Repercussions of a Potential OpenAI Valuation Drop on the AI Sector and Public Companies

Unlock More Features

Login to access AI-powered analysis, deep research reports and more advanced features

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.

Related Stocks

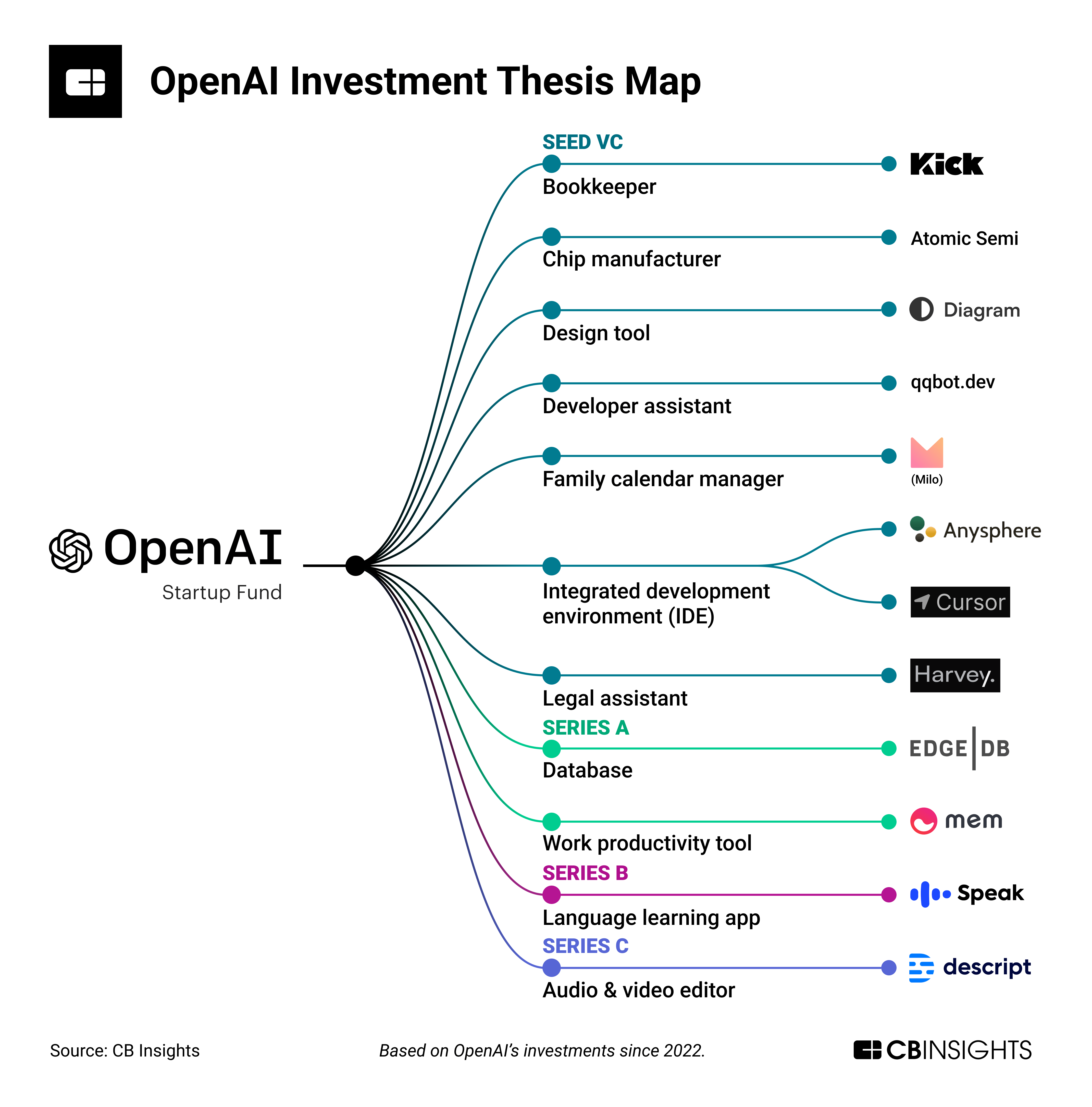

This analysis is based on a Reddit discussion and verified web search data [1-18].

OpenAI’s $500B valuation acts as a narrative anchor for the AI sector [3]. A drop would force investors to reevaluate AI cashflow expectations [4], leading to lower valuations for high-multiple AI stocks like NVDA [4]. Microsoft’s 27% stake (valued at ~$135B) [8] would face significant devaluation, though its Azure growth (39%) [10] may mitigate impacts. NVDA has a circular dependency with OpenAI (invests in OpenAI, which buys its chips) [12], so a drop could reduce chip purchases, but long-term demand from Blackwell/Rubin [11] may offset losses. Cloud providers rely on AI startups (51% of global VC deal value) [15], so reduced VC funding (seed rounds down 25% QoQ [16]) could slow growth. Google’s Gemini models are cheaper (up to 25x) than OpenAI’s [17], giving it a competitive edge [18].

- OpenAI’s valuation is belief-driven (H1 2025 revenue $4.3B vs Q3 loss $11.5B) [6], making it vulnerable to correction.

- Google’s cost advantage could accelerate market share gain if OpenAI’s valuation drops [17,18].

- AI startups face extinction as seed rounds shrink [16], leading to sector consolidation.

- Long-term AI growth remains intact despite short-term valuation risks [3].

- Microsoft’s stake devaluation (up to $121.5B loss for 90% drop) [8].

- NVDA’s short-term revenue impact from reduced OpenAI chip purchases [12].

- Cloud providers’ growth slowdown due to declining AI startup VC funding [15,16].

- Zero-revenue AI startups facing funding dry-up [16].

- Google gaining market share with cheaper AI offerings [17,18].

- Enterprise AI adoption (e.g., Microsoft Copilot) sustaining long-term cloud growth [10].

- NVDA’s $500B Blackwell/Rubin revenue visibility [11].

- OpenAI: $500B valuation, $4.3B H1 2025 revenue, $11.5B Q3 loss [6].

- Microsoft: 27% stake ($135B value), $3.1B Q3 profit reduction from OpenAI [8].

- NVDA: Q3 2025 revenue $57B, $100B pact with OpenAI (no assurance) [13,14].

- Google: Gemini models up to 25x cheaper than OpenAI’s [17].

- VC Funding: AI startups get 51% of global VC deal value, seed rounds down 25% QoQ [15,16].

Insights are generated using AI models and historical data for informational purposes only. They do not constitute investment advice or recommendations. Past performance is not indicative of future results.

About us: Ginlix AI is the AI Investment Copilot powered by real data, bridging advanced AI with professional financial databases to provide verifiable, truth-based answers. Please use the chat box below to ask any financial question.