Shipping Stocks Rally as Baltic Dry Index Surges 60% From 2023 Lows

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

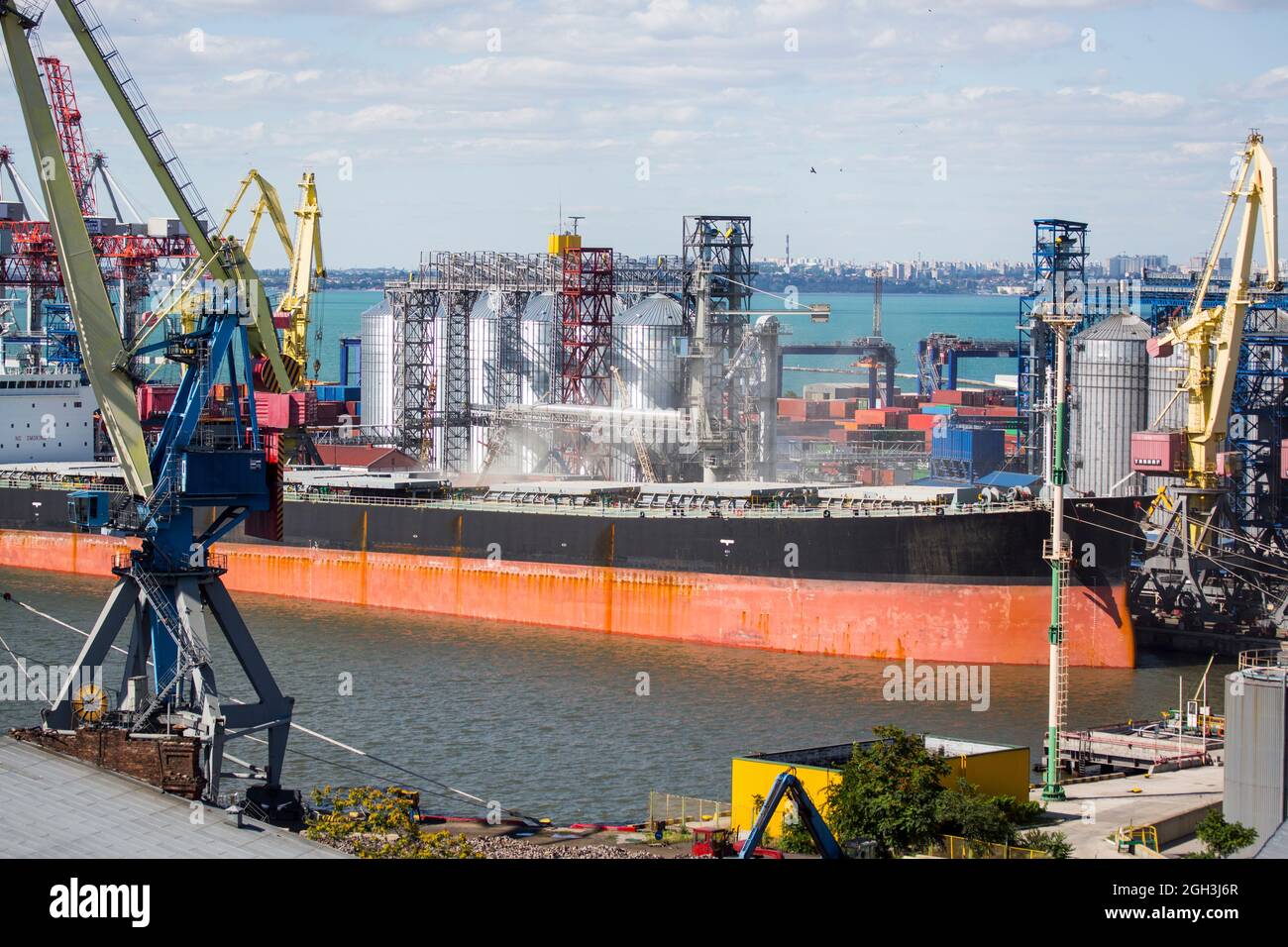

The shipping industry’s resurgence in early 2026 represents a fundamental recovery driven by structural supply-demand rebalancing rather than speculative positioning. The Baltic Dry Index (BDI), a key benchmark measuring the cost of shipping dry bulk commodities such as iron ore, coal, and grain, has risen more than 60% from its 2023 lows, currently trading at approximately 2,100 points [1][2][3]. This significant recovery signals a substantial improvement in global shipping demand after years of depression during which the index languished near multi-year lows amid weak global trade and excess vessel capacity.

The supply-side dynamics provide a particularly constructive backdrop for sustained freight rate elevation. According to Clarksons Research data, the dry-bulk vessel orderbook stands at approximately 7% of the current fleet—near multi-decade lows [1]. This constrained supply environment contrasts sharply with the period after 2020-2021 when excessive newbuilding orders created chronic overcapacity. Several structural factors are limiting fleet expansion: elevated shipbuilding costs continue to deter new orders, stricter environmental regulations under IMO 2030 carbon intensity targets are accelerating vessel retirement while constraining newbuildings, and limited shipyard capacity is extending delivery timelines. Clarksons projects global fleet growth will remain below 3% annually through 2027, significantly below historical averages [1].

On the demand side, multiple factors are supporting shipping activity. Global demand for key dry bulk commodities remains robust, while the World Trade Organization projects merchandise trade growth recovery in 2026 after the previous slowdown [1]. Additionally, longer average sailing distances are expected to support dry bulk demand through 2026, helping to offset any rising fleet growth [4].

The shipping industry is experiencing a significant revival in early 2026, with the Baltic Dry Index rising more than 60% from its 2023 lows to approximately 2,100 points [1][2][3]. This recovery is fundamentally driven by a notable supply-side rebalancing—the dry bulk vessel orderbook stands at approximately 7% of the current fleet, near multi-decade lows, with Clarksons projecting global fleet growth below 3% annually through 2027 [1]. The Breakwave Dry Bulk Shipping ETF (BDRY) has posted a 35% year-to-date gain, significantly outperforming the broader market [1]. Individual shipping stocks have shown strong performance: Star Bulk Carriers (SBLK) has gained 22.87% year-to-date, while Danaos Corporation (DAC) has risen 13.44% [1]. On the demand side, the WTO projects merchandise trade growth recovery in 2026, supporting shipping activity [1]. All shipping segments are outperforming the S&P 500 in 2026, with crude tankers up 26% and liner stocks up 7% [5].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.