U.S. Retail Sales Analysis: December 2025 Performance and Tariff Impact on Consumer Behavior

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

The December 2025 retail sales data presents a nuanced picture of American consumer behavior amid evolving economic conditions and trade policy shifts. According to the MarketWatch report published on February 10, 2026, U.S. retail sales were essentially unchanged from November, missing economist expectations of a 0.4% increase and signaling a notable deceleration in consumer spending momentum as the year concluded [1]. This flat reading followed a year in which unadjusted retail sales increased 3.8% year-over-year—a figure analysts characterize as “decent but below-trend” growth that reflects both consumer resilience and emerging headwinds [1].

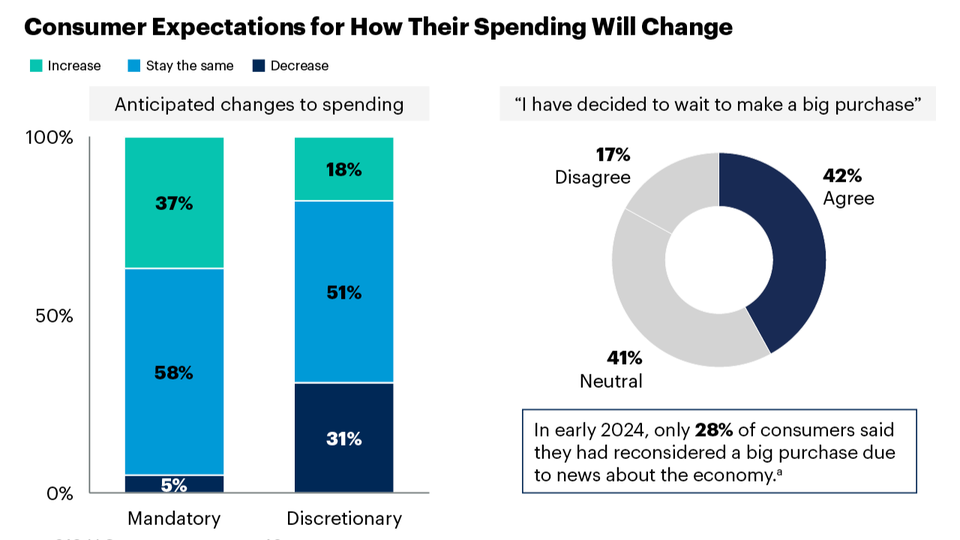

The most significant finding from the retail sales data centers on how tariff policies fundamentally altered American buying habits throughout 2025. Rather than following traditional seasonal patterns, consumers demonstrated a pronounced tendency to accelerate major purchases in spring and summer months, apparently in response to anticipation of tariff-related price increases on imported goods [1]. This front-loading of spending created an artificial surge in early-year retail activity, followed by a corresponding pullback in the second half of the year as consumers exhausted their immediate purchasing needs and exercised increased caution heading into the new year [1]. This tariff-driven consumption pattern suggests underlying economic fragility, as organic growth momentum appears to have been supplanted by policy-driven timing adjustments rather than fundamental strength in consumer demand.

The sector-level performance data reveals a deeply bifurcated retail landscape that favors certain categories while penalizing others. Consumer defensive stocks experienced the worst single-day performance among all sectors, declining 0.76% on February 10, 2026, while consumer cyclical stocks fell 0.27%, underperforming the broader market indices [0]. This sector rotation away from consumer-related investments reflects investor concerns about the sustainability of consumer spending into 2026, particularly given the flat December reading and the evidence of tariff-driven spending distortions throughout the prior year.

Home centers emerged as the clear outperformer within the retail sector, with building materials and garden stores recording small increases while home improvement giants Home Depot and Lowe’s achieved outsized gains [1][2]. This strength in home improvement retail suggests continued housing market activity and indicates that homeowners prioritized renovation and improvement projects—potentially accelerating purchases in anticipation of tariff-driven price increases on building materials and home goods. Conversely, auto dealers, clothing stores, furniture and home furnishings retailers, electronics and appliance stores, pharmacies, and restaurants all experienced declines during the December period, indicating broad-based weakness across discretionary spending categories [1][2].

The XRT (SPDR S&P Retail ETF) technical profile provides additional context for the retail sector’s recent trajectory. Trading at $89.04, the ETF remains above all major moving averages—the 20-day at $88.89, 50-day at $87.65, and 200-day at $82.27—indicating that market participants have largely priced in recent weakness [0]. However, the modest 14.93% gain recorded over the 16-month period since September 2024 reflects compressed valuations across the retail space, suggesting investor caution about the sector’s growth prospects [0]. Daily volatility of 1.49% indicates ongoing uncertainty that traders and investors must navigate carefully.

The tariff-induced spending pattern identified in the retail sales data carries profound implications for understanding how trade policy translates into consumer economic behavior. The fact that American consumers demonstrably altered their purchasing timing in response to anticipated tariff impacts reveals a sophisticated level of economic awareness among households, while simultaneously demonstrating the vulnerability of consumer spending to policy uncertainty. This finding suggests that future tariff developments—whether implementation, modification, or removal—could produce similar distortions in consumption patterns, creating both opportunities and risks for retail sector forecasting.

The concentration of early-year spending gains among higher-income households while middle- and lower-income Americans “did not fare as well” represents a critical structural concern within the consumer economy [1]. Higher-income households possess greater flexibility to accelerate major purchases in response to anticipated price increases, while middle- and lower-income consumers face budget constraints that limit their ability to engage in similar timing strategies. This income-based bifurcation creates concentration risk within consumer spending data, as economic health indicators may overstate overall consumer resilience when they are disproportionately driven by affluent household behavior.

The modest job additions of approximately 28,000 monthly since December contrast sharply with the 400,000 monthly job growth observed during the 2021-2023 post-COVID economic expansion, suggesting a meaningful deceleration in labor market support for consumer spending [2]. While December CPI remained steady at 0.3%, matching November’s rate and indicating relatively controlled inflation, the combination of modest employment growth and flat retail sales raises questions about whether consumer purchasing power can sustain economic expansion into 2026 [1]. The consumer spending component represents what analysts describe as “the main pillar of growth for the U.S. economy,” making any erosion in consumer confidence or purchasing capacity a matter of significant macroeconomic concern.

The retail sector faces several identifiable risk factors that warrant continued monitoring. The tariff-driven spending pattern—characterized by front-loading followed by pullback—suggests underlying economic fragility rather than organic growth momentum, as consumer expenditure patterns respond more to policy uncertainty than to fundamental economic strength [1]. This dynamic creates inherent unpredictability in retail sales forecasting and introduces volatility into sector performance that investors must navigate. Multiple store closures and bankruptcies within the retail sector, including notable names such as Eddie Bauer, Saks Off 5th, and Amazon Go/Fresh operations, indicate structural pressures that extend beyond cyclical concerns to fundamental shifts in consumer shopping behavior and retail business models [2].

The income inequality dimension of consumer spending creates additional risk exposure, as the concentration of spending strength among higher-income households introduces vulnerability to any factor that disproportionately affects affluent consumer confidence or purchasing capacity [1]. Should housing markets weaken, investment portfolios decline, or employment conditions shift among higher-income demographics, the primary driver of retail sales growth could experience significant disruption.

From an opportunity perspective, the home improvement retail segment demonstrates resilience and potential growth catalysts given continued housing market activity and potential tariff-related price dynamics. Retailers that successfully navigate the tariff landscape—either through supply chain diversification, pricing strategies, or product positioning—may capture market share as weaker competitors consolidate or exit. The steady inflation readings provide the Federal Reserve with potential flexibility for rate considerations later in 2026, which could stimulate consumer borrowing and spending if implemented [1].

Key factors warranting ongoing monitoring include January 2026 retail sales data to determine whether tariff-related pullback continues, Federal Reserve policy signals regarding potential rate adjustments, fourth quarter 2025 corporate earnings for retailer guidance on consumer outlook, consumer confidence indices from the University of Michigan and Conference Board, and any tariff policy developments that could shift consumer behavior patterns again [1].

The December 2025 retail sales report, delayed due to the federal shutdown and published on February 10, 2026, documents flat consumer spending that missed expectations and revealed tariff-driven distortions in purchasing patterns [1]. Unadjusted year-over-year growth of 3.8% represents solid but below-trend expansion, while the flat December reading raises questions about sustainable momentum. Consumer defensive and cyclical sectors underperformed broader markets, with home improvement retailers emerging as the primary outperformer amid sector-wide weakness. The Commerce Department’s complete retail sales data warrant verification given the reporting delay, and additional investigation into tariff implementation timelines, regional variations, and detailed income cohort spending patterns would provide enhanced visibility for decision-making purposes.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.