U.S.-Iran Geopolitical Crisis: Fixed Income Market Drivers and Portfolio Protection Strategies

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

This analysis is based on the Cooper Howard commentary from Charles Schwab published on YouTube on March 23, 2026 [1], which provides timely guidance on navigating fixed income markets during an active geopolitical crisis.

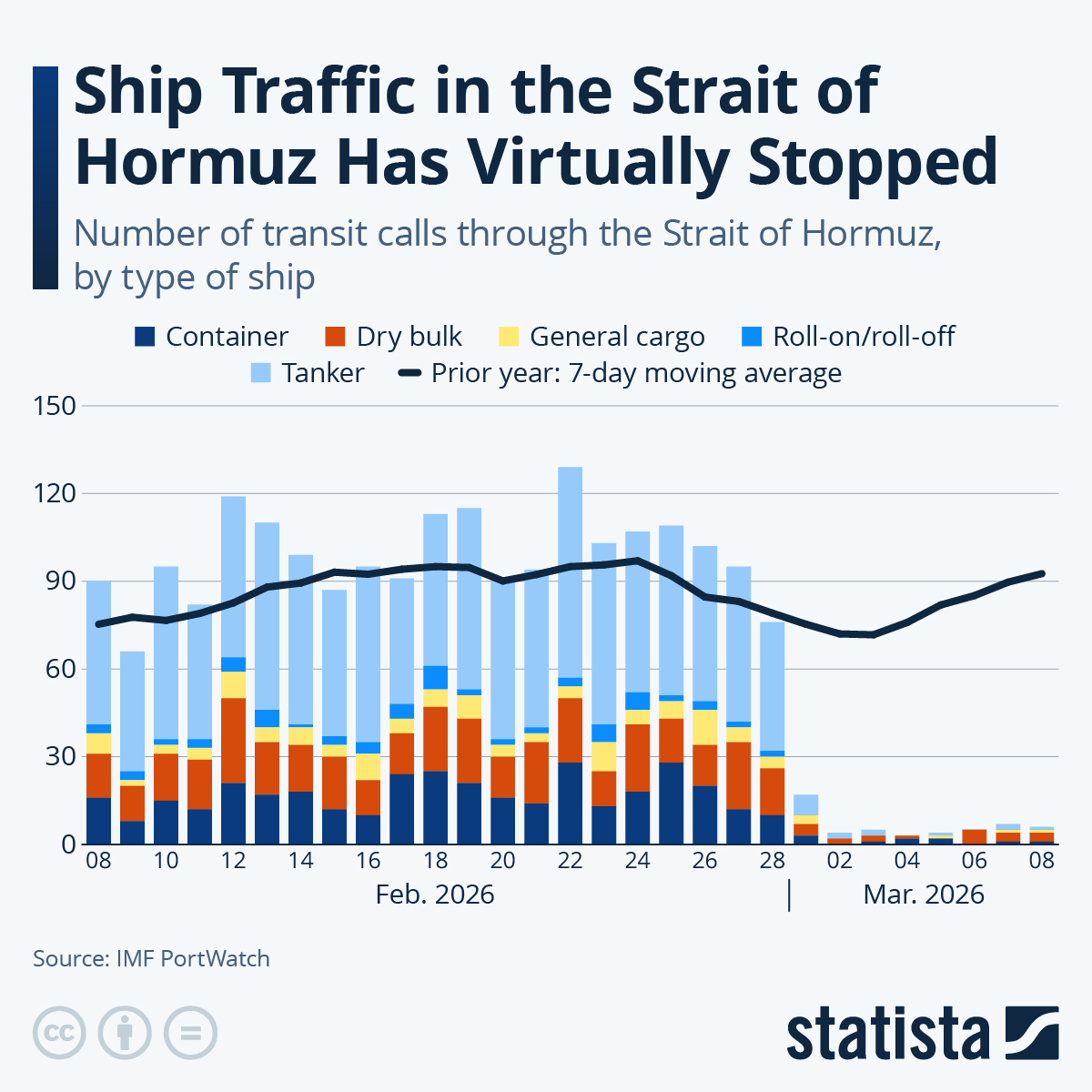

The U.S.-Iran conflict has entered its fourth week, creating unprecedented disruption to global energy markets. The Strait of Hormuz—through which approximately 20% of the world’s oil passes—remains effectively closed, representing what the International Energy Agency has characterized as the largest supply disruption in global oil market history, exceeding the severity of the 1970s oil crises [3]. This development creates a direct pipeline from geopolitical risk to fixed income market dynamics through multiple transmission mechanisms.

The current market environment demonstrates heightened volatility with meaningful index movements. Recent market data [0] shows significant drops on March 18 and 20, with partial recovery attempts on March 19 and 23. The S&P 500 declined 1.34% on March 20 while NASDAQ fell 1.55%, reflecting investor uncertainty about the conflict’s trajectory [0]. These movements underscore Cooper Howard’s emphasis on investors “hunkering down” while maintaining awareness of headline developments surrounding U.S. and Iran relations.

According to the Charles Schwab analysis, several key drivers are currently moving fixed income markets:

Cooper Howard’s guidance emphasizes avoiding “outsized bets” in this environment—a recommendation that reflects the high uncertainty surrounding the conflict’s resolution. The March 23 deadline for Trump’s 48-hour ultimatum regarding the Strait of Hormuz adds temporal urgency to this guidance [2].

Key portfolio considerations include:

- Duration Positioning: Balancing yield capture against potential rate volatility

- Credit Quality: Emphasizing higher-quality fixed income amid corporate earnings uncertainty

- Currency Exposure: Dollar strength dynamics as a traditional geopolitical hedge

- Liquidity Management: Maintaining flexibility to respond to headline developments

The analysis reveals strong interconnections between geopolitical developments and fixed income market mechanics. Oil price volatility serves as the primary transmission mechanism, linking headline geopolitical events to inflation expectations, Fed policy trajectories, and ultimately Treasury yield movements. The current situation demonstrates how energy supply disruptions can rapidly cascade through economic systems—elevated fertilizer costs are already feeding into global production chains [3], creating secondary inflation pressures beyond direct energy costs.

The unprecedented closure of the Strait of Hormuz represents a structural shift in global energy markets rather than a temporary disruption. This reality means fixed income investors must account for sustained elevated energy prices in their inflation assumptions, potentially altering the duration calculus that had been favoring rate-sensitive positioning earlier in the year.

The March 23 deadline referenced in the analysis creates acute headline risk for investors. Market sentiment has shown rapid swings between escalation fears and de-escalation hopes—oil prices fell on March 23 following reports of “productive” conversations between Trump and Iranian officials [4]. This volatility pattern reinforces the importance of Cooper Howard’s recommendation to avoid outsized reactive trades.

The integration of Cooper Howard’s fixed income guidance with current market data and geopolitical context reveals a market environment defined by elevated uncertainty and significant headline risk. The fourth-week U.S.-Iran conflict has created structural disruptions to global energy supplies, with the Strait of Hormuz closure representing the most significant supply shock in modern oil market history [3].

For fixed income investors, the key takeaways center on defensive positioning without complete de-risking. Maintaining adequate liquidity, avoiding outsized position changes in response to headlines, and focusing on credit quality align with the “heads on a swivel” approach recommended by Cooper Howard. The Federal Reserve’s policy path—already complicated by pre-conflict inflation concerns—faces additional uncertainty from war-driven energy price pressures, suggesting rate cuts may be further delayed beyond market expectations.

The temporal proximity of the March 23 deadline for the Strait of Hormuz ultimatum creates particular urgency for headline monitoring. However, the market’s demonstrated capacity for rapid sentiment shifts—evidenced by oil’s response to diplomatic developments—underscores the importance of disciplined position management rather than reactive trading.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.