Institutional Investors Rotate Away from US Equities Toward Emerging Markets and Japan

Executive Summary

This analysis examines the significant shift in institutional investor sentiment documented in the Barron’s report published March 17, 2026, which reveals that the market’s largest investors are reducing allocations to US equities while increasing exposure to emerging markets (at the highest level in five years) and Japanese equities [1]. The underlying data comes from the Commonfund annual survey of over 200 institutional investors representing more than $238 billion in assets [2]. While 49% of institutional investors expect below-average US equity returns in 2026, the key point of optimism remains: 76% express confidence in meeting long-term target returns over the next decade through diversified portfolio construction, including allocations to private markets, emerging markets, and international equities.

Integrated Analysis

Market Context and Event Timing

The institutional investor sentiment shift occurs against a backdrop of elevated market volatility and geopolitical uncertainty. The S&P 500 experienced a 1.01% decline on March 12, 2026, followed by a modest 0.37% recovery on March 16, with the index trading around 6,728 as of March 17 [0]. This pattern reflects the conflicting pressures facing institutional investors: near-term caution driven by valuation concerns and geopolitical risks, balanced against long-term return objectives that require maintaining equity exposure through diversification.

The sector rotation pattern observed in recent trading sessions provides additional context for this institutional reallocation. Energy stocks led market gains with a 1.30% increase on March 17, reflecting geopolitical risk premiums associated with ongoing international tensions, while Technology stocks remained relatively flat at +0.09% [0]. This divergence suggests investors are positioning defensively within US equities while shifting overall allocation toward international markets.

The Commonfund Survey: Quantitative Foundation

The Commonfund survey, released March 12, 2026, provides the empirical foundation for understanding institutional positioning [2]. The survey reveals several critical data points that explain the Barron’s characterization of investors as “pulling back” while remaining “optimistic”:

Return Expectations

: Nearly half (49%) of institutional investors expect lower S&P 500 returns in 2026 compared to the 10-year average of 13% [2]. This represents a significant bearish shift in near-term expectations for US equities.

Economic Sentiment

: While 42% maintain a neutral economic outlook, 35% express bullish sentiment (up substantially from 22% last year), counterbalanced by 17% holding bearish views [2]. This mixed but gradually improving economic outlook contrasts with elevated equity market caution.

Geopolitical Concerns

: The dominant worry among institutional investors centers on geopolitical events, with 52% citing this as their primary concern [2][3]. The timing of this survey coincides with early weeks of the Iran conflict, which market analysts suggest may be amplifying these geopolitical risk perceptions.

Asset Allocation Strategy: The Rotation Thesis

The Barron’s article highlights that institutional investors are implementing a clear rotation strategy rather than exiting equities entirely. The key allocation shifts include:

Emerging Markets

: Allocations to emerging markets have reached the highest level in five years, representing a significant strategic repositioning [1]. This reflects both valuation considerations and growth opportunity assessment.

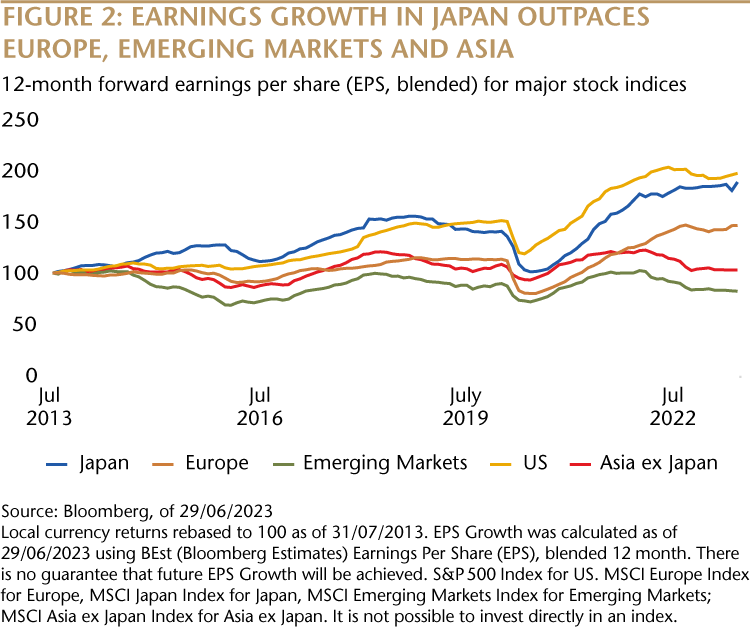

Japanese Equities

: Increased allocations to Japan represent another dimension of the international diversification strategy, benefiting from corporate governance reforms and valuation gaps relative to US markets.

Private Markets

: Notably, 34% of institutional investors expect private equity to deliver the best returns over the next 12 months, while 31% anticipate stronger returns from private markets over a 12-18 month horizon [2]. This preference for private markets introduces liquidity considerations into the allocation framework.

Key Insights

The “Key Point of Optimism” Explained

The Barron’s headline references optimism on “1 key point” – this appears to be institutional confidence in meeting long-term investment targets despite near-term caution [1]. The data reveals that 59% of institutional investors are “modestly bullish” and 17% are “very bullish” about achieving their 10-year target returns [2]. This 76% combined bullish reading on long-term outcomes suggests the current repositioning represents tactical asset allocation adjustment rather than strategic departure from equities.

The optimism is grounded in portfolio diversification capabilities. By allocating to emerging markets, Japanese equities, and private markets, institutional investors believe they can generate sufficient returns to meet long-term targets even if US equities underperform relative to historical averages.

Distinguishing Tactical vs. Strategic Positioning

The institutional behavior documented in this survey represents a nuanced positioning that deserves careful interpretation:

Tactical Adjustments

: The reduction in US equity exposure reflects tactical concerns about valuation (49% expecting lower returns), geopolitical risks (52% top concern), and near-term market conditions. These factors warrant reduced exposure but do not indicate fundamental loss of confidence.

Strategic Commitment

: The maintained long-term optimism (76% bullish on 10-year targets) indicates strategic commitment to equity markets. Investors are rotating within equities rather than toward safety assets like bonds or cash.

Diversification as Risk Management

: The shift toward emerging markets and Japan reflects a sophisticated risk management approach – diversifying geographic exposure to mitigate concentration risk in US markets while maintaining equity exposure for growth requirements.

Risks & Opportunities

Risk Factors to Monitor

Geopolitical Escalation Risk

: With 52% of institutional investors citing geopolitical events as their primary concern, any significant escalation in existing conflicts could trigger rapid risk asset devaluation [2][3]. The Iran conflict’s evolution remains a critical monitor variable.

Emerging Markets Volatility

: While allocations to emerging markets are at five-year highs, these markets carry elevated volatility and liquidity risks. The “largest allocation in five years” could indicate elevated exposure to market corrections in these regions [1].

US Equity Valuation Correction

: The sentiment that 49% expect below-average US returns historically correlates with periods of US equity underperformance. This positioning could become self-fulfilling if institutional selling pressure persists.

Private Market Liquidity

: Heavy reliance on private equity (34% expect best returns) creates potential liquidity constraints during market stress periods. Valuation delays in private markets may amplify exit difficulties.

Stagflation Concerns

: The Seeking Alpha analysis suggests the prolonged Iran conflict raises stagflation risks, which could impact both developed and emerging market returns [3].

Opportunity Windows

International Diversification Benefits

: The rotation toward emerging markets and Japan provides exposure to valuation gaps and growth opportunities unavailable in richly-valued US markets. Investors maintaining US-only exposure may miss these opportunities.

Long-Term Entry Points

: The institutional “pullback” from US equities could create attractive entry points for patient investors who share the long-term optimism (76% bullish on 10-year targets).

Active Management Advantage

: The current environment favors active management capable of navigating sector rotation and geographic allocation shifts – passive index exposure may underperform the institutional repositioning strategy.

Key Information Summary

This analysis synthesizes findings from the Barron’s March 17, 2026 report and the Commonfund survey representing $238 billion in institutional assets [1][2]. The key findings are:

Institutional Positioning

: Major investors are reducing US equity allocations while increasing emerging markets (five-year high) and Japanese equity allocations. This represents rotation within equities rather than flight to safety.

Sentiment Split

: Near-term caution is evident (49% expect below-average US returns), but long-term optimism remains strong (76% bullish on 10-year targets). The “key point of optimism” is confidence in meeting long-term targets through diversified portfolio construction.

Primary Concern

: Geopolitical events (52%) represent the dominant worry, with the Iran conflict timeline potentially amplifying risk perceptions [2][3].

Market Reaction

: Recent US equity weakness (S&P 500 down 1.01% on March 12) aligns with institutional repositioning, though markets have shown resilience with modest recovery subsequent to the initial decline [0].

Sector Rotation

: Energy leading (+1.30%) on geopolitical concerns while Technology remains flat (+0.09%) reflects defensive positioning within US equities [0].

This informational synthesis supports understanding of institutional investment strategy shifts without providing prescriptive recommendations about specific securities or allocation decisions.