Market Rebalancing Advisory After 60%+ Stock Gains Since 2022

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis is based on a CNBC report [1] published on November 5, 2025, which highlights financial advisors’ recommendations for portfolio rebalancing after major stock indexes posted gains exceeding 60% since mid-October 2022. The report emerges during a period of increasing market volatility and growing concerns about overvaluation, particularly in technology and AI-related sectors.

Market data confirms the substantial rally referenced in the advisory [0]. Since October 17, 2022, through November 4, 2025:

- S&P 500: +86.10% (from $3,638.65 to $6,771.54) [0]

- NASDAQ Composite: +120.78% (from $10,575.65 to $23,348.64) [0]

- Dow Jones Industrial: +56.64% (from $30,059.58 to $47,085.25) [0]

- Russell 2000: +42.69% (from $1,701.16 to $2,427.34) [0]

The technology sector has been the primary driver, with AI-related stocks leading the extended rally. However, this concentration has created significant allocation drift for investors who established their portfolios before the bull market began.

Recent trading sessions reveal emerging valuation concerns that support the rebalancing recommendation [0]:

- November 4, 2025: S&P 500 declined 1.17%, Nasdaq dropped 2.04%, driven by AI valuation concerns [2]

- November 5, 2025: Continued pressure on technology stocks with Bitcoin falling 6% and Ether plunging 11%, indicating broader risk-off sentiment [3]

Sector performance divergence is becoming apparent, with defensive sectors showing relative strength:

- Consumer Defensive: +0.64% [0]

- Basic Materials: +0.32% [0]

- Technology: -0.50% [0]

- Financial Services: -0.74% [0]

Multiple Wall Street CEOs have recently issued warnings about potential market corrections, creating a consensus among institutional leaders [2]:

- Goldman Sachs CEO David Solomon: Predicts “10 to 20% drawdown in equity markets sometime in the next 12 to 24 months”

- Morgan Stanley CEO Ted Pick: Expects “10 to 15% drawdowns that are not driven by some sort of macro cliff effect”

- JPMorgan Chase CEO Jamie Dimon: Previously warned about “a significant stock market correction within the next six months to two years”

This convergence of institutional warnings coincides with the rebalancing advisory, suggesting growing professional consensus about market risk levels.

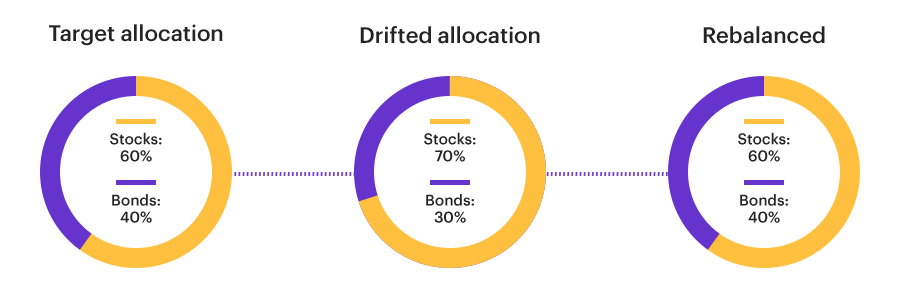

A 60/40 stock/bond portfolio established in October 2022 would now be significantly overweight equities due to the market rally [1]. For example:

- Initial $100,000 portfolio: $60,000 stocks, $40,000 bonds

- After 86% stock gains: $111,600 stocks, $40,000 bonds = 73.6% stocks, 26.4% bonds

- This represents a 13.6 percentage point drift from the original target allocation

James Armstrong, president of Henry H. Armstrong Associates (ranked No. 14 on CNBC’s Financial Advisor 100 list), warns that investors “could have too much in equities and not enough in safe assets” [1].

The rebalancing need varies significantly by investor age and time horizon [1]:

- Younger investors: May maintain higher equity exposure despite gains due to longer recovery timeframes

- Near-retirement investors: Face critical timing risk as Armstrong emphasizes they “don’t have the time to recover from a prolonged down market”

- Overvaluation Concentration: Technology and AI-related stocks appear particularly vulnerable after leading the rally for extended periods [2][3]

- Correction Probability: Multiple major bank CEOs predicting 10-20% corrections in the next 12-24 months [2]

- Allocation Drift Risk: Investors who haven’t rebalanced may have excessive exposure to growth stocks, creating unintended risk concentrations

- Tax Efficiency Concerns: Large embedded gains in concentrated positions make future rebalancing potentially more costly from a tax perspective [1]

- Systematic Rebalancing: Benjamin Offit, CFP, recommends removing emotion through systematic rebalancing strategies [1]

- Tax Loss Harvesting: Current market declines provide opportunities to offset gains with strategic losses

- Diversification Enhancement: Rebalancing allows investors to reduce concentration risk while maintaining market exposure

Decision-makers should closely track:

- Valuation Metrics: P/E ratios, particularly in technology sectors showing signs of compression

- Interest Rate Environment: Federal Reserve policy changes affecting bond yields and equity valuations

- Institutional Flow Patterns: Large-scale rebalancing by pension funds and endowments that could trigger market movements

- Volatility Indicators: VIX levels and options market positioning suggesting changing risk perceptions

The rebalancing recommendation is supported by several technical and fundamental factors [1]:

- Risk Management: Portfolio allocation drift has created unintended risk exposures that may not align with investors’ original risk tolerance

- Tax Efficiency: Regular rebalancing helps manage capital gains by preventing large, concentrated positions that become difficult to sell due to high embedded tax costs

- Systematic Approach: Most advisors recommend rebalancing at least annually, with Armstrong suggesting “a couple times a year or maybe more” [1]

The advisory emerges during a period of:

- Extended Market Gains: Three years of above-average returns across major indexes

- Valuation Concerns: Growing consensus about overvaluation, particularly in technology sectors

- Institutional Warnings: Multiple bank CEOs publicly discussing potential corrections

- Recent Volatility: Emerging market stress signals in high-growth sectors

While not providing specific investment recommendations, the analysis suggests that current market conditions warrant:

- Review of asset allocation targets relative to current portfolio composition

- Assessment of risk tolerance in light of extended market gains

- Consideration of tax-efficient rebalancing strategies

- Evaluation of diversification across sectors and asset classes

The convergence of advisor recommendations, institutional warnings, and market stress signals creates a compelling case for portfolio reassessment, though individual circumstances should guide specific actions.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.