion” with suppressed demand, which historically signals undervaluation [1]. Veteran Treasury bond manager Van Hoisington identifies eight indicators pointing toward declining inflation, including slowing economic growth, rising labor-market slack, stagnant real wages, AI-induced disinflationary pressures, job cuts in manufacturing sectors, tariff-driven economic headwinds, declining commodity prices, and reduced consumer spending momentum. If these indicators prove accurate, bond prices could appreciate in addition to providing current yields ranging from 3.8% for 5-Year Treasuries to 6.7% for high-yield corporate bonds [1].

The February 5, 2026 MarketWatch analysis provides retirement-focused investors with a framework for evaluating current portfolio allocations against historical risk patterns and contemporary market conditions. The core recommendation to increase bond allocations reflects both behavioral concerns—addressing recency bias that may cause retirees to underestimate equity risk—and fundamental factors including attractive current yields and potential inflation-decline indicators that could benefit bond prices.

Current bond market yields span a meaningful range: 5-Year Treasuries at 3.8%, 10-Year Treasuries at 4.3%, BAA-rated corporate bonds at 5.9%, high-yield bonds at 6.7%, and TIPS offering inflation protection of 1.2% to 2.6% above inflation [1]. This yield spectrum provides retirees with options to tailor fixed-income allocations to their specific risk tolerance and income requirements while maintaining portfolio diversification benefits.

The historical context provided—negative real equity returns occurring in roughly one-quarter of five-year periods—underscores the importance of sequence-of-returns risk for retirees. The current market environment, characterized by modest equity declines, mixed sector performance, and defensive sector weakness, reinforces the article’s timeliness by demonstrating that equity markets do not always align with retiree preferences for capital preservation and predictable income generation.

Implementation guidance emphasizes tax-advantaged account placement for bonds, low-cost diversified vehicle selection, and disciplined rebalancing practices. The analysis acknowledges competition from annuity products offering higher guaranteed returns while noting the liquidity and flexibility trade-offs involved. Investors should evaluate these alternatives against their individual circumstances, including health status, family longevity history, and flexibility requirements for unexpected expenses or changing needs.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.