Global Markets Navigate Energy Crisis and Interest Rate Repricing Amid Iran Conflict

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

The Iran conflict has evolved into a significant geopolitical and economic crisis with far-reaching implications for global markets. The escalating hostilities involving the US, Israel, and Iran have disrupted critical energy infrastructure, creating substantial uncertainty in energy supply chains worldwide [1][2]. This analysis synthesizes the multidimensional impacts of the conflict on energy markets, monetary policy, and broader economic conditions.

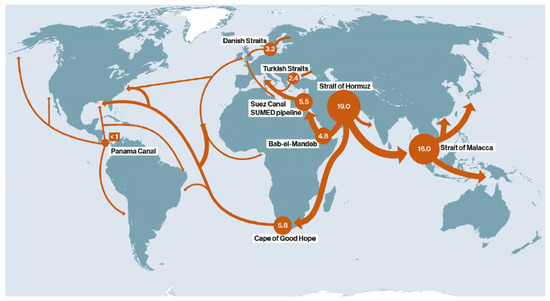

The energy impact has been substantial and potentially long-lasting. Oil prices have surged approximately 40% above pre-conflict levels, with Brent crude trading above $108/barrel. Analysts now consider $200/barrel no longer outside the realm of possibility [3]. The strike on Qatar’s Ras Laffan gas facility has eliminated approximately 17% of Qatar’s LNG export capacity for an estimated 3-5 year period [1], representing a fundamental shift in global natural gas supply dynamics. The Strait of Hormuz, which normally conveys roughly 20% of global oil and LNG supply, remains a focal point of concern [2].

The conflict’s timing coincides with an unprecedented coordination among major central banks. The Federal Reserve, European Central Bank, Bank of England, and Bank of Japan are holding simultaneous meetings this week—the first such occurrence since December 2026 [6]. This gathering reflects the gravity of the situation and the need for coordinated policy responses to emerging economic challenges.

Market volatility has been pronounced. March 18 saw significant selloffs across major indices, with the S&P 500 declining 1.08%, the Nasdaq falling 1.20%, the Dow Jones Industrial Average dropping 1.47%, and the Russell 2000 sliding 1.30% [0]. Some recovery materialized on March 19, but underlying uncertainty persists. Global bond markets have tumbled as investors price in potential rate hikes to combat inflation pressures stemming from elevated energy prices [9].

The macroeconomic implications are significant. The conflict is pushing the US economy toward stagflation—a challenging environment characterized by simultaneous inflation surge and economic growth weakening [8]. US gasoline prices have risen nearly 80 cents per gallon from one month ago, with some markets experiencing prices exceeding $5/gallon [4][5]. These developments complicate the Federal Reserve’s policy calculus significantly.

The current crisis exhibits several distinctive characteristics that differentiate it from previous energy shocks. First, the infrastructure damage to Qatar’s LNG facilities represents a medium-term supply constraint rather than a temporary disruption [1]. The 3-5 year recovery timeline for Ras Laffan means that even conflict resolution would not immediately restore normal supply conditions, fundamentally altering the energy market outlook.

Second, the simultaneous meeting of G4 central banks signals recognition that this crisis requires coordinated international response [6]. The Federal Reserve is expected to maintain rates at the current 3.50-3.75% range with 99% probability in the immediate term [7], but the underlying inflation pressure from energy prices suggests a potential 25-50 basis point rate increase if oil prices remain elevated [8].

Third, market participants are recalibrating expectations regarding the duration and severity of the conflict. Initial assumptions that hostilities and Strait of Hormuz disruptions would be short-lived have given way to recognition that these conditions may persist longer than originally anticipated. This repricing is evident across both equity and fixed income markets.

The strategic response from the US includes formation of a coalition to protect tankers transiting the Strait of Hormuz, while simultaneously allowing Iranian oil tankers to transit—reflecting the complex balancing act required in managing energy supply while avoiding further escalation.

The analysis reveals several elevated risk factors that warrant careful monitoring:

-

Inflation Persistence: The energy shock is compounding existing inflation pressures, creating a difficult dilemma for central banks. The Fed faces a choice between raising rates to control inflation or maintaining accommodation to support economic growth [8].

-

Stagflation Dynamics: The US economy is exhibiting classic stagflation characteristics—simultaneous inflation acceleration and growth deceleration. This combination historically presents challenging policy environments and negative equity market conditions.

-

Prolonged Energy Disruption: Analysts note that the energy crisis will persist even if the conflict ends immediately due to infrastructure damage [2]. The destruction of Qatar’s LNG capacity cannot be rapidly restored, ensuring sustained pressure on natural gas markets.

-

Interest Rate Uncertainty: Market repricing of rate expectations continues, with potential for 25-50 basis point increases if energy prices remain elevated. This creates uncertainty across asset classes.

-

Bond Market Stress: Global bonds are experiencing significant pressure as investors digest the implications of potential rate hikes [9]. This could create spillover effects into equity valuations.

-

Energy Sector Exposure: Companies with production or infrastructure in regions unaffected by the conflict may benefit from elevated commodity prices.

-

Inflation-Protected Securities: Treasury Inflation-Protected Securities (TIPS) and similar instruments may find demand as investors seek inflation hedges.

-

Defense and Security Companies: Companies involved in protection, logistics, and security services for energy transportation may see increased demand.

-

Alternative Energy Development: The crisis highlights vulnerabilities in fossil fuel supply chains, potentially accelerating investment in renewable energy infrastructure and energy independence initiatives.

This analysis synthesizes confirmed developments from multiple authoritative sources regarding the Iran conflict’s market implications:

This information is provided for situational awareness and decision-support purposes. The evolving nature of the conflict and its market implications requires ongoing monitoring.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.