DTE Energy: Data Center Partnerships and Business Model Transformation

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

Based on comprehensive analysis of DTE Energy’s data center partnerships, financial metrics, and growth trajectory, I can provide a detailed assessment of whether these partnerships can drive sustainable earnings growth and transform its business model.

DTE Energy is undergoing a significant transformation driven by its hyperscale data center partnerships, most notably the landmark agreement to power Oracle’s Stargate OpenAI data center in Saline Township, Michigan. This deal, combined with a robust pipeline of additional data center projects, positions DTE to potentially redefine its business model beyond traditional regulated utility operations [1][2].

DTE’s most significant partnership is the agreement to provide

- 25% of DTE’s total electric load— a single customer adding massive scale

- Equivalent to the output of a nuclear reactor or enough power for approximately one million homes

- Over 2,500 union construction jobsprojected for the build-out

The contract structure is particularly compelling from an investment perspective:

“The agreement is structured with minimum monthly charges that cover 80% of the billing demand. This take-or-pay feature is crucial. It means DTE gets paid for the capacity, whether the AI servers are running at full speed or sitting idle.” [2]

This effectively functions as a

DTE is actively pursuing a substantial pipeline of hyperscale data center projects:

| Metric | Value |

|---|---|

| Active proposals (2025-2026) | 10-15 hyperscale projects |

| Total power allocation sought | 4.4+ GW |

| Equivalent nuclear plants | ~6 Palisades Nuclear Plants |

| Additional load in advanced discussions | 3 GW |

DTE’s Q4 2025 performance demonstrates strong execution:

| Metric | Actual | Estimate | Surprise |

|---|---|---|---|

| EPS | $1.65 | $1.52 | +7.14% |

| Revenue | $4.24B | $3.39B | +25.12% |

The stock responded positively, rising approximately 2.8% on the day of the report [2].

Management issued robust guidance projecting

- Tax credits from Renewable Natural Gas (RNG) business

- Infrastructure investments supporting data center load

- Rate base expansion from capital expenditure program

| Metric | Value | Sector Context |

|---|---|---|

| P/E Ratio (TTM) | 21.15x | Premium vs typical 16-18x for slower-growth utilities |

| P/B Ratio | 2.51x | Reflects infrastructure asset value |

| Market Cap | $31.05B | Mid-cap utility |

| Dividend Yield | ~3.2% | 16 consecutive years of increases |

| Beta | 0.43 | Defensive, low correlation to market |

DTE announced a

“In the utility business model, capital expenditure is the engine of profit. Because utilities are regulated monopolies, they are authorized to earn a specific return on equity (ROE) on every dollar they invest in the grid.” [2]

The capital spending directly expands the

The capital program supports:

- Grid modernization for AI/hyperscale data center loads

- Renewable energy expansion (wind, solar)

- Natural gas infrastructure upgrades

- Reliability improvements

DTE’s positioning represents a meaningful evolution from traditional regulated utility toward

| Traditional Utility Model | DTE’s Emerging Model |

|---|---|

| Steady, predictable earnings | High-volume data center contracts |

| Residential/commercial customer base | Hyperscale anchor tenants |

| Rate case-driven growth | Take-or-pay contract structure |

| Low-beta defensive play | AI economy exposure with infrastructure returns |

As articulated by market analysts:

“Where Should You Invest $1,000 Right Now… DTE Energy stands as the adult in the room. For investors seeking exposure to AI without the vertigo of high valuations, the power grid is the ultimate physical hedge.” [2]

This reflects the unique value proposition:

- Contract language change from cost-coverage guarantee to aggregate revenue arrangement

- Concern that residential ratepayers could subsidize infrastructure in early years

- DTE argues the project will eventually save customers $300 million[2]

- $100 million civil penaltyordered by federal judge for environmental violations at Zug Island

- Context: Manageable relative to ~$1.5B in annual operating earnings, representing a one-time liquidity impact rather than structural threat [2]

- Aggressive rate increases ($242.4 million approved, another hike planned for 2027)

- Public transparency concerns regarding NDAs with municipalities

- Political opposition to data center expansion in local communities

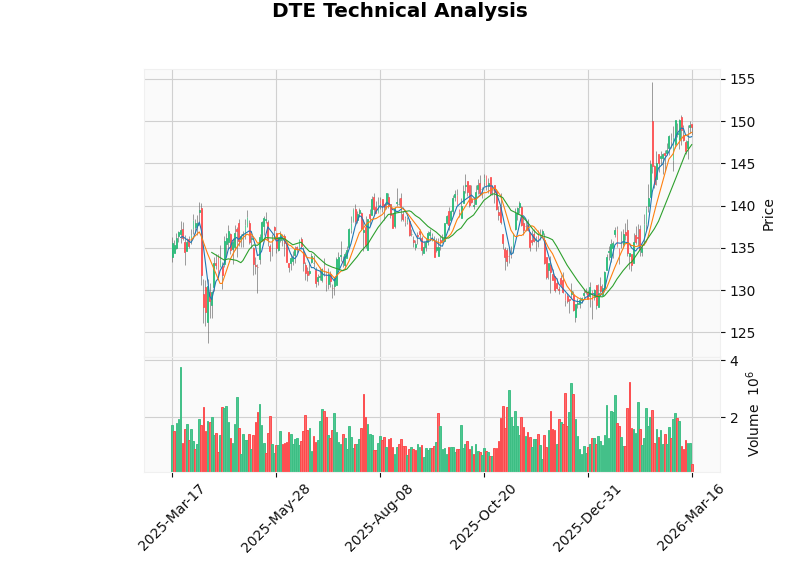

| Indicator | Value | Signal |

|---|---|---|

| Current Price | $149.36 | — |

| Support Level | $147.23 | — |

| Resistance Level | $150.75 | — |

| MACD | No cross | Bearish |

| KDJ | K:68.6, D:67.0 | Bullish |

| RSI (14) | Normal range | Neutral |

| Trend | Sideways | No clear direction |

The stock is currently trading in a

| Scenario | Fair Value | Upside vs Current |

|---|---|---|

| Conservative | $772.52 | +417.1% |

| Base Case | $989.65 | +562.4% |

| Optimistic | $3,274.42 | +2,091.7% |

| Probability-Weighted | $1,678.86 | +1,023.7% |

- Beta: 0.43 (low risk)

- Cost of Equity: 7.5%

- WACC: 5.5%

The DCF analysis suggests significant intrinsic value, though current market price reflects more conservative assumptions [0].

- Contractual Revenue Certainty: The 80% take-or-pay structure provides guaranteed minimum revenue regardless of data center utilization

- Massive TAM Expansion: 4.4+ GW pipeline represents potential 6x growth in load from single vertical

- Visible Capital-Driven Growth: $36.5 billion capex plan through 2030 creates rate base expansion

- AI Tailwinds: Structural demand for compute power unlikely to reverse

- Defensive Characteristics: Low beta (0.43), 3.2% dividend yield, 16-year dividend growth streak

- Regulatory Uncertainty: AG opposition could delay or modify contract terms

- Rate Increase Backlash: Customer and political resistance to utility rate hikes

- Execution Risk: Meeting construction deadlines (e.g., July 2026 tax credit deadline)

- Competition: Other utilities pursuing similar data center strategies

The evidence suggests

-

Sustainable Earnings Growth: The 6-8% EPS guidance for 2026, combined with the contractual structure of data center deals, provides a visible growth pathway. The take-or-pay mechanism effectively derisks the revenue model.

-

Business Model Transformation: The Stargate deal represents a meaningful shift toward becoming an AI infrastructure provider rather than purely a traditional utility. The 25% load addition from a single customer is unprecedented in DTE’s history.

-

Key Differentiator: Unlike peers pursuing smaller data center projects, DTE is “whale-hunting” — securing massive singular projects that move the needle immediately [2].

-

Current Valuation: At 21x P/E with modest upside to analyst targets ($151.50), the stock prices in existing partnerships but may not fully reflect the optionality on the 4.4+ GW pipeline.

[1] DTE Energy - 2025 Accomplishments and Investments (https://www.dteenergy.com/us/en/newsroom/2026/DTE-Energy-reports-2025-accomplishments,-earnings-and-investments.html)

[2] MarketBeat - “DTE’s Stargate Deal Turns Power Into Profits” (https://www.marketbeat.com/originals/dtes-stargate-deal-turns-power-into-profits/)

[3] Yahoo Finance - “DTE Energy Boosts Growth With Strategic Clean Energy Investments” (https://finance.yahoo.com/news/dte-energy-boosts-growth-strategic-134200064.html)

[4] Planet Detroit - “Data center news: DTE Energy’s data center pipeline could require power of 6 nuclear plants” (https://planetdetroit.org/2026/03/dte-data-center-pipeline/)

[5] GuruFocus - “DTE Energy (DTE) Discusses 2026 Operating Earnings Guidance” (https://www.gurufocus.com/news/8692320/dte-energy-dte-discusses-2026-operating-earnings-guidance-in-investor-presentation)

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.