DFLI Market Analysis: Delisting Risk vs. Operational Growth Catalysts

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

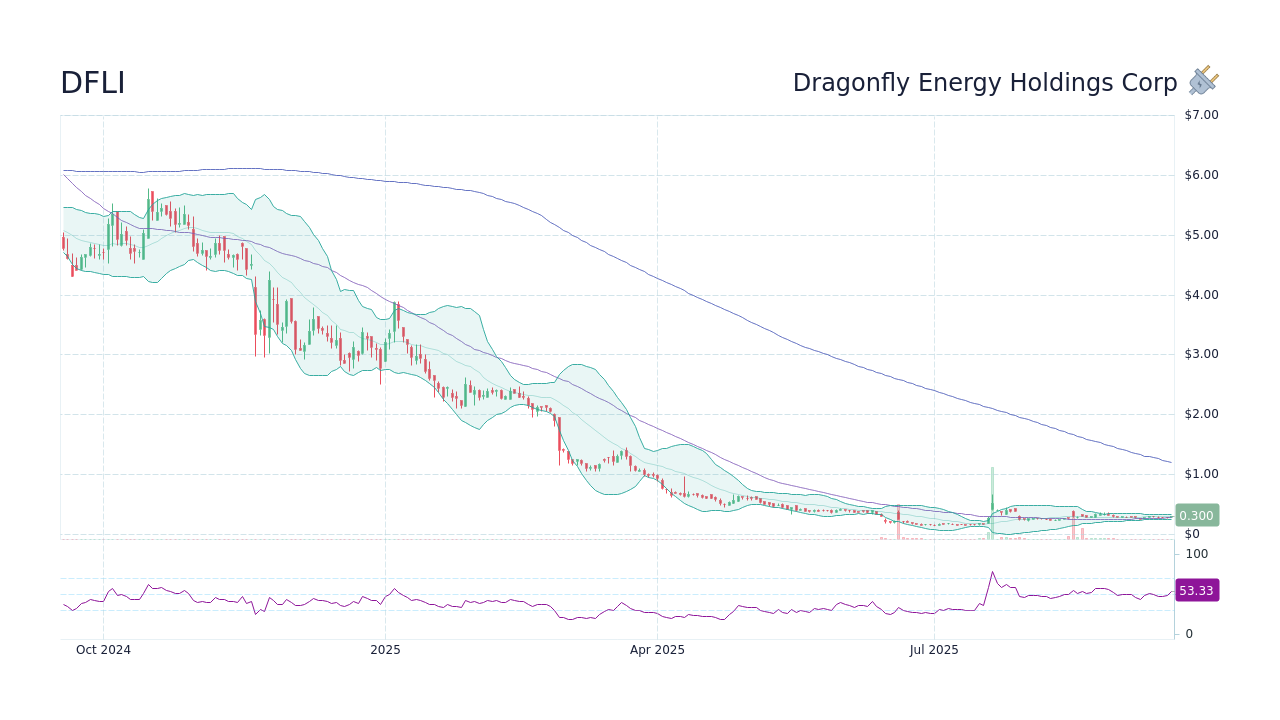

This analysis is based on a Reddit post discussing DFLI’s investment thesis [1]. DFLI’s Q3 2025 results show strong operational performance: 26% YoY revenue growth to $16M, ~30% gross margin (up 700 bps), and debt reduction to $19M with $30M cash [0]. However, the stock price has dropped 22.87% since Nov 6 to $0.85, below the $1 Nasdaq threshold, with a delisting deadline of Dec 19 [0]. The market has not priced in operational positives due to delisting overhang.

- Disconnect Between Fundamentals and Price: Operational improvements (Q3 growth, margin expansion) are overshadowed by delisting risk.

- Volatility Potential: Short interest of 11.71% [0] could lead to sharp price swings if delisting risk is addressed.

- Long-Term Catalysts: 2026 trucking segment growth and solid-state battery plans are positive but not immediate [0].

- Risks: Delisting (if no action by Dec19), dilution from equity offerings [0].

- Opportunities: Operational growth (OEM sales up 44% YoY [0]), long-term solid-state battery commercialization.

- Current Price: $0.85 [0]

- Q3 Revenue: $16M (26% YoY) [0]

- Gross Margin: ~30% [0]

- Short Interest: 11.71% [0]

- Delisting Deadline: Dec19 [1]

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.