META Investment Analysis: Evaluating Buy and Hold Opportunity After Recent Pullback

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Reddit investors show mixed sentiment on META’s current valuation opportunity:

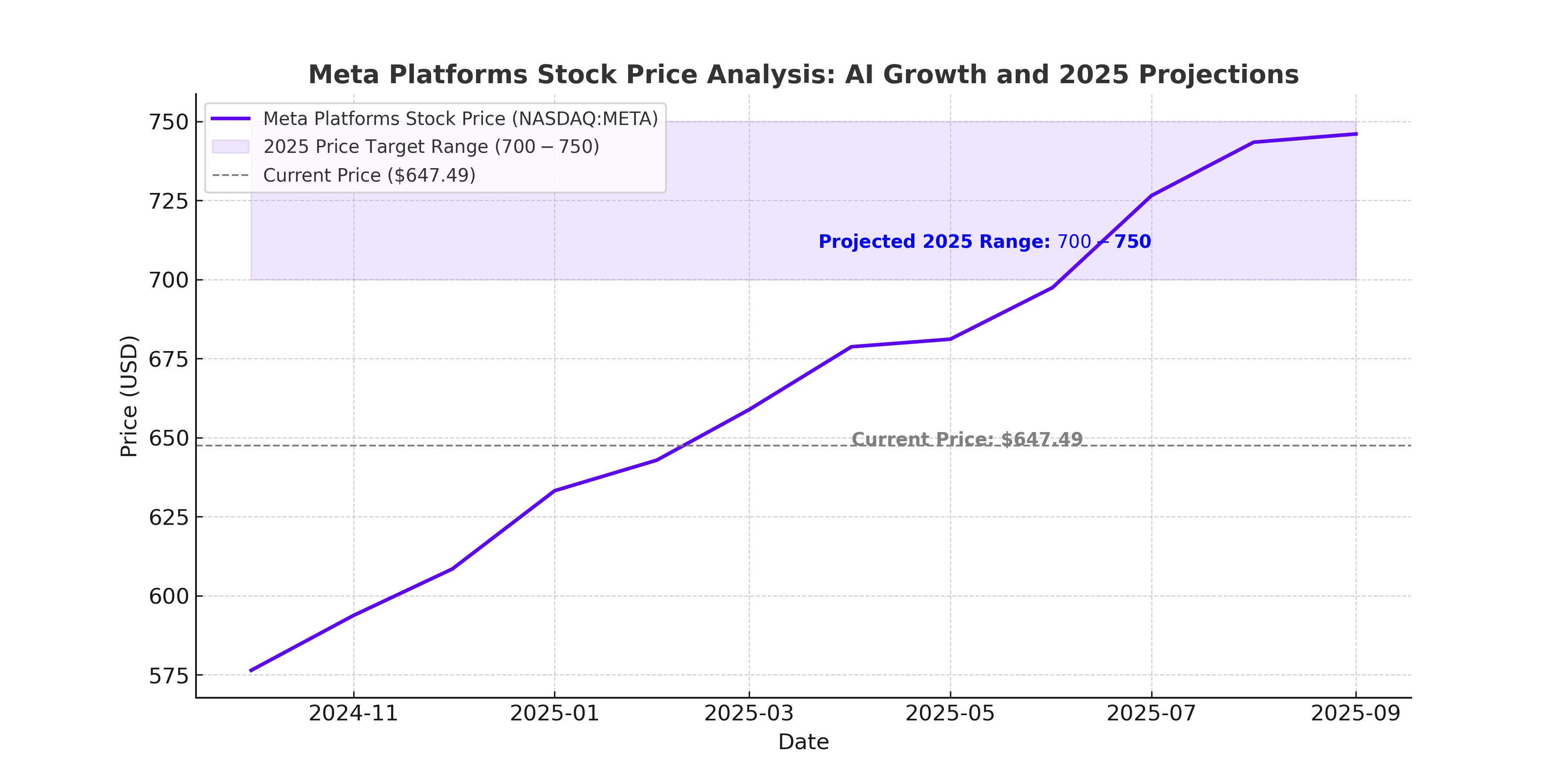

- Average analyst target of ~$840 represents ~30% upside potential from current levels

- Intrinsic value estimates range from $800-$1,000, suggesting the recent dip is a buying opportunity

- Strong financial fundamentals and robust user base of 3.54B daily active users across family apps

- Several users advocate buying the dip and implementing dollar-cost averaging strategies

- Current ~30x P/E ratio may be too high given 7% EPS growth expectations

- Skepticism about AR/VR segment and Zuckerberg’s leadership

- Sustainability questions around reliance on algorithmic content and monetization challenges with WhatsApp

- Some investors waiting for steeper discount before entering positions

Meta’s Q3 2024 performance demonstrates strong operational momentum:

- Revenue grew 26% YoY to $51.24B, exceeding expectations of $49.6B

- Family of Apps revenue reached $50.77B vs $48.6B expected

- Ad impressions increased 14% while average price per ad rose 10%

- EPS of $1.05 missed consensus of $6.72 due to one-time tax-related charge

- Daily active users across family apps grew to over 3.5 billion

- Maintained robust engagement metrics across platforms

- Capital expenditures rose over 100% in Q3 2024

- 2025 capex guidance increased to $70-72 billion

- 2026 capex growth expected to be notably larger than 2025

- AI infrastructure spending may exceed $100 billion by 2026

- Current P/E ratio around 28.7x, in line with industry averages

- Analyst consensus shows predominantly positive sentiment with ‘Strong Buy’ and ‘Moderate Buy’ ratings

- Price targets mentioned range from $800-$930

- Both Reddit discussions and research confirm strong user base (3.5B+ DAUs) as key value driver

- Agreement on robust financial performance and revenue growth trajectory

- Recognition of massive AI investment as both opportunity and risk factor

- Reddit’s $550-$750 valuation range doesn’t align with research findings showing analyst targets of $800-$930

- Reddit concerns about 7% EPS growth may be outdated given Q3’s 26% revenue acceleration

- Research shows P/E of 28.7x vs Reddit’s 30x estimate - both reasonable given growth profile

The recent pullback appears to offer a reasonable entry point, particularly for long-term investors comfortable with Meta’s aggressive AI investment strategy. The company’s strong revenue acceleration and massive user base provide solid fundamentals, while AI infrastructure investments position Meta for future growth despite near-term margin pressure.

- Massive capital expenditures ($100B+ by 2026) could pressure margins and returns

- AR/VR segment remains unproven and capital-intensive

- Regulatory scrutiny and platform competition risks

- Execution risk on AI strategy and monetization

- AI infrastructure investments could create competitive moat and new revenue streams

- Strong advertising platform benefiting from AI improvements

- Cross-platform synergies across 3.5B+ user ecosystem

- Potential for multiple expansion if AI investments deliver expected returns

Consider dollar-cost averaging into META positions, particularly on further weakness. The current valuation appears reasonable given growth prospects, but investors should be prepared for volatility as the market digests massive AI spending and its impact on future profitability.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.