Middle East Escalation Triggers Global Risk-Off: Oil Surge, Stock Decline, Yield Spike

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on the Wall Street Journal report [1] published on March 23, 2026, which documented a significant shift in global market sentiment driven by weekend developments in the Middle East conflict. The market data reveals a comprehensive risk-off environment affecting equities, bonds, and commodities simultaneously [0].

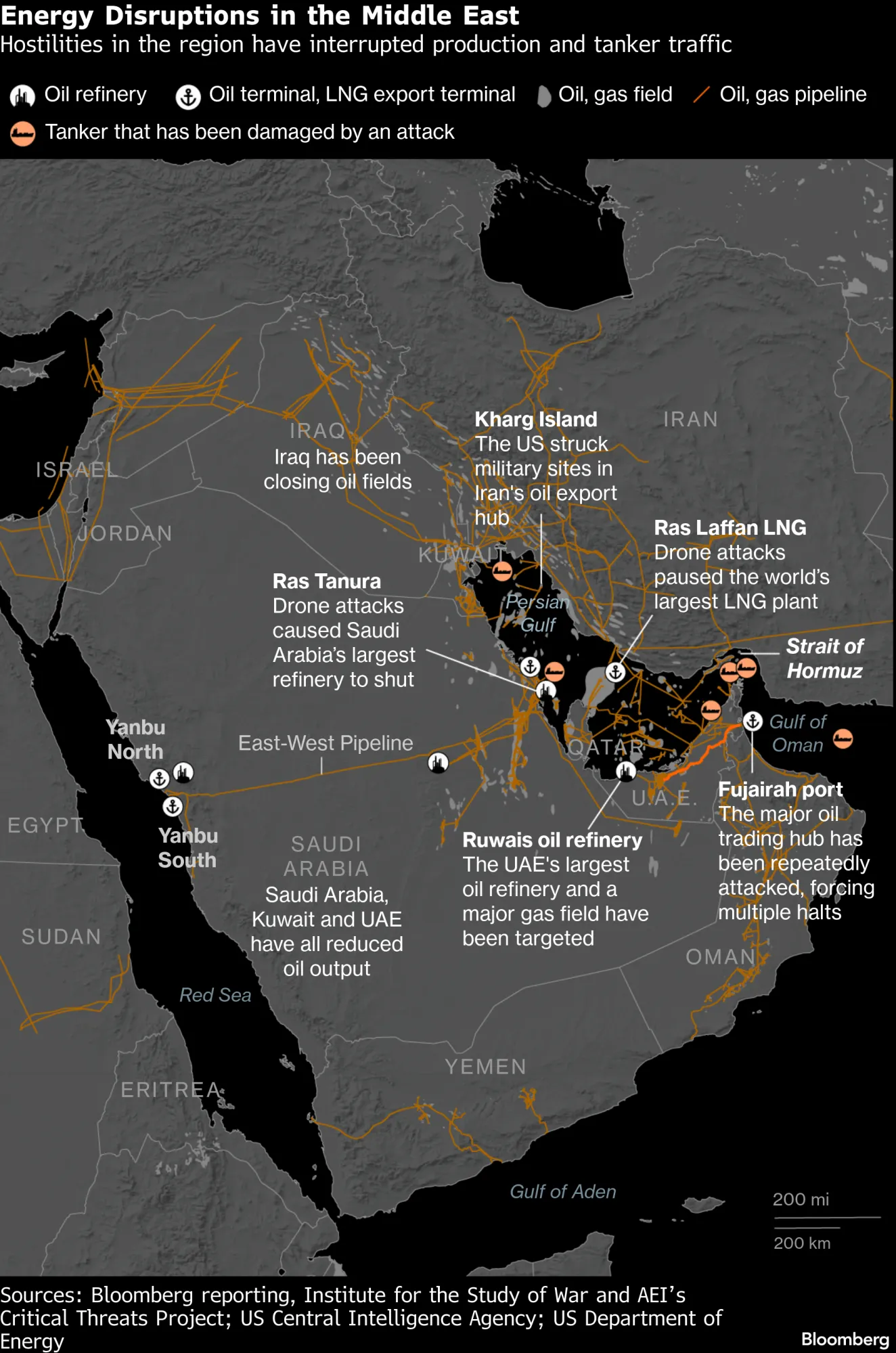

The escalation represents a dramatic intensification of geopolitical tensions, with the U.S. military having struck more than 7,000 targets across Iran according to UN News [5] and CBS News [6]. The attacks on energy infrastructure—including an oil refinery in Kuwait and the Ras Laffan LNG facility in Qatar—have created substantial concerns about global energy supply disruption. Trump issued a 48-hour ultimatum demanding Tehran reopen the Strait of Hormuz, further elevating market anxiety [5][6].

The March 20 trading session demonstrated widespread market weakness across all major indices [0]:

| Index | March 20 Close | Daily Change |

|---|---|---|

| S&P 500 | 6,506.49 | -1.34% |

| NASDAQ | 21,647.61 | -1.55% |

| Dow Jones | 45,577.48 | -0.87% |

| Russell 2000 | 2,438.45 | -2.24% |

The Russell 2000’s 2.24% decline—the steepest among major indices—indicates that small-cap stocks experienced the most severe pressure, suggesting the risk-off sentiment is broadening beyond large-cap equities [0]. This small-cap weakness historically correlates with heightened investor concerns about economic growth trajectories.

Sector performance data reveals a clear pattern of rotation away from rate-sensitive and growth-oriented sectors [0]:

- Worst Performers:Utilities (-7.36%), Technology (-2.01%), Industrials (-1.90%)

- Best Performers (Relative):Energy (-0.08%), Financial Services (-0.56%)

The Utilities sector’s dramatic 7.36% decline reflects its dual sensitivity to both interest rate concerns and economic slowdown fears—a classic stagflationary signal. Technology’s 2.01% decline aligns with the sector’s rate sensitivity, as higher yields compress growth stock valuations. The Energy sector’s relative resilience at -0.08% directly reflects the positive impact of elevated oil prices on energy company fundamentals [0].

Treasury yields rose significantly as markets digested the geopolitical developments and their implications for Federal Reserve policy [2][3][4]. The bond market experienced what analysts characterize as a “bear flattening” yield curve movement—where short-term yields rise faster than long-term yields—indicating simultaneous concerns about near-term inflation pressures and longer-term economic growth [4].

This yield curve dynamics suggests traders are inferring a hawkish read from the Federal Reserve’s recent communications while simultaneously pricing in potential economic headwinds [2][3]. The interplay between war-driven inflation concerns and potential growth deceleration creates a particularly challenging environment for fixed income investors.

The geopolitical escalation has produced dramatic oil price movements that represent a significant shock to global energy markets [5][6][7]:

- Brent crudebriefly topped$119 per barrelon Thursday before settling above $100/barrel [5][6]

- The spread between Brent and WTI exceeded $14/barrel—the steepest difference in years [5]

- Qatar warned that LNG export capacity could fall following attacks on the Ras Laffan facility [5]

- Energy infrastructure attacked in Kuwait (oil refinery), Qatar (LNG facility), and Iran [5][7]

As reported by the New York Times [7], damage to Persian Gulf energy infrastructure could significantly hurt global supply and make recovery more difficult when the conflict ends, potentially creating longer-term price support even after hostilities cease. This represents a structural shift in risk premium rather than a temporary shock.

The war-driven oil shock creates a profoundly challenging policy dilemma for the Federal Reserve [2][3]. The Morningstar analysis [3] captures this tension: “While companies can adjust to gradual rises in oil prices, they’re less able to quickly change their business models after a spike turns into a long-term new normal.”

- Near-term inflation concerns:Higher oil prices push inflation expectations upward, traditionally suggesting rate hikes

- Medium-term growth concerns:If elevated energy prices persist, they could drag on economic growth, potentially forcing rate cuts rather than hikes

Market pricing for Federal Reserve rate cuts in 2026 has diminished significantly [2][3], reflecting uncertainty about the policy path. Upcoming Fed communications will be critical in establishing how the central bank balances these competing imperatives.

The market response demonstrates a classic risk-off pattern with several interconnected dynamics:

-

Equity-Bond Correlation Shift:The simultaneous decline in stocks and bonds (rising yields) represents a departure from the correlation pattern that characterized much of recent market history, suggesting a fundamental recalibration of risk premiums.

-

Sector Rotation Pattern:The rotation away from Utilities and Technology toward Energy reflects market participants attempting to position for stagflationary conditions—a challenging environment where both growth and margins are pressured.

-

Small-Cap Sensitivity:The Russell 2000’s outsized decline (-2.24%) suggests investors are increasingly concerned about the economic growth outlook, as smaller companies are typically more sensitive to domestic economic conditions.

- Continued military escalation could push oil above $120/barrel, intensifying inflation pressures

- Further Treasury yield increases could pressure equity valuations, particularly in growth sectors

- Stagflationary concerns may intensify, creating a challenging environment for risk assets

- Strait of Hormuz disruption would represent an existential threat to global oil supply

- Sustained high energy prices could compress corporate profit margins across multiple sectors

- Consumer spending may be impacted by higher gasoline and heating costs, filtering through the broader economy

- Global supply chain disruptions possible if conflict spreads beyond current boundaries

- Earnings guidance from companies regarding input cost pressures will be critical to monitor

- The VIX volatility index likely elevated (intraday data not available at time of analysis)

- Small-cap weakness suggests risk-off sentiment is broadening

- Growth and rate-sensitive sectors underperforming most significantly

While the current environment is predominantly challenging, several considerations warrant attention:

-

Energy Sector Positioning:The Energy sector’s relative resilience (-0.08% vs. -7.36% for Utilities) suggests market participants are already pricing in elevated oil prices. Further oil price increases could continue to benefit energy equities.

-

Volatility Premium:Elevated market volatility typically increases option premiums, potentially creating opportunities for volatility-based strategies for sophisticated investors.

-

Defensive Positioning:Companies with strong balance sheets, pricing power, and limited energy input exposure may represent relative value in a risk-off environment.

-

Duration of Conflict:Historical precedent suggests that Middle East conflicts with limited duration have historically seen market recoveries. The key variable is whether oil prices remain elevated for an extended period.

The global market response to Middle East escalation on March 23, 2026, reflects a comprehensive risk-off environment driven by several interconnected factors:

- S&P 500: 6,506.49 (-1.34%)

- NASDAQ: 21,647.61 (-1.55%)

- Russell 2000: 2,438.45 (-2.24%)

- Brent crude: briefly topped $119/barrel, settled above $100

- Brent-WTI spread: exceeded $14/barrel

- Worst sector: Utilities (-7.36%)

- Best relative sector: Energy (-0.08%)

- U.S. military strikes: 7,000+ targets across Iran

- Energy infrastructure attacked in Kuwait, Qatar, Iran

- Trump ultimatum regarding Strait of Hormuz

- First week military operations cost: ~$11.3 billion

- Fed rate cut expectations diminished for 2026

- Market pricing reflects uncertainty between inflation and growth concerns

- Bear flattening yield curve indicates near-term inflation, longer-term growth concerns

The synthesis of this information suggests markets are processing a significant geopolitical shock with uncertain duration and implications. The trajectory of oil prices, Federal Reserve communications, and Middle East developments will be the primary determinants of market direction in the coming weeks.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.