Low Private-Sector Debt Provides Economic Cushion Amid Market Volatility and Inflation Pressures

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

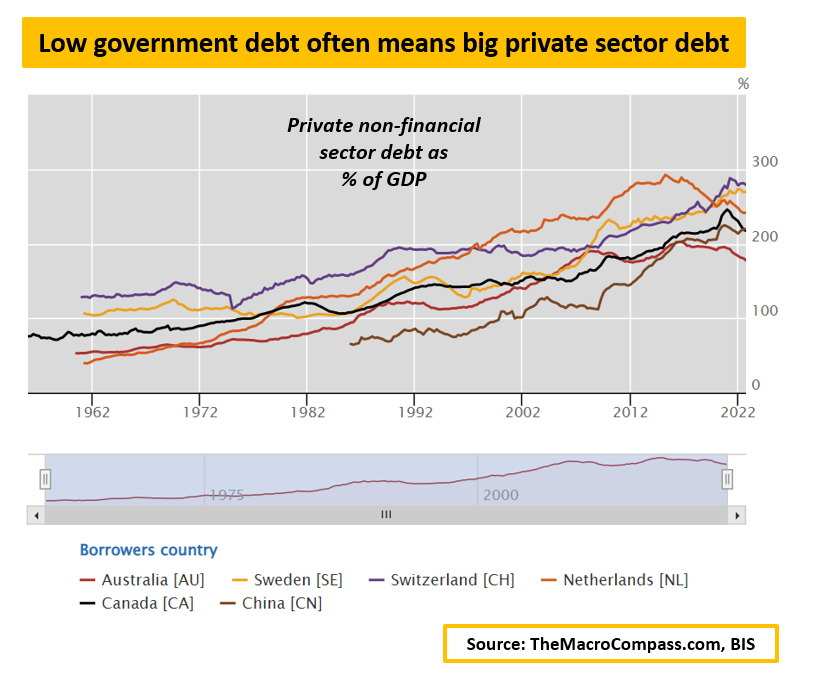

The Barron’s article presents a contrarian perspective amid mounting market concerns: that low household and business debt levels are providing meaningful economic “ballast” even as inflation accelerates and equity markets decline [1]. This thesis rests on recently released Q4 flow-of-funds data from the Federal Reserve, which reveals two critical metrics supporting this view:

-

Private Sector Liquidity Position: The private sector—comprising households and businesses—continued to strengthen its liquidity position relative to its debt burden [1]. This improvement suggests that the aggregate financial health of consumers and corporations remains resilient despite broader economic headwinds.

-

Banking System Fundamentals: At commercial banks, deposits relative to loans remain favorable, indicating robust banking system liquidity [1]. This metric is particularly significant as it suggests financial institutions are well-positioned to absorb potential credit losses while maintaining their lending capacity.

The timing of this analysis is notable. The article appeared on March 20, 2026, during a period when major equity indices were experiencing substantial declines [0]. The divergence between market performance and the underlying economic fundamentals as characterized by private-sector balance sheets presents an interesting analytical tension that warrants careful examination.

The market environment on the publication date provides essential context for interpreting this analysis [0]:

| Index | Daily Change | Closing Level |

|---|---|---|

| S&P 500 | -1.34% | 6,506.49 |

| NASDAQ Composite | -1.55% | 21,647.61 |

| Dow Jones Industrial | -0.87% | 45,577.48 |

| Russell 2000 | -2.24% | 2,438.45 |

Sector performance was broadly negative, with Utilities experiencing the steepest decline at -7.36%, followed by Technology (-2.03%) and Industrials (-1.90%). The sole sector showing relative resilience was Energy, declining just -0.08% [0]. This breadth of selling pressure across multiple sectors suggests investor concerns extend beyond any single economic factor.

The article’s investment commentary extends beyond the core thesis to address several notable market developments [1]:

The central insight from this analysis is that market price action and underlying economic fundamentals may be diverging meaningfully. While equity markets are pricing in significant uncertainty—reflected in the broad-based sector declines on March 20, 2026—the private sector’s balance sheet strength suggests that consumer and business spending capacity remains intact [1].

This disconnect between market sentiment and fundamental economic health has important implications for analytical frameworks that rely heavily on real-time market pricing as economic indicators. The flow-of-funds data represents a滞后 (lagging) indicator that may provide a more stable picture of economic capacity than volatile daily market movements.

The analysis reveals interesting risk transmission patterns across asset classes:

- Equity Markets: Broad declines indicate investor risk aversion and concerns about future earnings growth or valuations

- Fixed Income/Utilities: The steep 7.36% decline in Utilities may reflect concerns about interest rate sensitivity or inflation impacts on regulated earnings

- Commodities: The gold selloff demonstrates that even safe-haven assets can experience selling pressure when tariff policies create uncertainty about inflation trajectories

- Banking Sector: Despite concerns about stagflation impacts on bank profitability [6], deposit-to-loan ratios remain favorable

Federal Reserve Vice Chair Michelle Bowman recently signaled expectations for three interest rate cuts before year-end 2026 [5], suggesting monetary policy may provide some accommodation even as inflation remains elevated. This policy backdrop, combined with strong private-sector balance sheets, creates a complex environment where traditional economic relationships may not hold in their historical patterns.

-

Strong Consumer Balance Sheets: Low household debt relative to assets and income provides spending capacity that can support economic activity even during periods of market volatility

-

Business Sector Resilience: Favorable deposit-to-loan ratios at banks suggest businesses maintain access to credit and have not over-leveraged their balance sheets

-

Monetary Policy Optionality: The Fed’s signaled rate cuts provide potential support for economic activity going forward

-

Inflation Persistence: If price increases continue accelerating, even strong balance sheets may be eroded as purchasing power declines [1]

-

Labor Market Trajectory: Fed officials have expressed concerns about potential labor market weakening [5], which could eventually impact household income even without balance sheet deterioration

-

Commercial Credit Growth: Commercial and industrial loans have risen 5% year-over-year—the fastest pace in almost three years [6]—suggesting some segments may be increasing leverage

-

Geopolitical Uncertainty: Ongoing Iran conflict and tariff implementation could disrupt economic activity in unpredictable ways [4]

-

Corporate Profitability Pressures: The Alibaba example illustrates how technology companies face significant headwinds when growth strategies fail to resonate with investors [3]

The analysis suggests several near-term monitoring points:

- Quarterly flow-of-funds releases will provide ongoing updates on private-sector balance sheet trends

- Consumer spending data will reveal whether strong balance sheets translate into maintained consumption

- Banking system stress indicators will signal if the favorable deposit-to-loan ratios are deteriorating

- Trade policy developments will continue to impact commodity markets and international commerce

This Barron’s analysis [1] presents a perspective that low private-sector debt levels are providing economic resilience amid current market turbulence and inflation concerns. The thesis is supported by Q4 Federal Reserve flow-of-funds data showing improving private-sector liquidity relative to debt and favorable banking system deposit-to-loan ratios.

The market context on the publication date (March 20, 2026) showed significant declines across major indices [0], creating an interesting contrast with the constructive fundamental message. The article also addressed several investment themes including Sunbelt REITs, Chinese AI challenges (exemplified by Alibaba’s 67% profit decline), and the gold ETF selloff triggered by tariff news.

Risk factors to monitor include potential inflation erosion of purchasing power, labor market deterioration, rising commercial credit growth, and geopolitical uncertainties. The Federal Reserve’s signaled three rate cuts before year-end 2026 [5] may provide some economic support, though the ultimate trajectory will depend on how these various factors interact.

The analysis represents one perspective among market commentary and should be evaluated alongside other economic indicators and analytical frameworks when forming views on the economic outlook.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.