Deepening Energy Crisis Drives Fourth Straight Weekly Stock Losses

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis synthesizes market data, technical indicators, and fundamental developments surrounding the escalating Middle East conflict and its cascading effects on global markets. The original event source from the Wall Street Journal [1] reported that investors’ hopes for a quick resolution to the Iran war are fading, with U.S. stocks and bonds sliding on Friday after the Pentagon sent three more warships and a new deployment of marines to the region.

The market downturn represents the longest weekly losing streak in a year, with all major indices recording significant declines. According to internal market data [0], the S&P 500 declined approximately 1.34% on Friday alone, while the Dow Jones fell 0.87%, Nasdaq dropped 1.55%, and the small-cap Russell 2000 experienced an even sharper 2.24% decline. Since the Iran war began on February 28, 2026, the cumulative damage to equity portfolios is substantial: the Dow has declined 6%, the S&P 500 has fallen 4.5-5%, and the Nasdaq has dropped 4% [0][2].

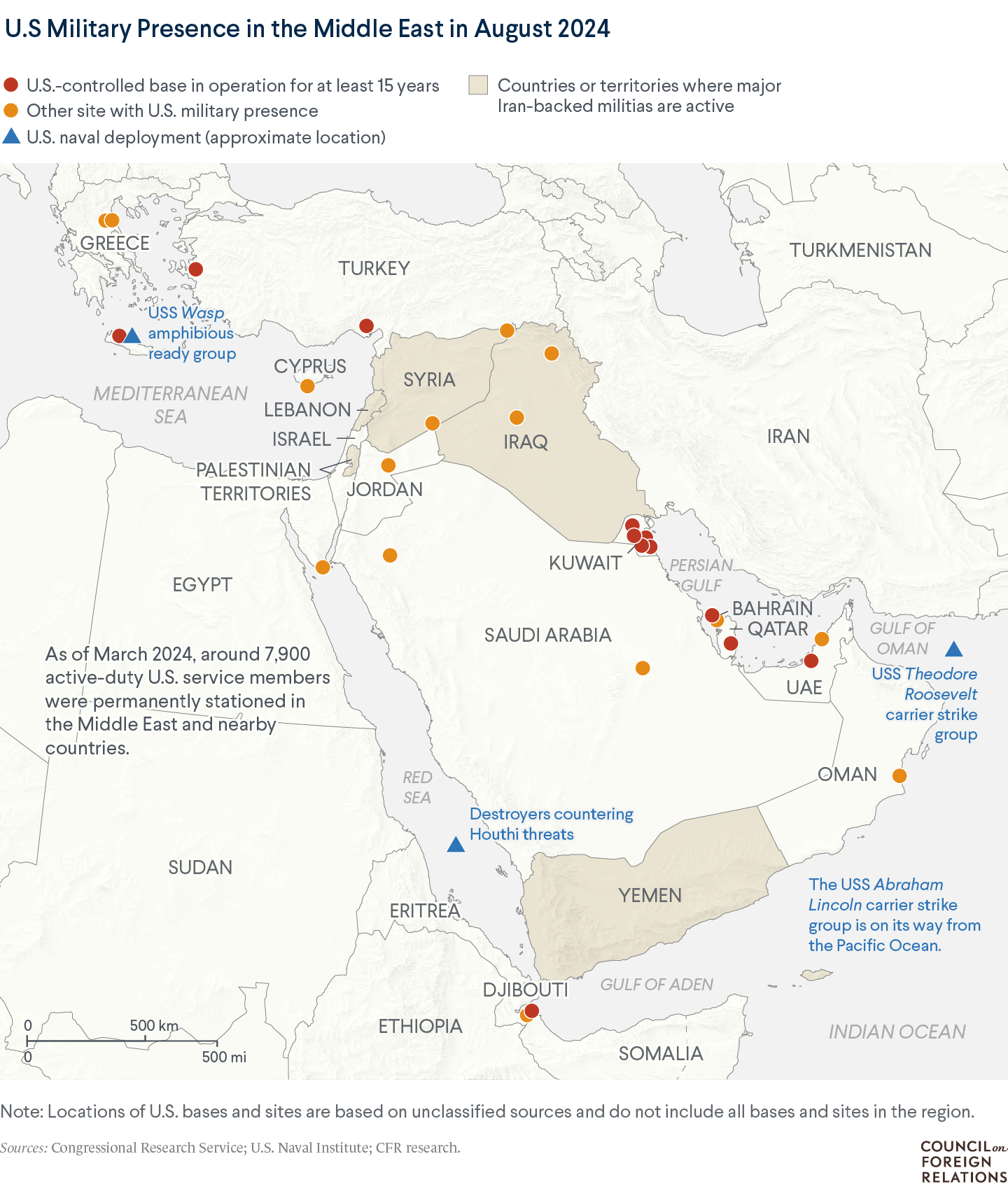

The energy crisis has created unprecedented disruptions to global supply chains. The Strait of Hormuz—through which approximately 20% of global oil and LNG flows pass—has effectively ground to a near-standstill [1][2]. This logistical choke point, combined with damage to Qatar’s Ras Laffan facility (the world’s largest LNG facility), has sent European natural gas prices surging 35% [4]. These supply disruptions have pushed Brent crude above $114/barrel, representing approximately a 50% increase since the conflict began [1][2].

The energy price shock has fundamentally altered the interest rate outlook. Bond traders have reversed course significantly, with market pricing now reflecting a 50% probability of a Federal Reserve rate hike by October [1][2]. This marks a dramatic shift from expectations of rate cuts that prevailed earlier in the year. The traditional inflation-fighting playbook faces a complex dilemma: while elevated energy prices typically pressure the Fed to tighten policy, a sufficient oil price spike could alternatively create financial conditions shock that would require rate cuts instead [1].

The K-shaped economy dynamics have been significantly exacerbated by the energy price surge, worsening economic bifurcation across income brackets and geographic regions [3]. This divergence creates additional challenges for policymakers attempting to craft appropriate responses.

Market technicals suggest the decline may not yet be complete. As noted by David Laut of Kerux Financial, “the market may not have yet found its bottom and is still in the process of sorting out and pricing in the duration of the Middle East conflict” [1][2]. This sentiment is reinforced by the fact that markets made new 2026 lows during the week, indicating continued downside momentum.

Traditional safe-haven assets have failed to provide protection during this crisis, a particularly troubling development for portfolio diversification strategies. Both bonds and gold have lost value, with gold headed for its worst weekly retreat since the pandemic onset [1]. Money market funds have emerged as the preferred safe haven among investors seeking capital preservation [1].

The escalation of military involvement suggests a prolonged conflict timeline that markets have not fully priced in. The Pentagon’s decision to deploy additional assets—three warships and thousands of Marines—indicates official expectations of an extended regional conflict rather than a rapid resolution [1][2]. Iranian leadership has reinforced this outlook, with Foreign Minister statements confirming “zero restraint” if infrastructure is struck again, and military warnings that retaliation will continue until “complete destruction” of U.S. and allied energy infrastructure [4].

The strategic importance of the Strait of Hormuz cannot be overstated. With approximately 20% of global oil and LNG flows dependent on this chokepoint, even partial disruption has outsized market implications. The U.S. is reportedly considering operations to take over Kharg Island, Iran’s major oil-export site, which would represent a significant escalation [1][2].

The energy sector has shown internal divergence, with companies like Chevron demonstrating relative insulation due to lower Middle East exposure [5]. This differentiation suggests opportunity for targeted sector allocation decisions, though overall market uncertainty remains elevated.

- Prolonged conflict risk: Iranian leadership has signaled zero restraint in continued attacks on energy infrastructure [4]

- Supply disruption escalation: Strait of Hormuz operations remain near standstill with no clear resolution timeline

- Inflation-Fed uncertainty: Conflicting pressures between energy-driven inflation and potential economic slowdown create policy ambiguity

- Traditional havens failing: Bonds and gold losing value simultaneously undermines portfolio protection strategies

- Technical breakdown: Market making new 2026 lows suggests potential for continued downside

- Energy sector differentiation provides selective allocation opportunities

- Money market funds offer interim capital preservation with competitive yields

- Potential Fed rate changes could create fixed income opportunities if inflation moderates

- Market dislocations may present long-term value entry points for patient investors

The fourth consecutive weekly stock decline reflects investor reassessment of the Middle East conflict timeline. Military developments—specifically the Pentagon’s deployment of additional warships and Marines—suggest no near-term resolution to the Iran war, extending what is now characterized as the largest disruption to oil supplies in history. Energy prices have responded dramatically: Brent crude above $114/barrel (up 50%), U.S. gasoline at $3.79/gallon (up 30% month-over-month), and diesel exceeding $5/gallon for the first time since 2022 [0][3]. The Strait of Hormuz remains near-total standstill, affecting 20% of global oil and LNG flows. Federal Reserve policy expectations have shifted dramatically, with bond traders now pricing a 50% chance of rate hike by October. Traditional portfolio hedges (bonds, gold) have failed to provide protection during this crisis period.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.