Private Credit Market Stress: Liquidity Mismatch and Redemption Pressures

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

This analysis is based on Jim Cramer’s commentary from CNBC published on March 20, 2026 [1], which addresses the growing stress in private credit markets. The event occurs against a backdrop of unprecedented redemption pressures on private credit funds, a development that has been building over recent quarters as investors reassess their allocations in an environment of heightened market volatility.

The private credit industry has experienced explosive growth, with fund managers globally attracting $1.3 trillion in new capital from 2021 through 2025, much of it through evergreen funds distributed through the wealth channel [3]. This rapid expansion created a structural vulnerability: the mismatch between illiquid private debt instruments—which feature long-dated cash flows and limited secondary marketability—and periodic redemption terms offered to investors, particularly retail participants seeking yield enhancement.

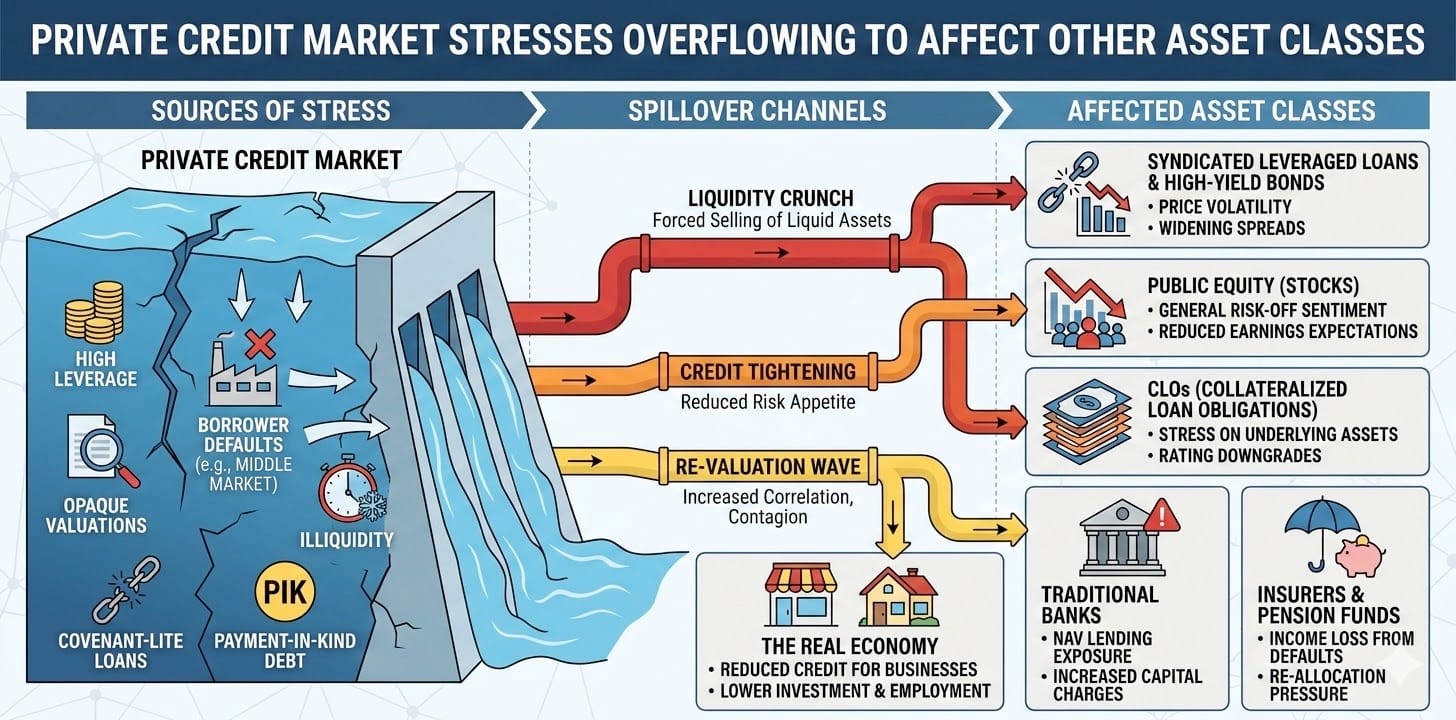

The private credit market is undergoing a critical stress test characterized by several interconnected pressures. First, elevated redemption requests have reached all-time highs across major funds. Blackstone’s $82 billion Private Credit Fund (BCRED) faced record redemption requests of 7.9% of assets, approximately $3.8 billion [4]. BlackRock restricted withdrawals from its HPS Corporate Lending debt fund after redemption requests hit approximately 9.3% ($1.2 billion), exceeding its 5% quarterly limit [5]. Blue Owl ended regular quarterly liquidity payments in its Blue Owl Capital Corporation II fund, while Morgan Stanley limited withdrawals from its North Haven Private Income Fund, returning only $169 million (45.8% of tender requests) [5].

Second, the fundamental liquidity mismatch has become untenable. Private credit assets are inherently illiquid—non-tradable instruments with long-dated cash flows—combined with periodic redemption terms offered to investors. When redemption demand exceeds limits, fund managers face an unenviable choice: relax liquidity caps to satisfy investors (potentially compromising long-term portfolio value) or gate redemptions (alienating investors and signaling weakness) [3].

Third, credit quality concerns are emerging in certain segments. Rising defaults in highly leveraged segments, particularly in software and other sectors with elevated leverage levels, add another layer of stress to the asset class [13].

The current liquidity squeeze has affected some of the largest and most prominent names in alternative asset management, revealing structural vulnerabilities in the industry’s expansion model. The democratization of private credit through vehicles like business development companies (BDCs), interval funds, and semi-liquid strategies has attracted retail investors who may not fully understand the illiquid nature of the underlying assets [5][10].

A secondaries market has emerged as a pressure valve, with transaction volume forecast to approach $300 billion annually in the next 12-24 months [8]. This development provides an “off-ramp” for investors seeking liquidity but also introduces new pricing dynamics and potential value dislocations.

Jim Cramer’s assertion that “private credit funds weren’t meant to be traded” reflects a fundamental critique of the structural mismatch between the illiquid nature of private credit assets and the expectations of investors in semi-liquid vehicles [1]. This view aligns with broader industry debates about whether retail-friendly private credit products appropriately manage investor expectations about liquidity.

The rapid growth of retail-focused private credit products created what experts describe as a “mismatch” between the private credit investment model and the incentives of individual investors [10]. Retail investors may not fully appreciate that private credit funds may limit redemptions because the underlying loans are typically multi-year investments that can be difficult to sell quickly without potential losses [12].

Some observers have drawn parallels between current private credit market conditions and the conditions that preceded the 2008 financial crisis, citing lack of transparency within private credit funds and asset managers halting withdrawals [2]. While industry experts like Lynne Westbrook of Ocorian expect greater selectivity and performance dispersion with more restructurings and isolated defaults, rather than systemic shock [5], the structural similarities warrant continued monitoring.

The current stress may drive significant industry restructuring. According to Alexander Lis of Social Discovery Ventures, the asset class could shrink, shifting back to a larger share of long-term institutional capital instead of liquidity-sensitive investors [5]. This could fundamentally alter the competitive dynamics of the private credit industry, potentially benefiting well-capitalized institutional-focused managers while disadvantaging those that built retail-focused platforms.

-

Liquidity Gating Risk: The probability of continued redemption restrictions remains elevated as long as investor outflows persist. Funds that have already restricted withdrawals may face continued reputational damage and potential asset base contraction.

-

Credit Quality Deterioration: Rising defaults in highly leveraged segments could trigger additional redemption pressure as investors anticipate future losses. This creates a potential negative feedback loop where forced selling depresses asset values, triggering further redemptions.

-

Retail Investor Flight: The retail channel, which drove significant growth in recent years, could experience sustained outflows as investor confidence wavers. This would particularly impact managers with large retail AUM.

-

Regulatory Scrutiny: Increased regulatory attention to private credit fund structures and liquidity management could impose additional compliance burdens and potentially restrict product structures.

-

Secondaries Market Growth: The emerging secondaries market presents opportunities for investors seeking liquidity at potentially discounted valuations. Transaction volume is forecast to approach $300 billion annually [8], creating a new profit center for participants.

-

Dislocation Opportunities: Well-capitalized investors with long-term horizons may find attractive opportunities in stressed private credit segments, particularly in secondaries transactions where sellers face forced liquidation.

-

Platform Consolidation: Managers with strong liquidity management frameworks and transparent structures may attract capital migrating from managers with weaker redemption track records, potentially gaining market share.

-

Institutional Reallocation: If retail participation contracts, the industry may shift toward a more stable investor base of long-term institutional capital, potentially reducing liquidity-driven volatility.

The private credit market’s current stress reflects a fundamental structural tension between the illiquid nature of underlying assets and the liquidity expectations created by retail-friendly product structures. Jim Cramer’s characterization that these funds “weren’t meant to be traded” encapsulates the core issue: the industry expanded rapidly by offering semi-liquid products that promised periodic liquidity while investing in inherently illiquid instruments.

Major fund managers have responded to redemption pressures through various mechanisms, including restricting withdrawals, ending regular liquidity payments, and limiting tender acceptance. The emergence of a secondaries market provides an alternative liquidity channel, though at volumes that may not fully address current demand.

Industry participants should anticipate continued elevated redemption requests in the near term, with potential for further credit quality deterioration in highly leveraged segments. The long-term trajectory may involve a rebalancing toward institutional capital and away from liquidity-sensitive retail investors, fundamentally reshaping competitive dynamics within the industry.

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.