Triple Witching 2026 Meets Iran Conflict: $5.7 Trillion Options Expiration Coincides With Gulf Tensions

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

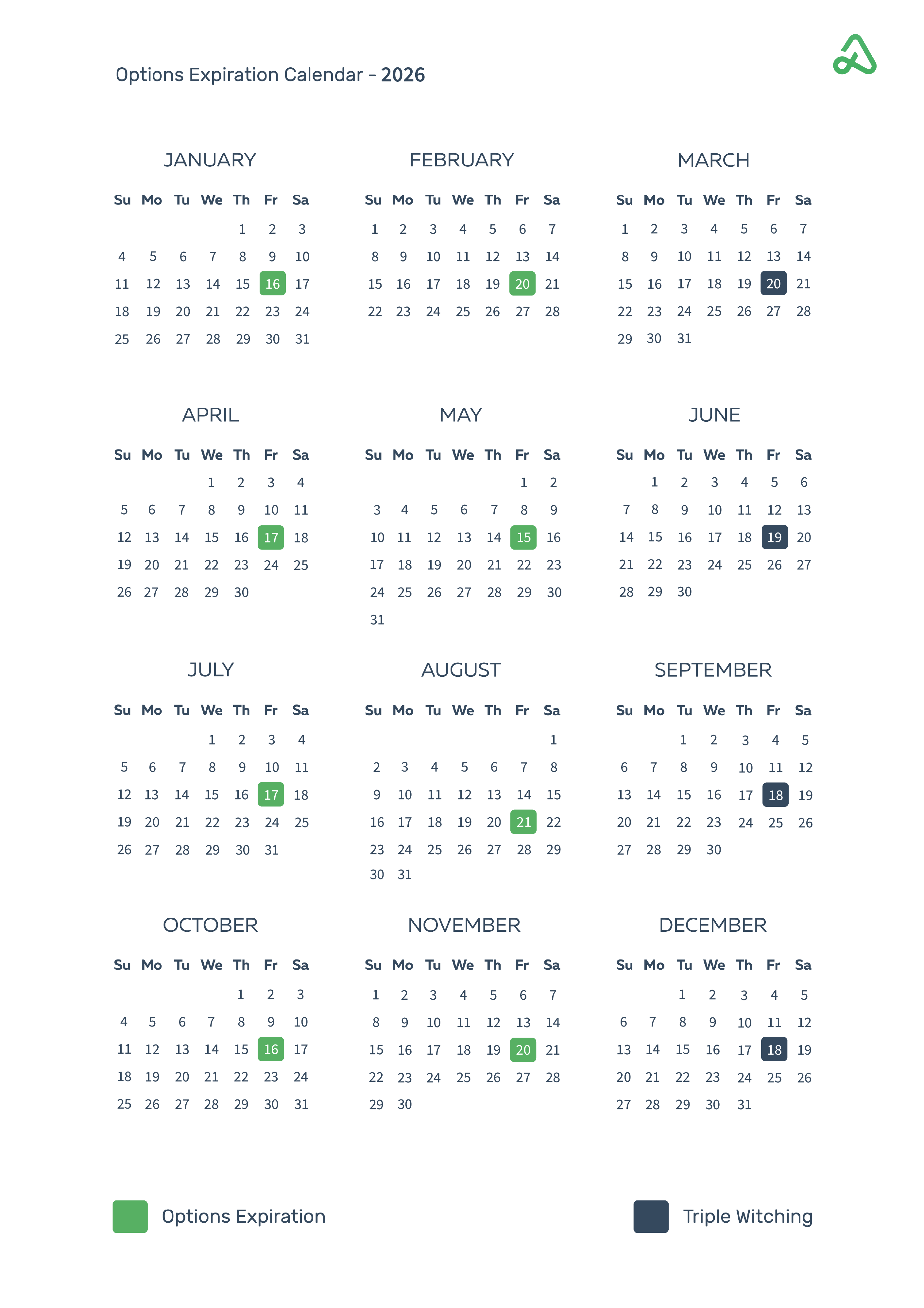

The convergence of three major market events on Friday, March 20, 2026 creates a uniquely volatile trading environment that warrants careful attention from investors and risk managers alike. The first triple witching of 2026 will see approximately

The geopolitical backdrop amplifies the technical market dynamics considerably. The ongoing US-Iran conflict has escalated to the point where analysts are warning about potential targeting of energy infrastructure in the Gulf region [3]. This geopolitical risk premium has kept oil prices elevated at $94.58 per barrel, though they have pulled back from recent highs. The conflict creates a complex catch-22 for policymakers, as any US action risks driving oil prices even higher, potentially triggering a broader market correction [3].

From a historical perspective, triple witching days have demonstrated consistently elevated volatility patterns. Data indicates these expiration events generate more than three times the normal trading volume, with the median S&P 500 return of

-

Expiration-Related Volatility: The $5.7 trillion notional options expiration creates significant gamma exposure that can amplify price movements in either direction. Historical patterns suggest elevated volatility persists through expiration and may create a “hangover” effect into Monday’s trading session as new positions are established under increased scrutiny.

-

Geopolitical Escalation: The US-Iran conflict presents an asymmetric risk scenario where escalation could rapidly transform from a contained regional issue into a broader market-disrupting event. The targeting of Gulf energy infrastructure remains a explicit concern [3].

-

Post-Rebalancing Friction: The S&P 500 reconstitution will force institutional investors to adjust positions in affected securities, potentially creating dislocation between closing and opening prices for stocks experiencing significant weight changes.

-

Volatility Premium: Elevated VIX levels and implied volatility create potential premium opportunities for volatility-sellers and options strategists who can manage tail risk effectively.

-

Sector Rotation Alpha: The rebalancing-driven rotation from consumer names into AI infrastructure plays may create sustained momentum in the receiving securities, offering position-taking opportunities for longer-term oriented investors.

-

Risk-Off Positioning: Should the Iran conflict escalate meaningfully, inverse equity products and put options could generate significant returns as part of a defensive portfolio strategy.

The March 20, 2026 triple witching event represents a confluence of technical derivatives expiration, index rebalancing, and geopolitical risk that creates elevated volatility conditions. The $5.7 trillion options expiration [1] combined with S&P 500 rebalancing [2] and US-Iran tensions [3] creates a complex risk environment that investors should approach with heightened monitoring and position management.

Current market data shows mixed signals heading into the expiration: equities showing modest strength (S&P +0.35%, NASDAQ +1.00%) [0], but commodities showing divergent moves (oil -0.92%, gold -4.53%) [0] that suggest ongoing uncertainty about the risk trajectory. Historical patterns of negative median returns (-0.36%) and low win rates (25%) on triple witching days [4] suggest a cautious stance is warranted, particularly given the additional geopolitical risk premium in the system.

Investors are advised to monitor position exposure, stress-test portfolios for 2-5% moves in either direction, watch for gap risk at Monday’s open, maintain energy sector vigilance, and track VIX levels for early volatility warning signs.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.