InvestorPlace Bullish Thesis: Economic Acceleration and Small-Cap AI Rotation Outlook

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

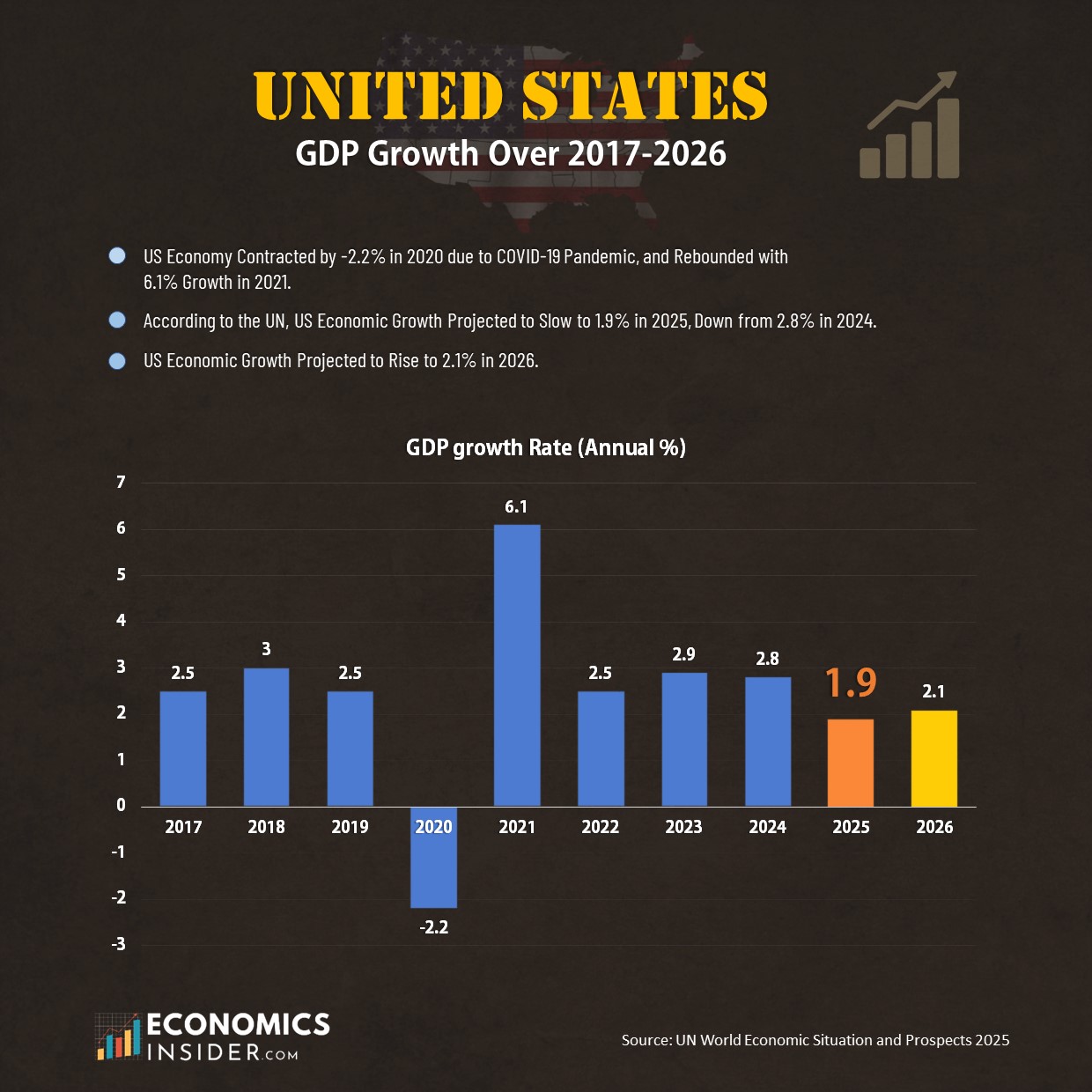

The InvestorPlace analysis arrives at a moment when U.S. economic data demonstrates meaningful acceleration, providing substance to the bullish thesis. Q3 2025 GDP growth of 4.4% annualized represents a notable pickup from 3.8% in Q2, while consumer spending maintains a robust 3.5% annual growth rate—indicating continued household sector resilience despite ongoing concerns about inflation and interest rates [1]. The author projects U.S. GDP could reach 6% in the second half of 2026, an aggressive forecast that would require sustained momentum across multiple economic sectors and favorable policy conditions.

Today’s market data (February 5, 2026) presents a more nuanced picture. All major indices recorded declines: S&P 500 closed at 6,798.39 (-0.57%), NASDAQ at 22,540.59 (-0.28%), Dow Jones at 48,908.73 (-0.68%), and Russell 2000 at 2,577.65 (-1.11%) [0]. This broad-based pullback illustrates the “noise” the article acknowledges investors must navigate, even when underlying economic fundamentals support a constructive stance. The Technology sector’s resilience (+0.46%) as the sole positive performer aligns with the AI-focused thesis, while economically sensitive sectors like Basic Materials (-2.49%) and Consumer Cyclical (-1.81%) experienced sharper declines [0].

The Russell 2000’s 7% January gain significantly outperformed the S&P 500 (+1.4%) and Dow Jones (+1.6%), providing empirical support for the rotation hypothesis described in the article [1]. This small-cap outperformance suggests capital is indeed beginning to shift toward companies that may benefit from AI infrastructure buildout and related supply chain opportunities—areas where smaller, more specialized firms often maintain competitive positioning. The rotation dynamic, if sustained, could represent a meaningful trend shift from the large-cap dominance that characterized much of the 2023-2025 period.

The “AI Dislocation” framework proposed by the author suggests the next phase of artificial intelligence adoption will favor smaller companies over the mega-cap technology leaders that drove initial AI enthusiasm. This thesis posits that as AI deployment expands beyond hyperscale cloud providers into broader enterprise and industrial applications, demand will flow toward companies providing specialized hardware, software, and services at lower price points and with greater customization capabilities. The January small-cap strength may represent early validation of this narrative, though today’s Russell 2000 decline (-1.11%) demonstrates that rotation dynamics remain subject to short-term volatility [0][1].

Several factors support the article’s constructive stance. The acceleration in GDP growth from Q2 to Q3 2025 provides tangible evidence of economic momentum, while consumer spending resilience indicates household balance sheets remain fundamentally sound. The Technology sector’s continued outperformance—today’s only positive sector at +0.46%—suggests investor appetite for AI-related exposure persists despite valuation concerns [0]. The historical pattern of economic accelerations often coinciding with equity market advances provides additional context for the bullish thesis.

However, significant caveats warrant attention. The article functions primarily as teaser content for a separate paid briefing, directing readers toward an “AI Dislocation” research product without disclosing specific stock recommendations in the public article [1]. This promotional structure raises appropriate questions about objectivity and should inform how investors weight the analysis. The 6% GDP forecast for H2 2026 is aggressive and contingent on multiple variables—including Federal Reserve policy trajectory, global economic conditions, and the pace of AI infrastructure investment—that introduce substantial uncertainty. The speculative nature of the “AI Dislocation” framework means timing and magnitude of any rotation toward small-caps remain inherently unpredictable.

The sector divergence observable in today’s market data reveals important structural dynamics. Technology’s resilience (+0.46%) contrasts sharply with Basic Materials (-2.49%), Healthcare (-1.41%), and Communication Services (-1.31%) [0]. This divergence may reflect ongoing rotation within equity markets as investors reassess relative valuations and growth prospects. The Real Estate (+0.25%) and Utilities (+0.06%) sectors’ modest gains suggest some defensive positioning, though the magnitude is limited [0].

The relationship between small-cap performance and economic acceleration deserves particular attention. Historically, small-cap indices have demonstrated higher correlation with domestic economic growth than large-cap indices, which derive substantial revenue from international operations. If the author’s GDP acceleration thesis proves accurate, the Russell 2000’s strong January performance may represent the early stages of a sustained relative strength trend rather than a temporary anomaly.

The analysis reveals several interconnected themes that extend beyond the article’s surface-level bullish stance. First, the acceleration from 3.8% to 4.4% GDP growth in consecutive quarters suggests the U.S. economy possesses greater resilience than many bears have argued, potentially supporting elevated equity valuations that might otherwise appear stretched by traditional metrics [1]. Second, the January small-cap outperformance, if sustained, could signal a structural shift in market leadership that alters the risk-reward profile of growth-oriented portfolios.

Third, the promotional structure of the article—teasing specific recommendations behind paid content—represents a common but underappreciated information asymmetry in retail investment media. Investors should recognize that analyses positioning themselves as “free insights” while directing readers toward paid products may have incentive structures that differ from objective, independent research [1]. Fourth, the AI investment thesis, regardless of its ultimate validity, has demonstrably influenced sector allocation decisions and relative valuations across technology and related sectors, creating both opportunities and risks that transcend the specific question of AI adoption trajectories.

The market volatility illustrated by today’s broad-based declines (-0.57% to -1.11% across indices) represents the most immediate risk factor [0]. Even investors convinced by the structural economic thesis must navigate significant short-term fluctuations that can test conviction and potentially force suboptimal exits. The aggressive 6% GDP forecast introduces forecast risk—a projection that may not materialize due to policy changes, external shocks, or momentum shifts in economic data. Small-cap exposure inherently carries higher volatility and liquidity risk compared to large-cap investments, meaning positions in the Russell 2000 or related indices may experience exaggerated drawdowns during periods of market stress.

The speculative nature of the “AI Dislocation” thesis warrants particular caution. While the narrative of AI adoption broadening from large to small companies is coherent, historical precedent for such rotations is mixed, and timing remains extremely difficult to predict [1]. Investors should maintain realistic expectations about the uncertainty inherent in forward-looking sector rotation strategies.

The small-cap momentum evidenced by the Russell 2000’s 7% January gain presents a potential opportunity for investors positioned to benefit from sustained rotation [1]. Should economic acceleration prove durable and AI adoption genuinely broaden to smaller companies, early positioning could generate meaningful alpha relative to large-cap concentrated strategies. The current sector divergence—with Technology showing relative strength while Materials and cyclicals pull back—may offer tactical entry points for investors with longer time horizons who can tolerate near-term volatility.

The key insight is that opportunity and risk exist simultaneously. The economic data supporting the bullish thesis is substantive, but the market’s response to that data remains uncertain. Investors should calibrate position sizes appropriately and maintain flexibility to adjust allocations as conditions evolve.

The InvestorPlace analysis presents a coherent bullish investment thesis grounded in accelerating economic growth and a potential sector rotation toward smaller companies positioned to benefit from AI adoption. Key data points include Q3 2025 GDP of 4.4% (up from 3.8% in Q2), consumer spending growth of 3.5%, and Russell 2000 outperformance of +7% in January versus +1.4-1.6% for major indices [1]. The author projects U.S. GDP could reach 6% in H2 2026, though this forecast carries significant uncertainty.

Current market data from February 5, 2026 shows all major indices declining (S&P 500 -0.57%, NASDAQ -0.28%, Dow Jones -0.68%, Russell 2000 -1.11%), with Technology (+0.46%) the only positive sector [0]. This short-term volatility illustrates the market noise acknowledged in the article while not necessarily contradicting the underlying structural thesis.

The article functions as teaser content for a separate paid briefing and does not disclose specific stock recommendations [1]. The promotional structure warrants appropriate skepticism from readers. Risk factors include elevated market volatility, forecast uncertainty, small-cap volatility, and the speculative nature of the AI rotation thesis. Investors considering implications should conduct independent verification of economic data and assess how thematic positioning aligns with their risk tolerance and investment horizon.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.