Energy Price Scenarios and Market Implications: Geopolitical Risk and Monetary Policy Divergence Analysis

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis examines the market implications of new energy price scenarios presented by Seeking Alpha, set against the backdrop of the US-Israel conflict with Iran that began in late February 2026. The analysis integrates findings from the original Seeking Alpha baseline scenario—which assumes Federal Reserve rate cuts and no ECB rate hikes, with EUR/USD expected to return to 1.20—alongside the significant geopolitical disruptions driving energy price volatility. Global oil prices have surged approximately 70% from pre-conflict levels, with Brent crude trading around $106 per barrel as of mid-March 2026 [1][3]. This energy shock has dramatically shifted monetary policy expectations, with market participants now pricing in a approximately 70% probability of two 25-basis-point ECB rate hikes by year-end, while Fed Funds Futures indicate a 43% chance of three or more rate cuts in 2026 [2][5]. The Energy sector demonstrated modest gains of 0.29% on March 17, 2026, suggesting markets may have already priced much of the current geopolitical risk premium [0].

The Seeking Alpha baseline scenario establishes a framework of monetary policy divergence between the United States and Europe. The analysis continues to assume rate cuts by the Federal Reserve while anticipating no interest rate hikes from the European Central Bank, projecting that both USD and EUR rates could decline by year-end as the growth outlook deteriorates [1]. This baseline expectation of EUR/USD returning to 1.20 during 2026 reflects assumptions of continued dollar weakness and European economic resilience.

However, the energy price shock emanating from the Iran conflict has introduced substantial uncertainty into these baseline projections. The geopolitical disruption represents a significant deviation from the smooth scenario contemplated in the original analysis, forcing rapid recalibration of market expectations across multiple asset classes.

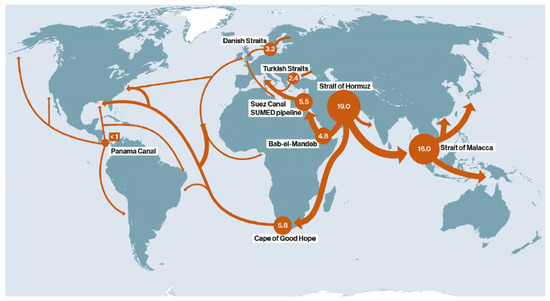

The US-Israel conflict with Iran, which began in late February 2026, has fundamentally reshaped the energy price landscape and created cascading effects across financial markets. Global oil prices have surged approximately 70% from pre-conflict levels, with Brent crude currently trading around $106 per barrel as of mid-March 2026 [3]. This represents an extraordinary price movement within a matter of weeks and introduces significant supply disruption risks, particularly regarding the Strait of Hormuz—a critical chokepoint through which approximately 20% of global oil supplies transit.

Bank of America commodity strategist Francisco Blanch has outlined scenarios where Brent prices could surge above $100 per barrel, with European natural gas prices potentially breaking 60 euros per megawatt hour if Iranian facilities are targeted [3]. Goldman Sachs has revised its oil price forecasts upward, now projecting Q4 2026 Brent prices at $71 per barrel and WTI at $67 per barrel, representing increases from previous estimates of $66 and $62 respectively [4].

The most severe scenario, analyzed by JPMorgan, suggests that if the Strait of Hormuz were disrupted for several months, Brent prices could spike by $40-80 per barrel, potentially reaching $120 per barrel [3]. This tail risk remains a significant concern for market participants and central bankers alike.

The energy price spike has dramatically altered the monetary policy outlook on both sides of the Atlantic, creating a stark divergence from baseline expectations. Interest rate futures now price in approximately a 70% probability of two 25-basis-point ECB rate hikes by year-end, with a first hike fully priced by July 2026 [2]. This represents a substantial recalibration of market expectations within just a few weeks—from anticipating continued ECB rate cuts at the start of the year to now expecting tightening.

The contrast with Federal Reserve expectations could not be starker. Fed Funds Futures markets now see a 43% chance of three or more rate cuts in 2026, up sharply from 25.6% just one month ago [5]. Fed officials including Chicago President Austan Goolsbee have indicated openness to further rate reductions if progress toward the 2% inflation target continues [5]. This creates a significant monetary policy divergence that carries profound implications for currency markets and capital flows.

The monetary policy divergence has created substantial movement in currency markets. The euro has weakened approximately 3% against the dollar since the conflict onset, while remaining relatively firm against other major currencies as the dollar weakens more broadly [2][6]. The EUR/USD pair remains tightly contested around the 1.20 level, with analysts noting that geopolitical concerns could work in favor of the US dollar unless the euro can break decisively through this technical resistance [1].

The 2-year German Schatz yield has risen approximately 40 basis points, signaling market anticipation of tighter European monetary policy [6]. This yield curve movement represents a substantial shift from expectations just weeks earlier and reflects the changing risk calculus for European fixed income investors.

Current sector performance data reveals nuanced market positioning as participants calibrate their response to the evolving situation. On March 17, 2026, the Energy sector demonstrated modest positive performance, gaining 0.29% amid broader market movements [0]. This relatively muted response suggests market participants may have already priced much of the current geopolitical risk premium, though further upside from energy price movements could materialize if supply disruptions occur.

Consumer Cyclical (+0.75%) and Real Estate (+0.74%) sectors led gains, while Consumer Defensive (-1.01%) and Utilities (-0.33%)—traditionally defensive plays—underperformed [0]. This pattern suggests markets are pricing in a moderate growth scenario while remaining cautious about inflation-sensitive sectors. The underperformance of defensive sectors despite elevated geopolitical risk may indicate that investors are prioritizing economic growth concerns over traditional safe-haven positioning.

The Energy sector’s modest 0.29% gain despite significant oil price increases represents a notable market anomaly that warrants careful interpretation. Historically, sharp oil price movements have translated into more pronounced sector performance, suggesting that current pricing may already embed substantial geopolitical risk premium. This implies limited further upside from pure price movements unless actual supply disruptions materialize rather than merely being anticipated.

The European Central Bank faces a particularly challenging trade-off. Energy-driven inflation pressures conflict directly with weakening economic growth prospects, with the eurozone projected at 1.2% growth in 2026 [6]. The ECB must decide whether to prioritize inflation containment through rate hikes or support growth through accommodative policy—a dilemma that has been dramatically underscored by the rapid shift in market expectations from rate cuts to rate hikes within weeks.

The US dollar’s strength against the euro despite growing expectations for Federal Reserve rate cuts reflects the safe-haven dynamics triggered by geopolitical uncertainty. This counterintuitive movement—dollar strengthening amid easing expectations—underscores the complexity of current market dynamics and suggests that geopolitical factors may be dominating traditional interest rate differentials in driving currency movements.

The approximately 3% weakening of the euro against the dollar adds imported inflation pressure to the eurozone economy [6]. This secondary effect complicates ECB policy calculations and may necessitate tighter monetary conditions despite softening growth. The transmission of energy prices through to broader inflation represents a significant concern for policymakers navigating the current environment.

The analysis integrates the Seeking Alpha baseline scenario of Federal Reserve rate cuts and stable ECB policy with the dramatic reality of energy price shocks emanating from the Iran conflict. Global oil prices have surged approximately 70%, with Brent crude at $106 per barrel, fundamentally altering the macroeconomic and monetary policy outlook [1][3].

Market expectations have shifted dramatically, with a 70% probability now priced for two ECB rate hikes this year versus expectations of continued rate cuts at the year’s start [2]. In contrast, Fed Funds Futures indicate a 43% chance of three or more rate cuts in 2026, creating pronounced monetary policy divergence [5]. This divergence has weakened the euro approximately 3% against the dollar and driven the 2-year German Schatz yield up approximately 40 basis points [2][6].

Sector performance reveals nuanced market positioning, with Energy (+0.29%), Consumer Cyclical (+0.75%), and Real Estate (+0.74%) outperforming, while Consumer Defensive (-1.01%) and Utilities (-0.33%) underperform [0]. This pattern suggests markets have priced substantial geopolitical risk premium while maintaining growth-oriented positioning.

The baseline EUR/USD target of 1.20 remains viable but faces headwinds from divergent monetary policies and geopolitical uncertainty [1][7]. The critical variables determining market trajectory include: geopolitical developments affecting energy supply, the pace of monetary policy divergence, inflation trajectory through mid-2026, and European growth dynamics.

For stakeholders across the energy value chain, the current environment favors companies with strong balance sheets capable of weathering extended uncertainty. Financial market participants should position for continued volatility while remaining adaptable to rapid scenario changes. Central banks face challenging trade-offs between supporting growth and containing inflation, with the ECB’s dilemma particularly acute given energy-driven inflation pressures conflicting with weakening growth [6].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.