January 2026 Non-Farm Payrolls Report: Delayed Release with Potential $1M+ Benchmark Revisions

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

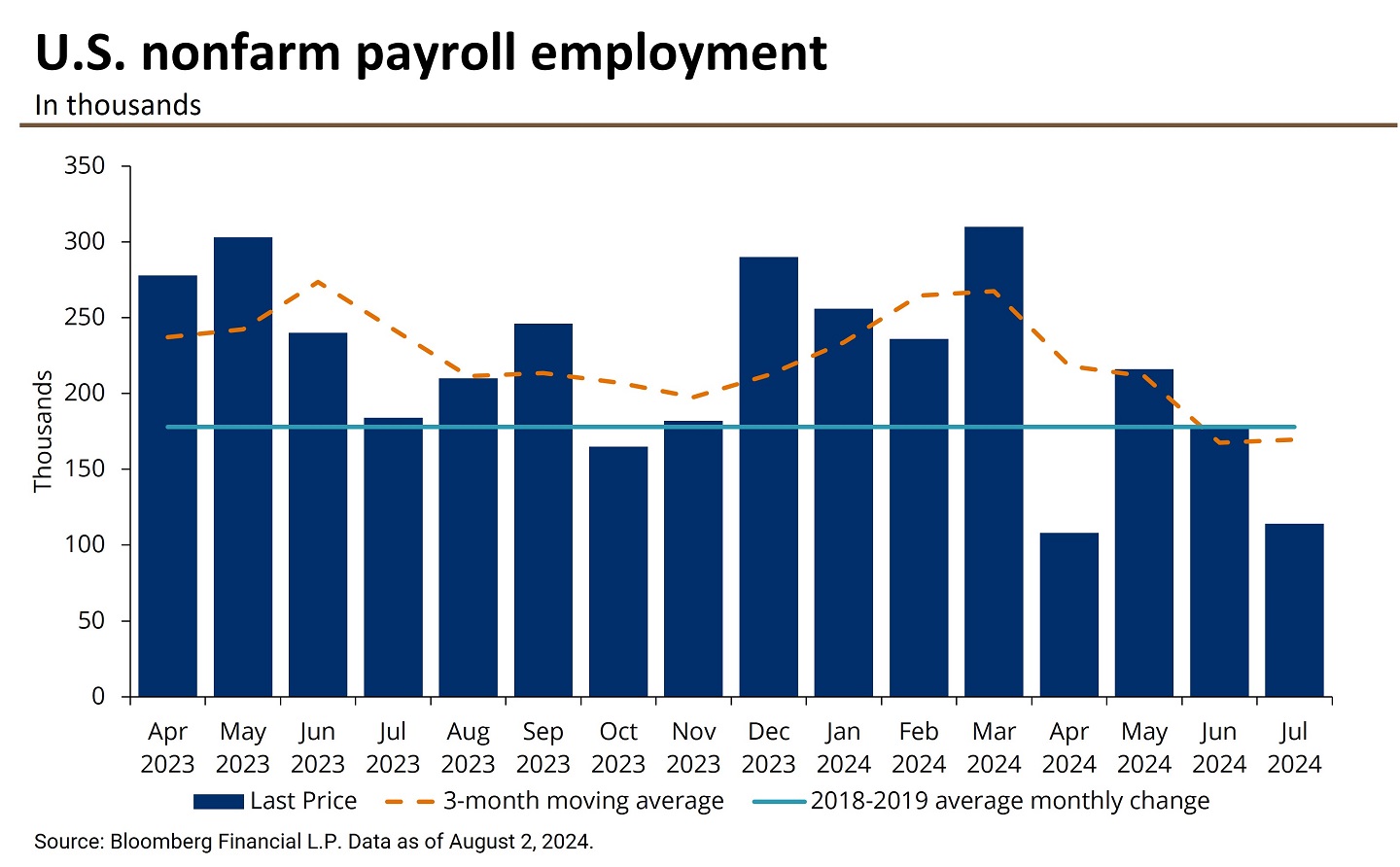

The January 2026 Non-Farm Payrolls report represents a significant data release for financial markets, distinguished by dual characteristics: its delayed publication due to the partial U.S. government shutdown and the anticipated substantial annual benchmark revisions that could fundamentally reshape perceptions of the 2025 labor market [1][3]. Scheduled for release on Wednesday, February 11, 2026 at 13:30 GMT, this employment data carries heightened significance for Federal Reserve policy decisions and market positioning in the coming weeks.

The Bureau of Labor Statistics typically releases NFP data on the first Friday of each month, but the government funding gap necessitated this exceptional postponement. Markets have operated with reduced visibility into labor market conditions during this interval, amplifying the importance of the forthcoming release as a comprehensive assessment of employment trends.

Economists project that the January NFP report will show approximately

The unemployment rate is expected to remain steady at

Average hourly earnings growth is projected at

The most consequential element of this report—and the factor most likely to drive market reaction—pertains to the

Analysts project downward revisions to 2025 employment figures in the range of

This benchmark revision process is technically routine—the BLS has conducted annual recalibrations for decades—but the anticipated magnitude is unusually large and reflects known methodological challenges in measuring rapid labor market changes during periods of significant economic transition. The revision would effectively “reset” market expectations for the 2025 employment trajectory and could prompt substantial reassessment of Federal Reserve policy paths.

The January NFP report arrives at a pivotal juncture for Federal Reserve decision-making, with the March FOMC meeting representing the next policy decision point [1][2]. Markets currently price approximately

A weak headline number combined with substantial downward benchmark revisions would likely accelerate market expectations for monetary easing, potentially pushing March cut probabilities toward 30-40% [1]. Conversely, a robust headline number that substantially exceeds the +70,000 consensus could reinforce the “higher-for-longer” narrative and dampen rate cut expectations.

The dual nature of this report—monthly headline data plus annual benchmark revisions—creates interpretive complexity for Fed officials. The benchmark revisions provide retrospective clarity about 2025 conditions, while the January figure offers prospective insight into 2026 trajectory. Fed communications in recent weeks have emphasized data dependency, making this comprehensive labor market assessment particularly influential for the policy debate.

Pre-release market behavior reflects the anticipation surrounding this data [3]. Dow futures have shown preliminary gains, suggesting investor optimism or defensive positioning against potential downside scenarios. The U.S. dollar has weakened, with the Dollar Index (DXY) testing the

Equity markets exhibited volatility in the February 10 session, with the S&P 500 declining 0.47% to close at 6,941.82, the NASDAQ falling 0.73% to 23,102.47, and the Dow Jones showing relative stability with a 0.01% decrease to 50,188.15 [0]. The Russell 2000’s 0.45% decline and 2.10% weekly gain suggests ongoing rotation dynamics between large-cap stability and small-cap opportunity.

The annual benchmark revision process, while routine, carries exceptional significance this cycle due to its anticipated magnitude. The BLS methodology involves reconciling monthly establishment survey data (CES) with quarterly census of employment and wages (CEW) data derived from state unemployment insurance records [1]. This reconciliation process identified discrepancies that suggest the monthly survey methodology may have overstated 2025 employment growth.

The practical implication extends beyond historical revision: markets will need to recalibrate expectations for the entire 2025 labor market narrative. If employment growth was substantially weaker than reported, consumer spending resilience, business investment decisions, and productivity metrics all require reassessment. This retrospective clarity could validate concerns that have persisted among some analysts throughout 2025 regarding the durability of economic expansion.

The government shutdown created a temporal gap in labor market visibility, during which alternative data sources—weekly unemployment claims, private sector employment indicators, and sector-level metrics—provided incomplete substitutes for comprehensive BLS reporting [3]. The January NFP release represents not merely one month’s data but a catch-up assessment incorporating updated methodologies and the benchmark revisions.

This timing dynamic introduces elevated uncertainty into market pricing. Traders and investors have operated with imperfect information about January labor conditions, and the release may reveal developments that deviate significantly from consensus expectations derived from fragmented indicators. Historically, delayed economic data releases following government disruptions have exhibited higher-than-normal volatility upon publication.

The dollar’s weakness ahead of the release suggests currency markets are positioning for potential labor market disappointment [3]. The 98.00 support level on DXY represents a technically significant zone, and sustained breach could signal broader dollar weakness with implications for international capital flows and multinational corporate earnings.

Fixed income markets will likely exhibit pronounced sensitivity to the release, with Treasury yields adjusting based on updated Fed policy expectations. The 10-year Treasury yield movement following the report will provide insight into market assessments of the neutral rate, inflation expectations, and growth trajectory.

The January 2026 Non-Farm Payrolls report, releasing February 11 at 13:30 GMT following delay due to the partial government shutdown, presents a high-information-density data event combining monthly employment indicators with significant annual benchmark revisions.

The synthesis of monthly data and retrospective benchmark revisions will provide comprehensive labor market clarity that has been obscured during the government shutdown period, enabling more informed positioning for the remainder of the first quarter.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.