Risk Assets: Navigating Crosscurrents - Sector Rotation Dynamics in February 2026

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

The current market environment represents a nuanced phase in the 2026 equity cycle, where constructive macro fundamentals coexist with significant tactical shifts in sector positioning. The S&P 500’s position near 6,881 reflects this dual nature—moderate gains driven by technology shares despite Fed policy uncertainty and elevated valuations [0][1].

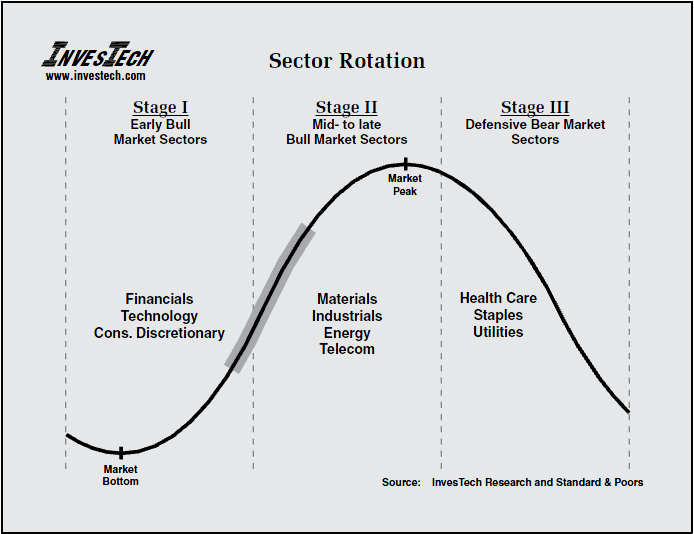

The most significant market development is the pronounced sector rotation phenomenon, which the Seeking Alpha analysis identifies as the primary expression of crosscurrents rather than outright risk-off moves [1]. This rotation has been characterized by Morningstar analysts as a “panic rotation,” marked by the unusual tandem movement of defensive and cyclical stocks—a rare occurrence that signals underlying structural changes in market leadership [2].

The Federal Reserve’s decision to maintain its target range at 3.5%-3.75% following the January 2026 FOMC meeting revealed significant division among policymakers [4]. Some officials suggested pausing rate cuts for now, while others indicated cuts could resume later in 2026 if inflation declines. This policy uncertainty has contributed to the sector rotation dynamics, as investors reposition between growth and value exposures based on anticipated monetary policy paths.

Nvidia continues to be a major market driver, with Meta Platforms announcing plans to use millions of Nvidia chips in its data-center buildout, supporting Nvidia shares (+1.6%) [1]. However, the AI infrastructure boom has generated both enthusiasm and skepticism. As analyst Stephen Hoedt noted: “Nvidia is dealing with the cross section of high expectations priced into the stock, but also a skeptical market” [5]. This tension between high expectations and growing skepticism is manifesting as pressure on the broader “Magnificent Seven” group, which has underperformed significantly during this rotation.

The simultaneous strength in both defensive sectors (consumer staples +7% in February, 16% YTD; utilities performing strongly) and cyclical groups (industrials +7% in February, 14% YTD; materials +7% in February, 17.6% YTD) represents a significant market anomaly [2]. Historically, these sectors move in opposite directions based on economic outlook, but current conditions have created a “buy everything” dynamic that reflects uncertainty rather than conviction. This suggests investors are hedging multiple scenarios rather than committing to a single directional thesis.

The rotation into industrials and materials is being driven by a specific catalyst: “physical AI” demand related to data center construction and infrastructure buildout [2]. This theme has legs according to analysts, as the AI infrastructure boom requires substantial physical inputs—construction materials, industrial equipment, and infrastructure components—that are distinct from the software and semiconductor focus that drove previous market phases.

The overcooked defensive positioning creates risk of a rapid unwind if economic data improves or sentiment shifts [2]. Consumer staples and utilities have benefited from safety-seeking behavior, but if the macro backdrop proves more resilient than anticipated, these positions could face significant pressure as investors reallocate to higher-growth opportunities.

High expectations priced into technology stocks create vulnerability to earnings disappointments. The “Magnificent Seven” group has underperformed sharply during this rotation, reflecting market reassessment of growth trajectories rather than fundamental deterioration in these businesses. The February 26 earnings date represents a critical test for this dynamic.

-

Tech Earnings Disappointment:With valuations elevated, AI-related earnings face intense scrutiny. Any miss could trigger further rotation out of growth names, potentially exacerbating market volatility [0].

-

Defensive Unwind:The crowded defensive positioning creates risk of rapid correction if economic data improves or Fed policy becomes clearer, leading to swift reallocation away from staples and utilities [2].

-

Fed Policy Uncertainty:The division among policymakers suggests the path forward remains unclear. Any hawkish surprise could pressure both growth and defensive positions [4].

-

Geopolitical Risks:U.S.-Iran tensions have been noted as potential risk-off catalysts that could disrupt the current rotation dynamics [4].

-

Volatility Persistence:The S&P 500 was on pace for its worst month since April 2025, with volatility expected to continue into late February [3].

-

Physical AI Infrastructure:Industrials and materials continue benefiting from AI infrastructure buildout—this theme has demonstrated sustained momentum and appears to have further runway [2].

-

Rotation Reversal Potential:If the defensive trade becomes overcooked, a reversal could present opportunities in quality growth names at reduced valuations.

-

Sector Dispersion:The current environment creates tactical opportunities as correlations break down, allowing for more granular sector and security selection.

The February 2026 market environment reflects a constructive macro backdrop navigating significant crosscurrents. Market data indicates the S&P 500 closed at approximately 6,881, with the Nasdaq Composite around 22,754 and Dow Jones Industrial near 49,663 [0][1]. The index fell approximately 0.9% for the month, representing its worst performance since April 2025 [3].

Sector rotation remains the dominant theme, with consumer staples (+7%), industrials (+7%), and materials (+7%) leading February performance while technology—particularly the “Magnificent Seven”—experienced sharp pressure [2]. The Federal Reserve maintained rates at 3.5%-3.75% with divided guidance on the path forward [4]. Notable individual movers included Nvidia (+1.6% on Meta’s AI announcement), Amazon (+~2% following Bill Ackman’s stake increase), Micron Technology (+5% on David Tepper’s increased holdings), and Trade Desk (-16% on missed projections) [1][2].

Key technical levels to watch include S&P 500 support around 6,800 and resistance near 6,950, with the Nasdaq watching 22,500 as a technical pivot [0]. The February 26 earnings date represents a significant catalyst with potential for notable market movement. Inflation readings will remain critical for Fed policy trajectory, while the current elevated volatility expectations suggest continued intraday swings in the near term.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.